Finance Act 1966

1966 CHAPTER 18

An Act to grant certain duties, to alter other duties, and to amend the law relating to the National Debt and the Public Revenue, and to make further provision in connection with Finance.

Editorial Information

X1The text of Ss. 12(6)(b), 15(5), Sch. 3, para. 6 was taken from S.I.F. Group 12:1 (Betting, Gaming and Lotteries: General), Ss. 2, 53(1)-(4) from S.I.F. Group 40:1 (Customs and Excise: General), ( Ss. 27, Sch.5, para. 19, Sch. 6, paras. 14, 23, Sch. 13 from S.I.F Group 63:1 (Income, Corporation & Capital Gains Taxes: Income and Corporation Taxes) and Ss. 45-47 from S.I.F. Group 114 (Stamp Duty) ; provisions omitted from S.I.F. have been dealt with as referred to in other commentary.

X2General amendments to Tax Acts, Income Tax Acts, and/or Corporation Tax Acts made by legislation after 1.2.1991 are noted against Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1) but not against each Act

Extent Information

E1For the extent of this Act see s. 53(4)(5)

Modifications etc. (not altering text)

C1Words of enactment omitted under authority of Statute Law Revision Act 1948 (c. 62), s. 3

C2General amendments to Tax Acts made by Taxes Management Act 1970 (c. 9, SIF 63:1), s. 41A(7) (as added by Finance Act 1990 (c. 29, SIF 63:1), s. 95(1)(2)), British Telecommunications Act 1981 (c. 38, SIF 96), s. 82(2)(7); Telecommunications Act 1984 (c. 12, SIF 96), s. 72(3); Finance Act 1984 (c. 43, SIF 63:1), ss. 82(6), 85(2), 89(1)(7), 96(1)(7), 98(7), Sch. 9 para. 3(2)(9), Sch. 16 paras. 6, 12 and Finance Act 1985 (c. 54, SIF 63:1), ss. 72(1), 74(5), Sch. 23 para. 15(4), S.I. 1987/530, regs. 11(2), 13(1), 14, Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1), ss. 4, 6, 7, 9, 32, 34, 78, 134, 135, 141, 142, 185, 191, 193, 194, 195, 200, 203, 209, 212, 213, 219, 247, 253, 272, 287, 314, 315, 317, 318, 325, 326, 327, 345, 350, 351, 368, 375, 381, 397, 414, 432, 440, 442, 446, 458, 460, 461, 463, 463(2)(3) (as added by Finance Act 1990 (c. 29, SIF 63:1), s. 50(2) ), 468, 474, 475, 486, 490, 491, 503, 511, 518, 524, 532, 544, 550, 556, 558, 569, 572, 582, 595, 601, 613, 617, 619, 621, 639, 656, 660, 663, 676, 689, 691, 694, 700, 701, 714, 716, 739, 743, 754, 763, 776, 780, 781, 782, 787, 789, 811, 828, 829, 832, 833, 834, 835, 837, 838, 839, 840, 841, 842, Sch. 2 para. 5, Sch. 4 para. 5, Sch. 13 para. 10, Sch. 16 para. 10, Sch. 21 para. 6, Sch. 26 para. 1, Sch. 27 para. 20, Finance Act 1988 (c. 39, SIF 63:1), ss. 66, 127(1)(6), Sch. 12 para. 6, Capital Allowances Act 1990 (c. 1, SIF 63:1), ss. 28(1), 68(8), 74, 82, 83(5), 148(5), 163(4), 164(2), S.I. 1990/627 and Finance Act 1990 (c. 29, SIF 63:1), s. 25(10)

Commencement Information

I1Act partly in force at Royal Assent, partly prospective, see individual sections; all provisions so far as unrepealed wholly in force at 1.2.1991

Finance Act 1966

1966 CHAPTER 18

An Act to grant certain duties, to alter other duties, and to amend the law relating to the National Debt and the Public Revenue, and to make further provision in connection with Finance.

[3rd August 1966]X3

Editorial Information

X3The text of Ss. 12(6)(b), 15(5), Sch. 3, para. 6 was taken from S.I.F. Group 12:1 (Betting, Gaming and Lotteries: General), Ss. 2, 53(1)-(4) from S.I.F. Group 40:1 (Customs and Excise: General), ( Ss. 27, Sch.5, para. 19, Sch. 6, paras. 14, 23, Sch. 13 from S.I.F Group 63:1 (Income, Corporation & Capital Gains Taxes: Income and Corporation Taxes) and Ss. 45-47 from S.I.F. Group 114 (Stamp Duty) ; provisions omitted from S.I.F. have been dealt with as referred to in other commentary.

Modifications etc. (not altering text)

C10Words of enactment omitted under authority of Statute Law Revision Act 1948 (c. 62), s. 3

C11General amendments to Tax Acts made by Taxes Management Act 1970 (c. 9, SIF 63:1), s. 41A(7) (as added by Finance Act 1990 (c. 29, SIF 63:1), s. 95(1)(2)), British Telecommunications Act 1981 (c. 38, SIF 96), s. 82(2)(7); Telecommunications Act 1984 (c. 12, SIF 96), s. 72(3); Finance Act 1984 (c. 43, SIF 63:1), ss. 82(6), 85(2), 89(1)(7), 96(1)(7), 98(7), Sch. 9 para. 3(2)(9), Sch. 16 paras. 6, 12 and Finance Act 1985 (c. 54, SIF 63:1), ss. 72(1), 74(5), Sch. 23 para. 15(4), S.I. 1987/530, regs. 11(2), 13(1), 14, Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1), ss. 4, 6, 7, 9, 32, 34, 78, 134, 135, 141, 142, 185, 191, 193, 194, 195, 200, 203, 209, 212, 213, 219, 247, 253, 272, 287, 314, 315, 317, 318, 325, 326, 327, 345, 350, 351, 368, 375, 381, 397, 414, 432, 440, 442, 446, 458, 460, 461, 463, 463(2)(3) (as added by Finance Act 1990 (c. 29, SIF 63:1), s. 50(2) ), 468, 474, 475, 486, 490, 491, 503, 511, 518, 524, 532, 544, 550, 556, 558, 569, 572, 582, 595, 601, 613, 617, 619, 621, 639, 656, 660, 663, 676, 689, 691, 694, 700, 701, 714, 716, 739, 743, 754, 763, 776, 780, 781, 782, 787, 789, 811, 828, 829, 832, 833, 834, 835, 837, 838, 839, 840, 841, 842, Sch. 2 para. 5, Sch. 4 para. 5, Sch. 13 para. 10, Sch. 16 para. 10, Sch. 21 para. 6, Sch. 26 para. 1, Sch. 27 para. 20, Finance Act 1988 (c. 39, SIF 63:1), ss. 66, 127(1)(6), Sch. 12 para. 6, Capital Allowances Act 1990 (c. 1, SIF 63:1), ss. 28(1), 68(8), 74, 82, 83(5), 148(5), 163(4), 164(2), S.I. 1990/627 and Finance Act 1990 (c. 29, SIF 63:1), s. 25(10)

Part IU.K. Customs and Excise

1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F1U.K.

Textual Amendments

F1S. 1 repealed (with saving) by S.I. 1977/910

2 Reliefs for shipbuilders in respect of certain duties.U.K.

(1)The provisions of this section shall have effect for the purpose of affording relief in respect of duties of customs and excise chargeable on hydrocarbon oils, vehicle excise duty (including such duty chargeable in Northern Ireland) . . . F2 incurred in connection with the construction and fitting out of certain vessels and other floating structures.

(2)If, on an application made in accordance with directions from time to time given by the Commissioners for the purposes of this section, it is shown to the satisfaction of the Commissioners that a vessel or other structure to which this section applies, having been constructed in the United Kingdom by the applicant pursuant to a contract (whenever made) under which it was to become the property of some other person, was delivered by him pursuant to that contract after the coming into force of this section, the applicant shall, subject to sub-sections (7) to (9) below, be entitled to receive from the Commissioners a payment of an amount determined in accordance with the two next following subsections.

(3)Subject to the next following subsection, the said amount shall be such percentage as the Treasury may by order prescribe of the price payable under the contract in question for the said vessel or structure and all fittings and other equipment supplied by the applicant therewith, or, if that price appears to the commissioners to be greater than the open market value of the vessel or structure and its said fittings and equipment as determined in accordance with Part I of Schedule 1 to this Act and the Commissioners so decide, the prescribed percentage of that value; and an order under this subsection may prescribe different percentages in relation to different descriptions of vessels or structures.

Any price which is expressed in a foreign currency shall be treated for the purposes of this subsection as equivalent to a sum calculated in such manner as the Commissioners may direct.

(4)The price or value referred to in the last foregoing subsection shall, in the circumstances specified in Part II of the said Schedule 1, be treated for the purposes of that subsection as reduced as mentioned in that Part.

(5)The vessels and other structures to which this section applies are as follows—

(a)any ship, within the meaning of the Merchant Shipping Acts 1894 to 1965, the gross tonnage of which, ascertained in accordance with those Acts, is not less than eighty tons; and

(b)any other vessel, or other structure capable of floating on the sea, which is of a description specified in that behalf by an order of the Treasury, and in respect of which any conditions so specified are satisfied:

Provided that the Treasury may by order exclude from the operation of this section any ship, or any ship of a specified description, in the case of which less than a specified percentage of the cost of its construction, calculated in accordance with the order, was attributable to United Kingdom expenditure as defined in the order.

(6)References in this section to the construction of vessels and other structures do not include references to their reconstruction, refitting or repair.

(7)If, within one month of the coming into force of this section, any person shows to the satisfaction of the Commissioners—

(a)that a vessel or other structure has been, or is to be, delivered to him pursuant to a contract made before 23rd June 1966, and has been, or is to be, exported by him pursuant to another such contract, and

(b)that, by reason of its exportation pursuant to the last-mentioned contract, he is or may become entitled to payment of a rebate under section 7 of the M1Finance (No. 2) Act 1964 (export rebates),

No payment shall be made under this section in respect of the said vessel or structure unless that person either by notice in writing to the Commissioners waives any right to the rebate in question or fails for any reason to become entitled thereto.

(8)No person shall be entitled to a rebate under the said section 7 in respect of any vessel or other structure in respect of which a payment under this section is, or could if applied for have been, made to any other person; and a person who, but for this subsection, would be entitled as respects any vessel or other structure to both such a rebate and such a payment may receive either, as he elects, but not both.

(9)Where in the case of any vessel or structure the whole or any part of the price payable as mentioned in subsection (3) above is not received in accordance with the contract in question by the applicant for a payment under this section, the Commissioners if they think fit may require the applicant to repay the whole or any part of any payment made to him on the application or, as the case may be, may withhold from him the whole or any part of any payment which would otherwise fall to be so made.

(10)It shall be the duty of any person to or by whom a payment under this section has been made or applied for to inform the Commissioners of any event which would entitle them to exercise the powers conferred by the last foregoing subsection, and any person who fails to comply with this subsection shall be liable to a penalty of [F3level 3 on the standard scale].

(11)The provisions of Part III of Schedule 1 to this Act shall have effect for the purposes of this section.

(12)For the avoidance of doubt it is hereby declared that the allowances referred to in [F4section 1 of the M2Excise Duties (Surcharges or Rebates) Act 1979] do not include payments under this section.

(13)Payments by the Commissioners under this section shall be made out of the sums received by them on account of duties of customs and excise . . . F2; and—

(a)notwithstanding anything in [F5section 3(4) of the M3Vehicle (Excise) Act 1971] . . . F6, the Treasury may give directions for the payment to the Commissioners, at such times and in such manner as the Treasury may determine, out of the duties levied under that Act of such sums as the Treasury think fit having regard to the extent to which payments under this section are designed to afford relief in respect of such duties;

(b)any sums so paid shall be treated for the purposes of [F7section 17 of the M4Customs and Excise Management Act 1979] (disposal of duties of customs and excise) as money received by the Commissioners on account of duties of customs and excise.

(14)Any order under the foregoing provisions of this section may be varied or revoked by a subsequent order, and shall be made by statutory instrument subject to annulment in pursuance of a resolution of the House of Commons.

(15)This section shall come into force on such day as may be appointed by the Treasury by an order under this subsection made by statutory instrument and laid before Parliament after being made, but shall, in its application to any vessel or other structure by virtue of an order under subsection (5) above, have effect as if it had not come into force until such later day, if any, as may be specified in that order.

Textual Amendments

F2Words repealed by Finance Act 1972 (c. 41), s. 54(8), Sch. 28 Pt. II

F3Words substituted by virtue of (E.W.) Criminal Justice Act 1982 (c. 48, SIF 39:1), ss. 38, 46 and (S.) Criminal Procedure (Scotland) Act 1975 (c. 21, SIF 39:1), ss. 289F, 289G and (N.I.) by S.I. 1984/703, (N.I. 3) arts. 5, 6

F4Words substituted by Excise Duties (Surcharges or Rebates) Act 1979 (c.8), Sch. 1 para. 3

F5Words substituted by virtue of Vehicles (Excise) Act 1971 (c. 10), Sch. 7 Pt. II para. 11

F6Words repealed by Vehicle and Driving Licences Act 1969 (c. 27), Sch. 3

F7Words substituted by Customs and Excise Management Act 1979 (c. 2), Sch. 4 para. 12 Table Pt. I

Modifications etc. (not altering text)

C312.9.1966 appointed under s. 2(15) by S.I. 1966/1025, art. 1

Marginal Citations

3. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F8U.K.

Textual Amendments

F8S. 3 repealed (with saving) by Finance Act 1977 (c. 36), s. 59(5), Sch. 9 Pt. II

4, 5.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F9U.K.

Textual Amendments

F9Ss. 4, 5 repealed by Finance Act 1968 (c. 44), ss. 1(3), 61(10), Sch. 20 Pt. I

6. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F10U.K.

Textual Amendments

7. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F11U.K.

Textual Amendments

F11S. 7 repealed by Finance Act 1978 (c. 42), s. 80(5), Sch. 13 Pt. I

8. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F12U.K.

Textual Amendments

F12S. 8 repealed by Vehicles (Excise) Act 1971 (c. 10), s. 39(5), Sch. 8 Pt. I

9. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F13U.K.

Textual Amendments

F13S. 9 repealed by European Communities Act 1972 (c. 68), s. 4, Sch. 3 Pt. I

10, 11.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F14U.K.

Textual Amendments

F14Ss. 10, 11 repealed by Customs and Excise Management Act 1979 (c. 2), s. 177(3), Sch. 6 Pt I

Duties relating to betting and gamingU.K.

12 General Betting Duty. U.K.

(1)—(5). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F15

(6)The pool betting duty shall not be chargeable on any bet made as mentioned in subsection (1)(c) of this section on or after 24th October 1966, and accordingly from that date—

(a). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F15

(b)paragraph 4(a)(i) of Schedule 5 to the M5Betting, Gaming and Lotteries Act 1963 (which relates to the disposal of amounts staked by means of a totalisator on a dog racecourse) for the words “pool betting duty” there shall be substituted the words “general betting duty” ;

and as from that date bookmakers’ licence duty shall cease to be charged.

Textual Amendments

F15S. 12(1)–(6)(a) repealed by Betting and Gaming Duties Act 1972 (c. 25), s. 29(2), Sch. 7

Modifications etc. (not altering text)

C4The text of Ss. 12, 53(7), Sch. 5 para. 19 and Sch. 13 is in the form in which it was originally enacted; it was not reproduced in Statutes in Force and, except as specified, does not reflect any amendments or repeals which may have been made prior to 1.2.1991.

Marginal Citations

13. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F16U.K.

Textual Amendments

F16S. 13 repealed, except as respects any gaming before 1st October 1970, by Finance Act 1970 (c. 24), s. 36(8), Sch. 8 Pt. I

14. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F17U.K.

Textual Amendments

F17S. 14 repealed (1.10.1969) by Finance Act 1969 (c. 32), Sch. 21 Pt. I

Duties relating to betting and gamingU.K.

15 Additional or supplementary provisions as to duties on betting or gaming.U.K.

(1)—(4). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F18

(5)The supplemental provisions set out in Schedule 3 to this Act shall have effect with respect to the duties relating to betting and gaming.

(6). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F18

Textual Amendments

F18S. 15(1)–(4)(6) repealed by Betting and Gaming Duties Act 1972 (c. 25), Sch. 7

16. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F19U.K.

Textual Amendments

F19S. 16 repealed by Finance Act 1967 (c. 54), ss. 1(1)(b), 45(8), Sch. 16 Pt. III

Part IIU.K.

17—25.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F20U.K.

Textual Amendments

Part IIIU.K. CORPORATION TAX ACTS

26. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F21U.K.

Textual Amendments

27 Amendments of Corporation Tax Acts.U.K.

Schedule 5 to this Act, which contains amendments of the Corporation Tax Acts relating to deductions allowable in computing profits,capital gains, annuity business of assurance companies, close companies, the definition of company distributions and other matters, and Schedule 6 to this Act, which contains administrative provisions for the Corporation Tax Acts, shall have effect.

28. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F22U.K.

Textual Amendments

29. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F23U.K.

Textual Amendments

F23S. 29 repealed by Statute Law (Repeals) Act 1978 (c. 45), s. 1(1), Sch. 1 Pt IX

30. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F24U.K.

Textual Amendments

31, 32.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F25U.K.

Textual Amendments

F25Ss. 31, 32 repealed by Finance Act 1972 (c. 41), Sch. 28 Pt. VI

33, 34.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F26U.K.

Textual Amendments

Part IVU.K.

35—39.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F27U.K.

Textual Amendments

40. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F28U.K.

Textual Amendments

F28S. 40 repealed by Finance Act 1969 (c. 32), s. 61(6), sch. 21 Pt. V

Part VU.K.

41, 42.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F29U.K.

Textual Amendments

F29Ss. 41, 42 repealed (with saving) by Finance Act 1975 (c. 7), ss. 50, 52(2)(3), 59, Sch. 13 Pt. I

43. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F30U.K.

Textual Amendments

F30S. 43 repealed (with saving) by Capital Gains Tax Act 1979 (c. 14), ss. 157(1), 158, Sch. 6 para. 10(2)(b), Sch. 8

Part VIU.K.

44. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F31U.K.

Textual Amendments

Part VIIU.K. Miscellaneous

45 Harbour reorganisation schemes: corporation tax and stamp duty.U.K.

(1)—(4). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F32

(5)Where a certified harbour reorganisation scheme contains provision for the transfer of an undertaking, or of any other description of property, to a harbour authority, then, in considering whether any and if so what duty is payable under section 12 of the M6Finance Act 1895 (which relates to the stamp duty payable in connection with certain statutory conveyances), the consideration for the transfer shall be left out of account; and no stamp duty shall be payable on any contract or agreement for any such transfer if the contract or agreement is conditional on the making and certification of a harbour reorganisation scheme.

(6)In this section—

“harbour authority” has the same meaning as in the M7Harbours Act 1964;

“harbour reorganisation scheme” means any statutory provision providing for the management by a harbour authority of any harbour or group of harbours in the United Kingdom, and “certified”, in relation to any harbour reorganisation scheme, means certified by a Minister of the Crown or Government department as so providing with a view to securing, in the public interest, the efficient and economical development of the harbour or harbours in question;

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F33

(7). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F32

Textual Amendments

F32S. 45(1)–(4)(7) repealed by Income and Corporation Taxes Act 1970 (c. 10), Sch. 16

F33Words repealed by Income and Corporation Taxes Act 1970 (c. 10), s. 539(1), Sch. 16

Marginal Citations

46. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F34U.K.

Textual Amendments

F34S. 46 repealed by Finance Act 1985 (c. 54, SIF 114), s. 98(6), Sch. 27 Pt. IX(3)

47. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F35U.K.

Textual Amendments

F35S. 47 repealed by Finance Act 1989 (c. 26, SIF 114), ss. 173, 187(1), Sch. 17 Pt. IX

48. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F36U.K.

Textual Amendments

F36S. 48 repealed by Post Office Act 1969 (c. 48), s. 141, Sch. 11 Pt. II

49—51.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F37U.K.

Textual Amendments

52. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F38U.K.

Textual Amendments

F38S. 52 repealed by European Communities Act 1972 (c. 68), s. 4, Sch. 3 Pt. II

53 Short title, construction, extent and repeals.U.K.

(1)This Act may be cited as the Finance Act 1966.

(2)In this Act Part I shall be construed as one with the [F39M8Customs and Excise Management Act 1979]; . . . F40; Part III shall be construed as one with the Corporation Tax Acts; . . . F40; . . . F41; and so much of Part VII as relates to stamp duties shall be construed as one with the M9Stamp Act 1891.

(3)Any reference in this Act to any other enactment shall, except so far as the context otherwise requires, be construed as a reference to that enactment as amended or applied by or under any other enactment, including this Act.

(4)Except as otherwise expressly provided, such of the provisions of this Act as relate to matters in respect of which the Parliament of Northern Ireland has power to make laws shall not extend to Northern Ireland.

(5)This Act, in so far as it affects the operation of the Sugar Act 1956, shall extend to the Isle of Man.

(6). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F42

(7)The enactments mentioned in Schedule 13 to this Act are hereby repealed to the extent mentioned in the third column of that Schedule, but subject to any provision in relation thereto made at the end of any Part of that Schedule.

Textual Amendments

F39Words substituted by Customs and Excise Management Act 1979 (c. 2), Sch. 4 para. 12 Table Pt. I

F40Words repealed by Income and Corporation Taxes Act 1970 (c. 10), s. 539(1), Sch. 16

F41Words repealed in relation to deaths occurring after 13.4.1975 and, so far as regards the duties referred to in s. 52(2)(b) of the repealing Act, in relation to any death, by Finance Act 1975 (c. 7, SIF 99:3), ss. 52(2), 59, Sch. 13 Pt. I note (with a saving in s. 52(3) in relation to repayment or allowance in respect of sums paid before 13.3.1975 on account of the said duties)

Modifications etc. (not altering text)

C5S. 53(4) amended by Northern Ireland Constitution Act 1973 (c. 36), s. 40

C6The text of Ss. 12, 53(7), Sch. 5 para. 19 and Sch. 13 is in the form in which it was originally enacted; it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991.

Marginal Citations

SCHEDULES

Section 2.

SCHEDULE 1U.K. Reliefs For Shipbuilders

Part IU.K. Determination of Open Market Value

1(1)The open market value of any vessel or other structure and its fittings and equipment shall be taken for the purposes of section 2 of this Act to be the price which they would fetch at the time of their delivery pursuant to the contract in question on a sale in the open market between buyer and seller independent of each other.U.K.

(2)The said price shall be determined on the assumption that the buyer will bear freight, insurance and all other costs, charges and expenses incurred in respect of the vessel or structure and other items in question after their delivery as aforesaid or, where delivery is to be effected outside the United Kingdom, after their departure from the United Kingdom for the purpose.

(3)For the purposes of this paragraph, a sale in the open market between a buyer and seller independent of each other presupposes—

(a)that the vessel or structure and other items in question are the sole consideration for the price paid, and

(b)that the price is not influenced by any commercial, financial or other relationship, whether by contract or otherwise, between the seller or any person associated in business with him and the buyer or any person associated in business with him (other than the relationship created by the sale of the said vessel or structure and other items), and

(c)that neither the seller nor any person associated in business with him has provided any part of the price, and that no part of the price will be returned to the buyer or any person associated in business with him.

(4)For the purposes of the last foregoing sub-paragraph, two persons shall be deemed to be associated in business with one another if, whether directly or indirectly, either of them has any interest in the business or property of the other, or both have a common interest in any business or property, or some third person has an interest in the business or property of both of them.

Part IIU.K. Reductions in Purchase Price or Open Market Value

2(1)Where the amount payable in respect of any vessel or other structure under the said section 2 is, by virtue of subsection (3) thereof, to be determined by reference to the price payable as mentioned in that subsection, then—U.K.

(a)if the terms of the contract in question are such that the applicant for the payment will bear any of the following, that is, any freight, insurance or other costs, charges or expenses incurred in respect of the vessel or structure or its fittings or equipment after their delivery pursuant thereto or, where delivery is to be effected outside the United Kingdom, after their departure from the United Kingdom for the purpose, the price shall be treated for the purposes of that subsection as reduced by an amount reflecting the burden thus assumed by the applicant;

(b)if the whole or any part of the price is payable twelve months or more after the time when the property in the vessel or structure passes or, if later, the time of delivery of the vessel or structure or of its departure from the United Kingdom for the purpose of delivery, the price shall be treated for those purposes as reduced by an amount representing the discount which would be chargeable for obtaining payment at that earlier time at a rate of interest equal to the bank rate then prevailing.

(2)In the foregoing sub-paragraph “bank rate” means the minimum rate at which the Bank of England will lend to a discount house having access to the Discount Office of the Bank.

3U.K.If, after consultation with the Board of Trade, it appears to the Commissioners that the fittings and other equipment supplied with any vessel or other structure include any items the supply of which would not in the ordinary course of events be undertaken by a person building such a vessel or structure for delivery to another as that other’s property, the price or, as the case may be, open market value referred to in the said subsection (3) shall be treated for the purposes of that subsection as reduced by an amount equal to the open market value of the items in question; and the provisions of paragraph 1 of this Schedule shall apply for the purpose of determining that value, subject to any necessary modifications.

Modifications etc. (not altering text)

C7Functions of Board of Trade now exercisable concurrently by Secretary of State: S.I. 1970/1537, art. 2(1)

Part IIIU.K. Supplemental

4U.K.The following provisions of the [F43M10Customs and Excise Management Act 1979] shall apply in relation to payments under the said section 2 as they apply in relation to drawbacks, allowances or repayments under [F43the Customs and Excise Acts 1979], that is to say, [F43section 135] (time limit on payment), [F43section 136(1) and (2)] (offences in connection with claims) and [F43section 167(4)] (recovery of overpayments).

Textual Amendments

F43Words substituted by Customs and Excise Management Act 1979 (c. 2), Sch. 4 para. 12 Table Pt. I

Marginal Citations

5(1)Any officer or person authorised by the Commissioners may require any person who has been concerned at any stage with a vessel or other structure in respect of which an application has been made under the said section 2, or with any fittings or other equipment supplied therewith, or with any payment in respect of the vessel or structure or any fittings or other equipment so supplied—U.K.

(a)to furnish, within such time as that officer or person may require, such information as may be reasonably necessary to enable the Commissioners to determine whether the applicant is entitled to a payment under that section, or liable to make any repayment thereunder, or to determine the amount of any payment to which the applicant is so entitled, and

(b)to produce for inspection by that officer or person, at such time and place as he may require, any books or accounts or other document of whatever nature relating to, or to any payment in respect of, the said vessel, structure, fittings or equipment.

(2)Any such officer or person shall be entitled to take extracts from or make copies of any document produced to him under the foregoing sub-paragraph.

(3)If any person fails to comply with any requirement under sub-paragraph (1) above, he shall be liable to a penalty of [F44level 3 on the standard scale], together with a further penalty of ten pounds for each day during which failure to comply with the requirement continues.

Textual Amendments

F44Words substituted by virtue of (E.W.) Criminal Justice Act 1982 (c. 48, SIF 39:1), ss. 38, 46 and (S.) Criminal Procedure (Scotland) Act 1975 (c. 21, SIF 39:1), ss. 289F, 289G and (N.I.) by S.I. 1984/703, (N.I. 3) arts. 5, 6

6(1)Any dispute as to the determination for the purposes of an application under the said section 2 of the price or value referred to in subsection (3) of that section, or of any amount by which that price or value is to be treated as reduced by virtue of subsection (4) thereof, shall be referred to a referee appointed in accordance with the next following sub-paragraph.U.K.

(2)A reference under the foregoing sub-paragraph shall be to a person (not being an official of any government department) appointed by the Lord Chancellor or, if the application for the purposes of which the determination is made relates to a vessel or structure constructed in Scotland or Northern Ireland, or was by a company incorporated in Scotland or Northern Ireland, and the applicant in either case so requires, appointed by the Lord President of the Court of Session or as the case may be, the Lord Chief Justice of Northern Ireland.

(3)The procedure on any such reference shall be such as the referee may determine.

(4)Sub-paragraph (1) above shall not have effect, and any price, value or amount falling to be determined for the purposes of the said subsection (3) or (4) shall be that fixed by the Commissioners, unless, within three months from the time when the Commissioners’ final determination thereof is communicated to him, or such longer time as the Commissioners may allow, a notice requiring a reference under that sub-paragraph has been served on the Commissioners by the person for the purposes of whose application the determination was made.

7U.K.The making by the Commissioners of a payment under the said section 2 determined by reference to the price or value referred to in subsection (3) of that section, or that price or value as reduced by virtue of subsection (4) thereof, shall not be taken as constituting the making by the Commissioners of a final decision under the said subsection (3).

SCHEDULE 2.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F45U.K.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

Section 15.

SCHEDULE 3U.K. Supplementary Provisions as to Duties relating to Betting and Gaming

Part IU.K. Duties relating to Betting

1—5.U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F46

Textual Amendments

6U.K.In Schedule 1 to the M11Betting, Gaming and Lotteries Act 1963 (which relates to the grant, renewal and cancellation of bookmaker’s permits, betting agency permits and betting office licences)—

(a)any reference to the appropriate officer of police—

(i)in paragraph 5, 7(b), 21(3), 25 or 27(1) shall include a reference to the Collector of Customs and Excise for the area in which the relevant premises within the meaning of that Schedule are, or are to be, situated;

(ii)in paragraph 11 or 27(2) shall include a reference to the Commissioners;

(b)in paragraph 34 (which relates to the right to inspect registers of bookmaker’s permits and betting agency permits), the reference to any constable shall include a reference to any officer;

and in considering for the purposes of paragraph 16(1), 17(b) or 27(4)(a) of that Schedule whether a person is or is not a fit and proper person to hold a bookmaker’s permit or, as the case may be, whether the applicant for the grant or renewal of a betting agency permit is or is not a fit and proper person to hold a betting office licence, the appropriate authority shall have regard to any failure of that person or applicant to pay any amount due from him by way of the general betting duty or the pool betting duty.

7—26.U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F47

Textual Amendments

SCHEDULE 4.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F48U.K.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

Section 27

SCHEDULE 5U.K. Amendments of Corporation Tax Acts

1—18.U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F49

Textual Amendments

Transitional relief for company with overseas trading income which is a member of a groupU.K.

19In paragraph 3(3) of Schedule 20 to the M12Finance Act 1965 (which allows to a member of a group of companies as part of the current overspill under section 84(2) of that Act the appropriate part of another member’s excess of current overspill over its relief) for the words “the amount of the relief (before abatement) falling to be given to the other member”there shall be substituted the words “ the amount of the relief under the principal section (calculated apart only from any reduction under the proviso to subsection (1) of that section) falling to be given to the other member ”.

Modifications etc. (not altering text)

C8The text of Ss. 12, 53(7), Sch. 5 para. 19 and Sch. 13 is in the form in which it was originally enacted; it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991.

Marginal Citations

20U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F50

Textual Amendments

Section 27.

SCHEDULE 6U.K. Administration of Corporation Tax Acts

1—13.U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F51

Textual Amendments

Priority of corporation tax and other tax in liquidationU.K.

14U.K.In . . . F52 . . . F53 (priority of debts) the reference to assessed taxes shall include a reference to corporation tax and a reference to capital gains tax chargeable under the Corporation Tax Acts or otherwise recoverable from a company, but nothing in this paragraph shall affect the powers conferred on the Parliament of Northern Ireland by section 16 of the M13Northern Ireland Act 1962.

Textual Amendments

F52Words repealed by Companies Consolidation (Consequential Provisions) Act 1985 (c. 9, SIF 27), s. 29, Sch. 1

F53Words repealed by S.I. 1986/1035 (N.I. 9), art. 24, Sch. 2

Marginal Citations

15—22.U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F54

Textual Amendments

Transitional relief for existing companies with overseas trading incomeU.K.

23(1)If a company fraudulently or negligently—

(a)makes any incorrect return, statement or declaration in connection with any claim for relief under section 84 of the M14Finance Act 1965 (companies with overseas trading income), or

(b)submits to an inspector or any Commissioners any incorrect accounts in connection with such a claim,

the company shall be liable to a penalty not exceeding the aggregate of fifty pounds and the amount or, in the case of fraud, twice the amount of the difference specified in sub-paragraph (2) below.

(2)The difference is that between—

(a)the amount of the relief obtained on the claim, or which would have been obtainable if the return, statement, declaration or accounts had been correct, and

(b)the amount, if any, of relief which is properly due to the company.

(3)[F55Section 99 of the M15Taxes Management Act 1970] (penalty for assisting in making incorrect returns etc.) shall apply in relation to any return, account, statement or declaration made for the purposes of obtaining relief under the said section 84 as it applies to any return, account, statement or declaration made for the purposes of income tax.

(4)[F55Subsections (1) and (2) of section 97 of the Taxes Management Act 1970] shall apply for the purposes of this paragraph as they apply for the purposes of [F55section 95 of that Act].

(5)[F55Section 88 of the Taxes Management Act 1970] (interest on tax recovered to make good loss due to taxpayer’s fault) shall apply in relation to proceedings brought for the recovery of relief under the said section 84 which is or has become excessive, where the bringing of the proceedings is wholly or partly attributable to the fraud, wilful default or neglect of the defendant as it applies in relation to an assessment made for the purpose of making good a loss of tax wholly or partly attributable to the fraud, wilful default or neglect of any person, and subject to any necessary modifications.

(6)The exception in section 30(1) proviso of the M16Limitation Act 1939 for proceedings for the recovery of any tax or duty or interest thereon, and any corresponding exceptions in any other enactment forming part of the law of any part of the United Kingdom and relating to the limitation of actions, shall apply in relation to proceedings for the recovery of relief under the said section 84 which is or has become excessive, or of interest thereon.

(7)Regulations under subsection (7) of the said section 84—

(a)may provide that where any relief given under that section is or becomes excessive, the excess may be recovered by being set off against any income tax, profits tax or corporation tax due to be repaid to the company, or against any relief from any such tax, to which the company is entitled, and

(b)may apply sections 500 to 505 of the M17Income Tax Act 1952 and any provisions of Part III of the Finance Act 1960 in relation to penalties under this paragraph and the recovery of relief under the said section 84 subject to such modifications and exceptions as may be prescribed by the regulations.

(8)This paragraph applies in relation to claims made before or after the passing of this Act.

Textual Amendments

F55Words substituted by Income and Corporation Taxes Act 1970 (c. 10), s. 537(2), Sch. 15 para. 11 Table Pt. I

Marginal Citations

24—27.U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F56

Textual Amendments

SCHEDULE 7.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F57U.K.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

SCHEDULE 8.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F58U.K.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

SCHEDULE 9.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F59U.K.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F59Sch. 9 repealed by Finance Act 1972 (c. 41), Sch. 28 Pt. VI

SCHEDULE 10. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F60U.K.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F60Sch. 10 repealed (with saving) by Capital Gains Tax Act 1979 (c. 14), ss. 157(1), 158, Sch. 6 para. 10(2)(b), Sch. 8

SCHEDULE 11.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F61U.K.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F61Sch. 11 repealed by Finance Act 1972 (c. 41), ss. 122(5), 134(7), Sch. 28 Pts. VIII, IX

SCHEDULE 12.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F62U.K.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

Section 53.

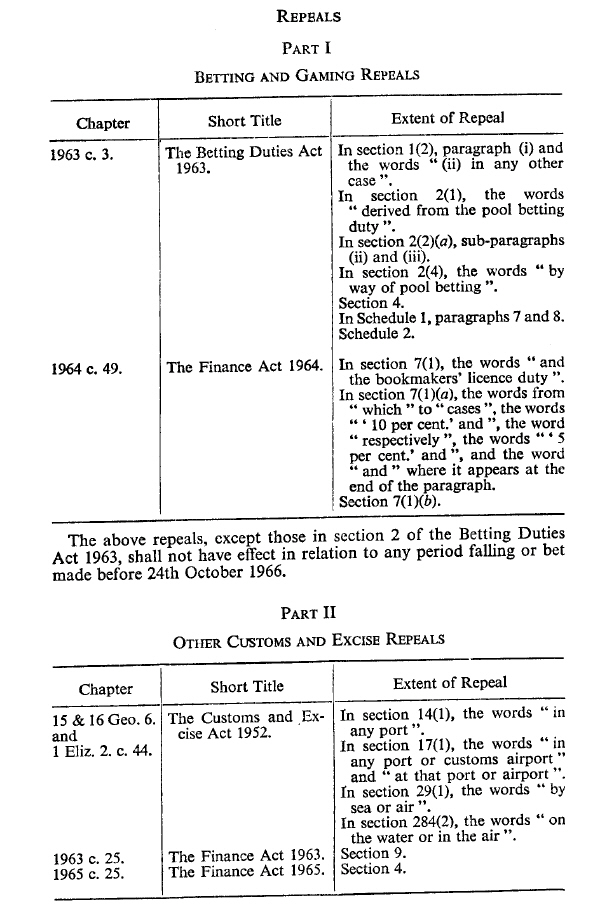

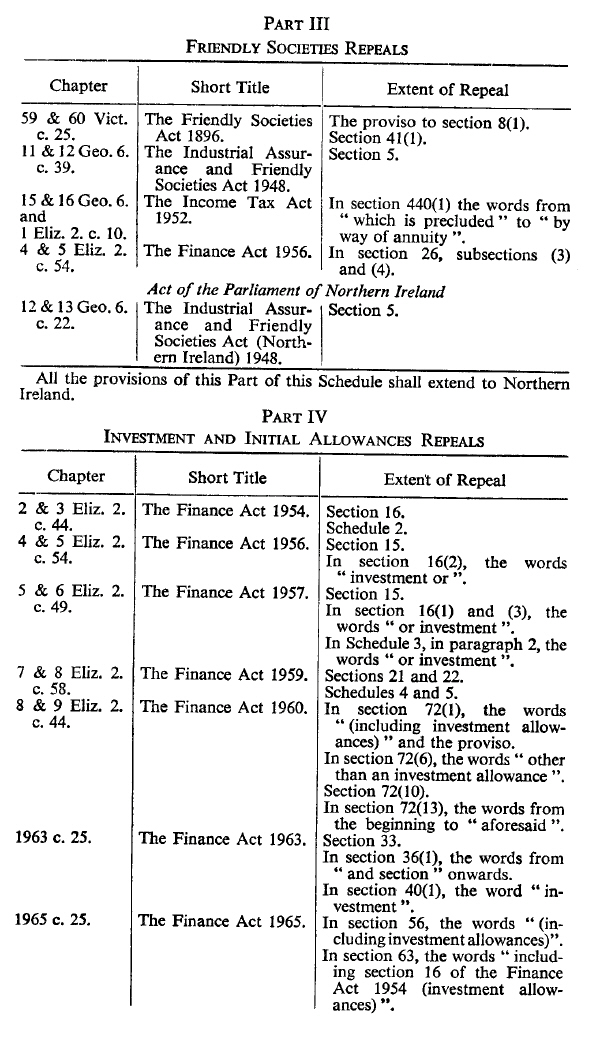

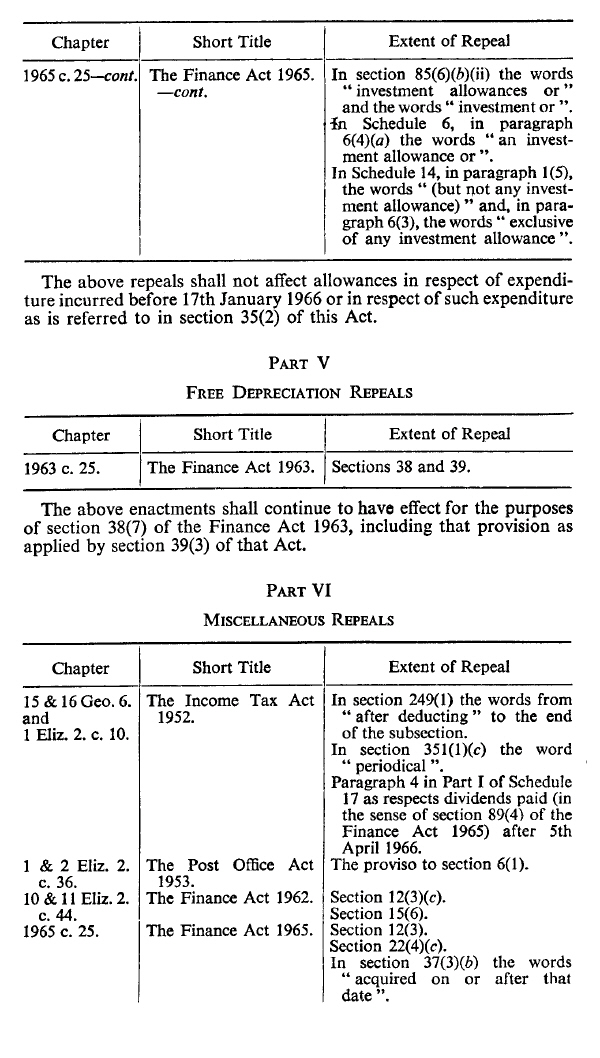

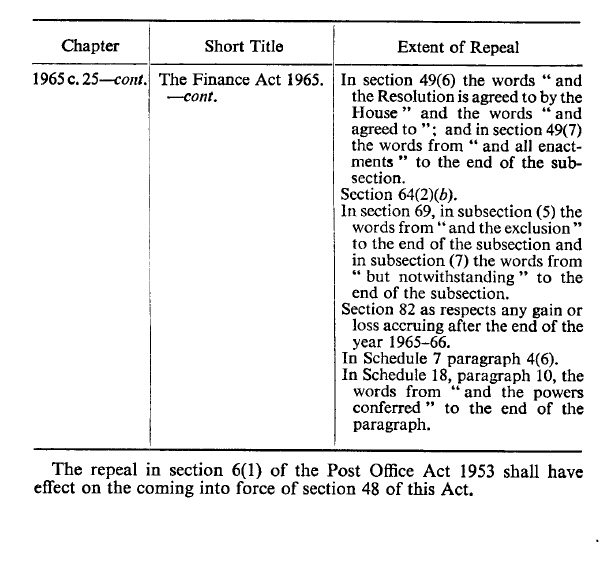

SCHEDULE 13U.K. REPEALS

Modifications etc. (not altering text)

C9The text of Ss. 12, 53(7), Sch. 5 para. 19 and Sch. 13 is in the form in which it was originally enacted; it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991.