- Y Diweddaraf sydd Ar Gael (Diwygiedig)

- Pwynt Penodol mewn Amser (01/07/2013)

- Gwreiddiol (Fel y’i mabwysiadwyd gan yr UE)

Commission Regulation (EC) No 612/2009Dangos y teitl llawn

Commission Regulation (EC) No 612/2009 of 7 July 2009 on laying down common detailed rules for the application of the system of export refunds on agricultural products (Recast)

You are here:

- Rheoliadau yn deillio o’r UE

- 2009 No. 612

- Whole Regulation

- Blaenorol

- Nesaf

Pa Fersiwn

Nodweddion Uwch

- Dangos Graddfa Ddaearyddol(e.e. Lloegr, Cymru, Yr Alban aca Gogledd Iwerddon)

- Dangos Llinell Amser Newidiadau

Rhagor o Adnoddau

PDF o Fersiynau Diwygiedig

- ddiwygiedig 04/09/20141.72 MB

- ddiwygiedig 01/07/20131.72 MB

- ddiwygiedig 01/03/20111.61 MB

- ddiwygiedig 03/12/20101.61 MB

- ddiwygiedig 01/07/20100.86 MB

Legislation originating from the EU

When the UK left the EU, legislation.gov.uk published EU legislation that had been published by the EU up to IP completion day (31 December 2020 11.00 p.m.). On legislation.gov.uk, these items of legislation are kept up-to-date with any amendments made by the UK since then.

Mae hon yn eitem o ddeddfwriaeth sy’n deillio o’r UE

Mae unrhyw newidiadau sydd wedi cael eu gwneud yn barod gan y tîm yn ymddangos yn y cynnwys a chyfeirir atynt gydag anodiadau.Ar ôl y diwrnod ymadael bydd tair fersiwn o’r ddeddfwriaeth yma i’w gwirio at ddibenion gwahanol. Y fersiwn legislation.gov.uk yw’r fersiwn sy’n weithredol yn y Deyrnas Unedig. Y Fersiwn UE sydd ar EUR-lex ar hyn o bryd yw’r fersiwn sy’n weithredol yn yr UE h.y. efallai y bydd arnoch angen y fersiwn hon os byddwch yn gweithredu busnes yn yr UE. EUR-Lex Y fersiwn yn yr archif ar y we yw’r fersiwn swyddogol o’r ddeddfwriaeth fel yr oedd ar y diwrnod ymadael cyn cael ei chyhoeddi ar legislation.gov.uk ac unrhyw newidiadau ac effeithiau a weithredwyd yn y Deyrnas Unedig wedyn. Mae’r archif ar y we hefyd yn cynnwys cyfraith achos a ffurfiau mewn ieithoedd eraill o EUR-Lex. The EU Exit Web Archive legislation_originated_from_EU_p3

Status:

Point in time view as at 01/07/2013.

Changes to legislation:

There are currently no known outstanding effects for the Commission Regulation (EC) No 612/2009.

Changes to Legislation

Revised legislation carried on this site may not be fully up to date. At the current time any known changes or effects made by subsequent legislation have been applied to the text of the legislation you are viewing by the editorial team. Please see ‘Frequently Asked Questions’ for details regarding the timescales for which new effects are identified and recorded on this site.

Commission Regulation (EC) No 612/2009

of 7 July 2009

on laying down common detailed rules for the application of the system of export refunds on agricultural products

(Recast)

THE COMMISSION OF THE EUROPEAN COMMUNITIES,

Having regard to the Treaty establishing the European Community,

Having regard to Council Regulation (EC) No 1234/2007 of 22 October 2007 establishing a common organisation of agricultural markets and on specific provisions for certain agricultural products (Single CMO Regulation)(1), and in particular Articles 170 and 192 in conjunction with Article 4,

Whereas:

(1) Commission Regulation (EC) No 800/1999 of 15 April 1999 laying down common detailed rules for the application of the system of export refunds on agricultural products(2) has been substantially amended several times(3). Since further amendments are to be made, it should be recast in the interests of clarity.

(2) The general rules laid down by the Council provide for the refund to be paid upon proof being furnished that the products have been exported from the Community. Entitlement to the refund is acquired as soon as the products have left the Community market, when a single refund rate applies for all third countries. Where the rate of refund is differentiated according to the destination of the products, entitlement to the refund is conditional on importation into a third country.

(3) The implementation of the Uruguay Round Agreement on Agriculture(4) makes the grant of a refund subject, as a general rule, to the requirement of an export licence comprising the advance fixing of the refund. However, deliveries in the Community for international organisations and for the armed forces, deliveries for victualling and exports of small quantities are special cases and of minor economic importance. For those reasons, provision has been made for a special system without an export licence, in the interests of simplifying such export operations and avoiding an excessive administrative burden on economic operators and the competent authorities.

(4) Within the meaning of this Regulation, the day of export is that during which the customs authorities accept the act by which the declarant shows his willingness to carry out the export of the products for which he seeks the benefit of an export refund. Such act is intended to draw the attention, and in particular the attention of the customs authorities, to the fact that the operation under consideration is being carried out with the aid of Community funds, in order that those customs authorities shall carry out suitable checks. At the time of acceptance, products are placed under customs supervision until their actual export. The date serves as a reference for establishing the quantity, nature and characteristics of the product exported.

(5) In the case of consignments in bulk or in non-standard units, it is recognised that the exact net mass of the products can be known only after loading onto the means of transport. In order to deal with that situation, provision should be made for stating a provisional mass on the export declaration.

(6) As regards the concept of the ‘place of loading’, a great many administrative and commercial circumstances affect the trade in agricultural exports; it is therefore hard to lay down a single rule and the Member States should accordingly be allowed to decide on the most appropriate place for conducting the physical checks of exported agricultural products qualifying for an export refund. To this end, there are particularly good grounds for defining the place of loading differently, depending on whether the goods are loaded in containers or, conversely, in bulk, sacks or cartons, and not subsequently loaded into containers. In duly justified cases, the customs authorities should also be permitted to accept the lodging of an export declaration for agricultural products qualifying for a refund at a customs office other than the office responsible for the place where the products are loaded.

(7) For the sake of the proper application of Commission Regulation (EC) No 1276/2008 of 17 December 2008 on the monitoring by physical checks of exports of agricultural products receiving refunds or other amounts(5), provision should be made so that verification of whether the export declaration matches the agricultural products is carried out at the time of loading of the container, lorry, vessel or other similar container.

(8) Where exports involve frequent consignments of small quantities, provision should be made for a simplified procedure as regards the relevant day to be used for the determination of the rate of refunds.

(9) The operative event, as defined by Commission Regulation (EC) No 1913/2006 of 20 December 2006 laying down detailed rules for the application of the agrimonetary system for the euro in agriculture and amending certain regulations(6), should be adopted.

(10) In order that the concept of ‘exportation from the Community’ may be interpreted consistently, it should be specified that a product is to be regarded as having been exported when it leaves the customs territory of the Community.

(11) It may be necessary for the exporter or transporter to take steps in order to prevent deterioration in the products intended for export during the 60-day period following acceptance of the export declaration and before departure from the customs territory of the Community or before arrival at destination. Freezing is such a step, making it possible to leave the products intact. In order to comply with this requirement, it should be permissible for freezing to be carried out during the said period.

(12) The competent authorities should ensure that products leaving the Community or in transit to a particular destination are in fact those which have undergone the customs export formalities. To this end, when a product crosses the territory of other Member States before leaving the customs territory of the Community or reaching a particular destination, use should be made of the T5 control copy referred to in Annex 63 to Commission Regulation (EEC) No 2454/93 of 2 July 1993 laying down provisions for the implementation of Council Regulation (EEC) No 2913/92 establishing the Community Customs Code(7). However, it seems desirable, in order to simplify administrative procedure, to provide more flexible arrangements than the use of the T5 control copy, in the case of transactions under the simplified Community transit procedures for carriage by rail or large containers under Articles 412 to 442a of Regulation (EEC) No 2454/93, which provides that when a transport operation begins within the Community and is to end outside it, no formalities need to be carried out at the customs office of the frontier station.

(13) In some instance a refund may be claimed in respect of products which have been exported and which have left the customs territory of the Community, but which are returned for the purposes of transhipment or a transit operation before reaching a final destination outside that territory. Such returns may conceivably also occur for reasons other than transport requirements, and more particularly for the purpose of speculation. In such cases compliance with the 60-day time limit for leaving the customs territory of the Community is undermined. In order to avoid such situations, there is a need to define clearly the conditions under which such returns may take place.

(14) The arrangements provided for in this Regulation may be accorded only to products which are in free circulation and which are, if appropriate, of Community origin. In the case of certain compound products the refund is fixed not on the basis of the product itself but by reference to the basic products of which they are composed. In cases where the refund is thus fixed on the basis of one or more components, it is sufficient for the grant of the refund or the relevant part thereof that the component or components in question themselves should meet the requirements, or no longer do so solely because they have been incorporated in other products. In order to take into account the particular status of certain components, a list should be drawn up of products for which the refunds are fixed on the basis of one component.

(15) Articles 23 to 26 of Council Regulation (EEC) No 2913/92 of 12 October 1992 establishing the Community Customs Code(8), define the non-preferential origin of goods. For the grant of export refunds; only products wholly obtained or substantially processed in the Community are deemed to be of Community origin. It is appropriate to clarify, in order to reach uniform application throughout the Member States, that certain mixtures of products do not qualify for refund.

(16) The rate of refund is determined by the tariff classification of a product. The classification may, for certain mixtures, goods put up in sets and composite goods, result in the grant of a higher refund than is economically justified. It is therefore necessary to adopt special provisions for determining the refund applicable to mixtures, goods put up in sets and composite goods.

(17) Where the rate of the refund varies according to the destination of the product, provision should be made for verification that the product has been imported into the third country or countries for which the refund was fixed. Such a measure can be relaxed without difficulty in respect of exports where the refund involved is small and the transaction is such as to offer adequate assurances that the products concerned arrive at their destination. The purpose of the provision is to simplify the administrative work involved in the submission of evidence.

(18) Provision should also be made for products under the returned-goods system to be reintroduced either via the Member State in which the products originated or via the Member State of first export.

(19) Where a single rate of refund applies to all destinations on the day on which the refund is fixed in advance, there is in certain cases a compulsory destination clause. This situation should be treated as a variation of the refund where the rate of the refund applicable on the day on which export takes place is lower than the rate, of the refund applicable on the day of advance fixing, adjusted where appropriate to the day on which export takes place.

(20) Where the rate of refund is differentiated according to the destination of the exported products, proof should be furnished that the product concerned has been imported into a third country. Completion of customs import formalities consists notably in the payment of import duties applicable in order that the product may be marketed in the third country concerned. Considering the diversity of situations prevailing in the importing third countries, it is advisable to accept the production of customs import documents which give assurances that the products exported have arrived at their destination, whilst hindering trade as little as possible.

(21) In order to assist the Community exporters in obtaining proof of arrival at destination, it should be provided that international control and supervisory agencies approved by Member States are to deliver arrival certificates for exported agricultural products of the Community benefiting from a differentiated refund. The approval of these agencies is the responsibility of the Member States which give their approval on a case-by-case basis, in accordance with certain guidelines. It is appropriate to integrate the principal guidelines in this Regulation.

(22) In order to put exports of products enjoying a variable refund, according to destination, on an equal footing with other exports, provision should be made for part of the refund, calculated on the basis of the lowest rate of refund applicable on the day on which export takes place, to be paid as soon as the exporter has furnished proof that the product has left the customs territory of the Community.

(23) In the case of differentiated refunds, if there has been a change of destination, the refund applicable to the actual destination is payable, subject to a ceiling of the level of the amount applicable to the destination fixed in advance. To prevent abuse whereby destinations with the highest rates of refund are selected systematically, a system of penalties should be introduced for changing the destination where the actual rate of refund is less than the rate for the destination fixed in advance. This new provision has consequences for the calculation of the part of the refund payable once the exporter furnishes proof that the product has left the customs territory of the Community.

(24) Articles 23 to 26 of Regulation (EEC) No 2913/92 define the non-preferential origin of goods. It is appropriate in certain cases to apply the criterion covering substantial processing or working laid down in Article 24 to assess whether products have actually reached their destination.

(25) Certain export transactions can lead to deflection of trade. In order to prevent such deflections, payment of the refund should be subject to the condition that the product has not only left the customs territory of the Community but has also been imported into a third country or has undergone substantial processing or working. Moreover, payment of the refund may, in some cases, be subject to the product’s having actually been placed on the market in the importing third country or to its having undergone substantial processing or working.

(26) If a product has been destroyed or damaged before being placed on the market in a third country or undergoing substantial processing the refund is considered not to be due. In such cases the exporter should have the opportunity of submitting evidence showing that the export operation was carried out in such economic conditions as would have allowed the transaction to be carried out in the normal course of events.

(27) Community financing of export operations is unjustified where the operation is not a normal commercial transaction, since it has no real economic purpose and is effected solely to obtain a payment from the Community.

(28) Steps should be taken to prevent Community funds from being allocated for transactions which do not correspond to any objective of the system of export refunds. This risk exists for products attracting export refunds which are subsequently reimported into the Community without having undergone substantial processing or working in a third country and on which reduced or zero duty is paid on reimport rather than the normal rate, pursuant to a preferential agreement or a Council decision. It is appropriate, in order to limit constraints on exporters, to apply such measures to the most sensitive products.

(29) It is appropriate, in order to limit the exporters' uncertainty, to remove the requirement as to repayment of refunds, whenever the product is reimported into the Community more than two years after exportation.

(30) On the one hand, the Member States should be permitted to refuse to grant refunds, or should be able to recover them; in flagrant cases where they note that the transaction is not in line with the aim of the system of export refunds and, on the other hand, no excessive burden should be placed on the national authorities through an obligation to verify systematically all imports.

(31) Products should be of a quality such that they can be marketed on normal terms in the Community. It is appropriate, however, to take account of the specific obligations arising from the standards in force in the third countries of destination.

(32) Certain products can lose the entitlement to the refund when they cease to be of sound and fair marketable quality.

(33) No export levy applies where an export refund has been fixed in advance or determined by tender, since exportation must be effected under the conditions thus fixed in advance or determined by tender. By the same token, it should be provided that where an export is subject to an export levy fixed in advance or determined by tender, exportation is to be effected under the conditions laid down and therefore cannot qualify for an export refund.

(34) To enable exporters to finance their transactions more easily, Member States should be authorised to advance all or part of the amount of the refund as soon as the export declaration or payment declaration is accepted, subject to the provision of security to guarantee repayment of the amount advanced if it should later be found that the refund ought not to have been paid.

(35) Reimbursement of the amount paid in advance of export must be made if there proves to be no right to the export refund or if there was a right to a smaller refund. The reimbursement must include an additional amount to avoid abuses. In case of force majeure the additional amount must not be reimbursed.

(36) Whereas it is clear from Commission Regulation (EEC) No 3002/92 of 16 October 1992 laying down common detailed rules for verifying the use and/or destination of products from intervention(9) that intervention products must reach the prescribed destination; whereas, as a result, such products may not be replaced by equivalent products.

(37) Whereas a time limit should be set for the export of the products concerned.

(38) Whereas no refund is granted if the time limit for export or for submitting the proof required for obtaining payment of the refund is not complied with; whereas measures should be adopted similar to those contained in Commission Regulation (EEC) No 2220/85 of 22 July 1985 laying down common detailed rules for the application of the system of securities for agricultural products(10).

(39) In the Member States products imported from non-member countries for certain uses are exempt from duties. In so far as those outlets are substantial, Community products should be placed on an equal footing with such products from non-member countries. This situation arises particularly in the case of products used in supplying ships and aircraft.

(40) In the case of ship and aircraft supplies and deliveries to the armed forces it is possible to lay down special rules for determining the amount of the refund.

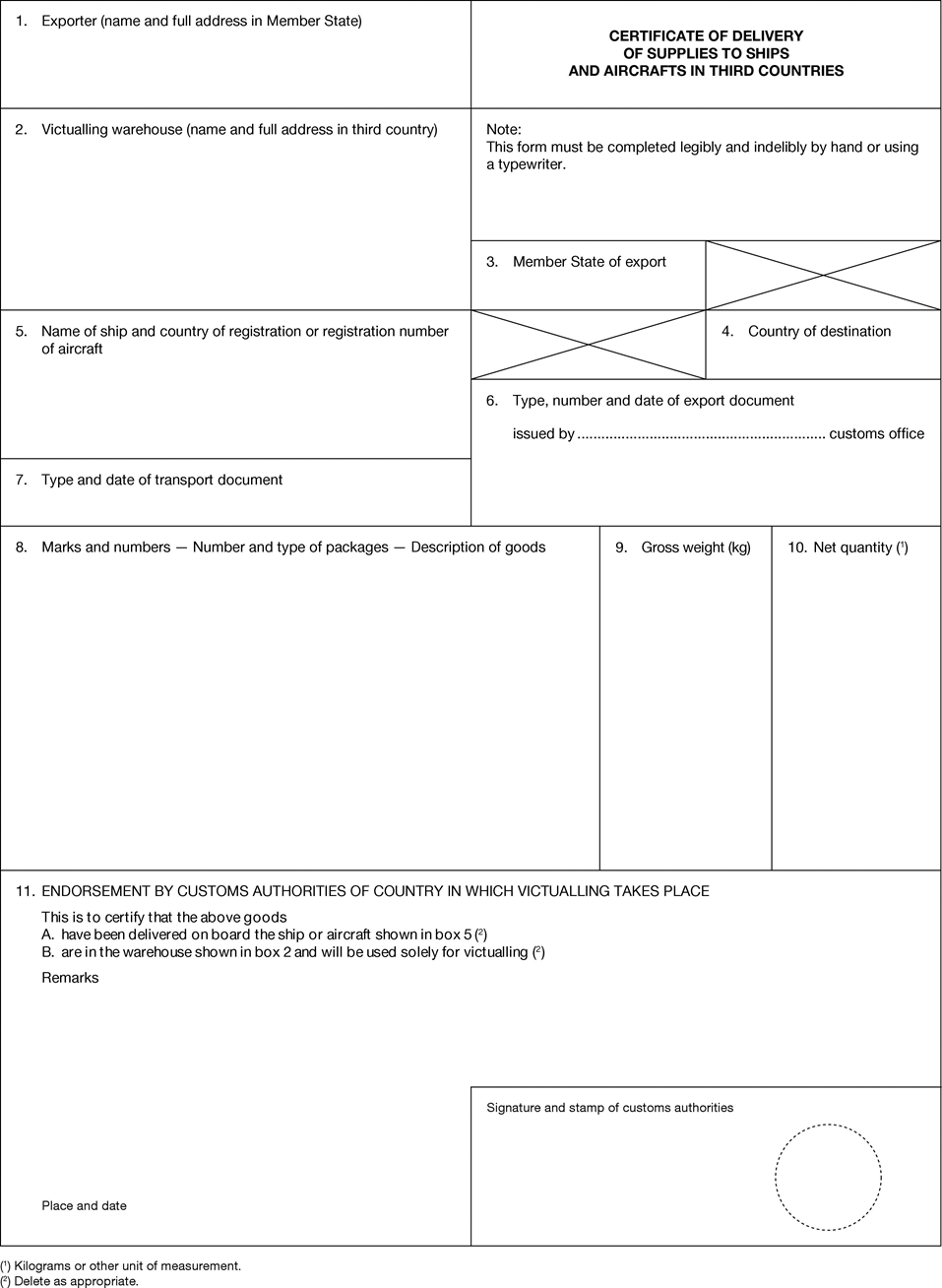

(41) Products taken on board ship as supplies are used for consumption on board. These products, consumed as they are or used in the preparation of food on board, qualify for the refund applicable to unprocessed products. In view of the limited space available on aircraft, food has to be prepared before it is taken on board. With a view to harmonisation, rules should be adopted so as to enable the same refund to be given on agricultural products consumed on board aircraft as are given to those consumed after preparation on board ship.

(42) The business of delivering ship and aircraft supplies is a very specialised trade, warranting special arrangements for the advance of refunds. Products and goods delivered to victualling warehouses must subsequently be delivered for victualling. Deliveries to such warehouses cannot be treated as final export for the purposes of entitlement to refund.

(43) If use is made of these facilities and it is later found that the refund should not have been paid, the exporters will in effect have had the unjustified benefit of an interest-free loan. Measures should therefore be taken to preclude this unwarranted benefit.

(44) In order to maintain the competitiveness of Community goods supplied to platforms in certain areas close to Member States, refunds should be made available at the rate applicable to victualling within the Community. The payment of a refund rate above the lowest in respect of deliveries to a particular destination cannot in any event be justified unless there is no doubt that the goods have reached that destination. The delivery of supplies to platforms in isolated sea areas is necessarily a specialised operation such that it would appear possible to exercise sufficient control over deliveries. Subject to adequate control measures being specified it would appear reasonable to apply to deliveries the rate of refund for victualling within the Community. It is possible to provide for a simplified procedure for deliveries of lesser importance. Since the extent of territorial waters varies according to the Member States between 3 and 12 miles, it would also be reasonable to regard as exports deliveries to all such platforms beyond the three-mile limit.

(45) When a naval vessel belonging to a Member State is victualled on the high seas by a naval supply vessel operating from a Community port, it is possible to obtain certification of that delivery from a competent authority. It would be reasonable to apply to such deliveries the same rate of refund as applies to victualling in a Community port.

(46) It is desirable that agricultural products used in supplying ships and aircraft should qualify for an identical refund whether they are taken on board a ship or an aircraft within the Community or outside it.

(47) Deliveries of such supplies in third countries may be direct or indirect. Methods of supervision appropriate to each type of delivery should be introduced.

(48) Under the provisions of Article 161(3) of Regulation (EEC) No 2913/92 the island of Heligoland does not qualify as a destination for which refunds are payable. The consumption of agricultural products from the Community in the island of Heligoland should be encouraged. The necessary provisions should be adopted for that purpose.

(49) Since the entry into force of the Interim Agreement on trade and customs union between the Community and San Marino(11) the territory of that State no longer forms part of the customs territory of the Community. It follows from Articles 1, 5 and 7 of that Agreement that prices for agricultural products are at the same level within the customs union and that there is, therefore, no economic justification for granting export refunds on Community agricultural products consigned to San Marino.

(50) If an application for repayment or remission of duties is subsequently refused, the products concerned may be eligible for an export refund or will be subject, as the case may be, to an export levy or export charge. Consequently, it is necessary to lay down special provisions.

(51) Generally, armed forces stationed in a non-member country which do not come under the command of that country, international organisations and diplomatic bodies established in a third country obtain their supplies free of import duty. It appears possible to take specific measures — in respect of armed forces which are under the command either of a Member State or an international organisation of which at least one of the Member States is a member, in respect of international organisations of which at least one Member State is a member and in respect of diplomatic bodies — which provide that the proof of import shall be furnished by a special document.

(52) A provision should be introduced whereby the refund is to be paid by the Member State on whose territory the export declaration was accepted.

(53) It may happen that by reason of circumstances beyond the control of the exporter the T5 control copy cannot be produced even though the product has left the customs territory of the Community or has reached a particular destination. Such a situation may impede trade. In such circumstances other documents should be recognised as equivalent.

(54) In the interests of sound administrative practice, applications for payment of the refund, accompanied by all relevant documents, should be required within a reasonable period, save in cases of force majeure and in particular when it has not been possible to comply with the time limit because of administrative delays beyond the control of the exporter.

(55) The period in which the payment of the export refunds is carried out varies from one Member State to the other. It is advisable, in order to avoid distortions to competition, to introduce a maximum uniform period for the payment of these refunds by the paying agencies.

(56) Exports of very small quantities of products are of no economic significance and are liable to overburden the competent authorities unnecessarily. The competent services of the Member States should be given the option of refusing to pay refunds in respect of such exports.

(57) The Community rules provide for the granting of export refunds on the sole basis of objective criteria, in particular as to the quantity, nature and characteristics of the product exported, and its geographical destination. In the light of experience, measures to combat irregularities and notably fraud harmful to the Community budget should be intensified. To that end, provision should be made for the recovery of amounts over-paid and sanctions to encourage exporters to comply with Community rules.

(58) To ensure the correct functioning of the system of export refunds, sanctions should be applied regardless of any subjectivity of the fault. It is nevertheless appropriate to waive sanctions in certain cases, and notably where there is an obvious error recognised by the competent authority, and to provide harsher sanctions in cases of intent. Those measures are necessary, and should be proportionate, sufficiently dissuasive, and uniformly applied throughout the Member States.

(59) In order to ensure equal treatment for exporters in Member States, explicit provision should be made, as far as export refunds are concerned, for any amount over-paid to be reimbursed with interest by the beneficiary, and the procedure for payment should be laid down. In order better to protect the Community’s financial interest, provision should be made, where the right to a refund is transferred, for that obligation to be extended to the transferee. Sums and interest recovered, and sanctions collected, should be credited to the European Agricultural Guarantee Fund (EAGF) in accordance with the principles laid down in Article 9 of Council Regulation (EC) No 1290/2005 of 21 June 2005 on the financing of the common agricultural policy(12).

(60) In order to ensure uniform application throughout the Community of the principle of legitimate expectation where amounts over-paid are recovered, the conditions under which that principle may be invoked should be laid down without prejudice to the treatment of irregular expenditure as provided for, in particular, in Articles 9 and 31 of Regulation (EC) No 1290/2005.

(61) The exporter should be responsible in particular for the acts of any third party which could make it possible to obtain improperly the documents needed for payment of the refund.

(62) The measures provided for in this Regulation are in accordance with the opinion of the Management Committee for the Common Organisation of Agricultural Markets,

HAS ADOPTED THIS REGULATION:

TITLE IU.K.SCOPE AND DEFINITIONS

Article 1U.K.

Without prejudice to derogations provided for in Community regulations specific to certain products, this Regulation lays down common detailed rules for the application of the system of export refunds, hereinafter referred to as ‘refunds’:

(a)

for the products of the sectors referred to in Article 162(1) of Regulation (EC) No 1234/2007;

(b)

provided for in Article 63 of Council Regulation (EC) No 1493/1999(13).

Article 2U.K.

1.For the purposes of this Regulation:

(a)‘products’ means the products referred to in Article 1, and goods,

(a)‘basic products’ means products intended for export after processing into processed products or into goods; goods intended for export after processing shall also be regarded as basic products,

‘processed products’ means products obtained from the processing of basic products and on which refunds are payable,

‘goods’ means the goods listed in Annex II to Commission Regulation (EC) No 1043/2005(14);

(b)‘import duties’ means customs duties, charges having equivalent effect and other import charges provided for under the common agricultural policy or under specific trade arrangements applicable to certain goods resulting from the processing of agricultural products;

(c)‘Member State of export’ means the Member State in which the export declaration is accepted;

(d)‘advance fixing of the refund’ means the fixing of the refund on the day of submission of the application for an export licence or advance-fixing certificate, the rate being adjusted by any increase or corrective amount applicable to the refund;

(e)‘differentiated refund’ means:

(e)more than one rate of refund is fixed on the same product depending on the third country of destination, or

one or more rates of refund are fixed on the same product according to the third country of destination, no rate being fixed for one or more third countries;

(f)‘differentiated part of the refund’ means the part of the refund obtained by deducting from the total amount of the refund applicable the refund paid or to be paid on the basis of proof of exit from the customs territory of the Community, calculated in accordance with Article 25;

(g)‘export’ means the completing of customs export formalities followed by the exit of the products from the customs territory of the Community;

(h)‘T5 control copy’ means the document referred to in Articles 912a to 912g of Regulation (EEC) No 2454/93;

(i)‘exporter’ means the natural or legal person who is entitled to the refund. Where an export licence with advance fixing of the refund must or may be used, the holder or, where appropriate, the transferee of the licence shall be entitled to the refund. The exporter for customs purposes may be different from the exporter within the meaning of this Regulation, given the relationship between economic operators under private law, except where otherwise stated in special provisions laid down in Regulation (EC) No 1234/2007 or its implementing provisions;

(j)‘advance on refund’ means an amount equal at most to the refund paid from the time of acceptation of the export declaration;

(k)‘rate of refund determined by invitation to tender’ means the refund quoted by the exporter and accepted by tender;

(l)‘customs territory of the Community’ means the territories referred to in Article 3 of Regulation (EEC) No 2913/92;

(m)‘refund nomenclature’ means the agricultural product nomenclature for export refunds in accordance with Commission Regulation (EEC) No 3846/87(15);

(n)‘export licence’ means the document referred to in Article 1 of Commission Regulation (EC) No 376/2008(16);

(o)‘remote refund zone’ means all destinations for which the same differentiated, non-zero part of the refund applies for a particular product except the excluded destinations for that product as set out in Annex I;

(p)‘hinterland country’ means a third country without its own sea port which is served by the sea port of another third country;

(q)‘transhipment’ means the movement of products from one means of transport to another with a view to their immediate transport to the third country or territory of destination.

2.For the purposes of this Regulation, refunds determined by invitation to tender shall rank as refunds fixed in advance.

3.Where an export declaration covers several different refund nomenclature codes or Combined Nomenclature codes, the entries relating to each code shall be deemed to be separate declarations.

TITLE IIU.K.EXPORTS TO THIRD COUNTRIES

CHAPTER 1U.K.Entitlement to refunds

Section 1U.K.General provisions

Article 3U.K.

Without prejudice to Articles 25, 27 and 28 of this Regulation and Article 4(3) of Council Regulation (EC, Euratom) No 2988/95(17), entitlement to the refund is acquired:

on leaving the customs territory of the Community, when a single refund rate applies for all third countries,

on importation into a specific third country, when a differentiated refund applies for that third country.

Article 4U.K.

1.Entitlement to the refund shall be conditional upon the presentation of an export licence with advance fixing of the refund, except in the case of exports of goods.

However, no licence shall be required to obtain a refund:

where the quantities exported per export declaration are less than or equal to the quantities set out in Annex II to Regulation (EC) No 376/2008,

in cases covered by Articles 6, 33, 37, 41, 42 and Article 43(1),

for deliveries to Member States’ armed forces stationed in non-member countries.

2.Notwithstanding paragraph 1, an export licence with advance fixing of the refund shall also be valid for the exportation of a product covered by a 12 -digit product code other than that indicated in box 16 of the licence if both products belong:

to the same category as referred to in the second subparagraph of Article 13(1) of Regulation (EC) No 376/2008, or

to the same product group, provided that such product groups have been defined for this purpose in accordance with the procedure referred to in Article 195 of Regulation (EC) No 1234/2007.

In the cases set out in the first subparagraph, the following further conditions shall apply:

if the rate of refund corresponding to the actual product is equal to or higher than the rate applicable to the product shown in box 16 of the licence, the latter rate shall apply,

if the rate of refund corresponding to the actual product is lower than the rate applicable to the product indicated in box 16 of the licence, the refund to be paid shall be that obtained by the application of the rate corresponding to the actual product, less, save in cases of force majeure, 20 % of the difference between the refund corresponding to the product indicated in box 16 of the licence and the refund for the actual product.

Where the second indent of the second subparagraph and point (b) of Article 25(3) apply, the reduction to be applied to the refund corresponding to the actual product and the actual destination shall be calculated on the difference between the refund corresponding to the product and destination indicated on the licence and the refund corresponding to the actual product and destination.

For the purpose of applying this paragraph, the rates of refund to be taken into consideration shall be those valid on the day on which the licence application is lodged. Where necessary those rates shall be adjusted on the day of acceptance of the export declaration.

3.Where paragraphs 1 or 2 and Article 48 apply to the same export operation, the amount resulting from paragraphs 1 or 2 shall be reduced by the amount of the penalty referred to in Article 48.

Article 5U.K.

1.‘Day of export’ means the day on which the customs authorities accept the export declaration stating that a refund is to be applied for.

2.The date of acceptance of the export declaration shall determine:

(a)the rate of refund applicable where the refund is not fixed in advance;

(b)any adjustments to be made to the rate of refund where it is so fixed in advance;

(c)the quantity, nature and characteristics of the product exported.

3.Any other act having the same effect in law as acceptance of the export declaration shall be deemed equivalent to such acceptance.

4.The document used on export to qualify for a refund shall include all information necessary to calculate the refund, and in particular:

(a)for products:

(a)a description, simplified where appropriate, of the products in accordance with the export refund nomenclature, together with the refund nomenclature code and, where necessary to calculate the refund, the composition of the products concerned or a reference thereto,

the net mass of the products or, where applicable, the quantity expressed in the unit of measurement to be used when calculating the refund;

(b)in the case of goods, the provisions of Regulation (EC) No 1043/2005 shall apply.

5.At the time of acceptance or of the act envisaged in paragraph 3, the products shall be placed under customs control in accordance with Article 4(13) and (14) of Regulation (EEC) No 2913/92 until they leave the customs territory of the Community.

6.By way of derogation from Article 282(2) of Regulation (EEC) No 2454/93, the authorisation to make the export declaration in a simplified form may stipulate that the simplified declaration shall contain an estimate of the net mass of products exported in bulk or in non-standard units, where the exact quantity can only be established once loading onto the means of transport is completed.

The additional declaration indicating the exact net mass must be lodged once loading is completed. It must be accompanied by documentary evidence of the exact net mass loaded.

No refund shall be granted for quantities exceeding 110 % of the estimated net mass. Where the mass actually loaded is less than 90 % of the estimated net mass, the refund for the net mass actually loaded will be reduced by 10 % of the difference between the refund corresponding to 90 % of the estimated net mass and the refund corresponding to the mass actually loaded. However, where export occurs by sea or navigable inland waterway, if the exporter can supply signed proof from the person responsible for the means of transport that constraints peculiar to this type of transport or alternatively overloading on the part of other exporters have prevented the loading of all his goods, the refund shall be paid for the net mass actually loaded. This subparagraph shall apply if the exporter has used the local clearance procedure provided for in Article 283 of Regulation (EEC) No 2454/93, provided that the customs authorities have authorised the correction of the records in which the exported products were entered.

The following shall be considered non-standard units: live animals, (half-) carcases, quarters, fore-ends, legs, shoulders, bellies and loins.

7.All persons exporting products for which they claim a refund shall be required to:

(a)lodge the export declaration with the competent customs office in the place where the products are to be loaded for export transport;

(b)inform that customs office at least 24 hours prior to starting the loading operations and indicate the anticipated duration of loading. The competent authorities may stipulate a time limit other than 24 hours.

The following may be considered as the place of loading for the transport of products intended for export:

(a)in the case of products exported in containers, the place where they are loaded into the containers;

(b)in the case of products exported in bulk, sacks, cartons, boxes, bottles, etc. and not loaded into containers, the place where the means of transport, in which they will leave the customs territory of the Community, is loaded.

The competent customs office may authorise the loading operations after having accepted the export declaration, before expiry of the time limit referred to in point (b) of the first paragraph.

The products shall be identified by appropriate means before the indicated time for starting loading. The competent customs office must be able to make physical checks and identify the goods for transport to the office of exit from the customs territory of the Community.

If the first subparagraph cannot be applied for administrative or other duly justified reasons, the export declaration may be lodged only with a competent customs office in the Member State concerned and, where a physical check is carried out in accordance with Regulation (EC) No 1276/2008, any goods presented must be fully unloaded. However, the goods do not have to be unloaded completely if the competent authorities can perform a thorough physical check.

8.Goods for which export refunds are claimed shall be sealed by, or under the control of, the customs office of export. Article 340a and paragraphs 2, 3 and 4 of Article 357 of Regulation (EEC) No 2454/93 shall apply mutatis mutandis.

[F1Before affixing seals, the customs office of export shall visually check the conformity of the products with the export declarations. The number of visual checks shall not be less than 10 % of the number of export declarations, other than those in respect of which the products covered by them have been physically checked or selected for a physical check under Article 3 of Regulation (EC) No 1276/2008. The customs office shall note this check in box D of the T5 control copy or equivalent document by using the control code as defined in Article 2(m) of Regulation (EC) No 1276/2008 and as set out in Annex II to this Regulation.]

Textual Amendments

F1 Substituted by Commission Regulation (EU) No 278/2010 of 31 March 2010 amending Regulation (EC) No 1276/2008 on the monitoring by physical checks of exports of agricultural products receiving refunds or other amounts and Regulation (EC) No 612/2009 on laying down common detailed rules for the application of the system of export refunds on agricultural products.

Article 6U.K.

By way of derogation from Article 5(2), where the quantities exported do not exceed 5 000 kilograms of product per refund nomenclature code in the case of cereals or 500 kilograms per refund nomenclature or Combined Nomenclature code in the case of other products and where such exports involve frequent consignments, the Member State may allow the last day of the month to be used to determine the refund applicable or, if the refund is fixed in advance, any adjustments to be made thereto.

Where the refund is fixed in advance or is determined by invitation to tender, the licence shall be valid on the last day of the month of export.

Exporters authorised to make use of this option shall not apply the normal procedure for the quantities set out in the first paragraph.

The operative event for the exchange rate applicable to the refund shall be that referred to in Article 1(1) of Regulation (EC) No 1913/2006.

Article 7U.K.

1.Without prejudice to Articles 15 and 27, payment of the refund shall be conditional upon proof being furnished that the products covered by accepted export declarations have left the customs territory of the Community in their unaltered state within 60 days of such acceptance.

However, the quantities of products taken as samples at the time of completion of customs export formalities and not returned subsequently shall be regarded as not having been removed from the products' net mass from which they were actually taken.

2.For the purposes of this Regulation, catering supplies delivered to drilling or extraction rigs as defined in point (a) of Article 41(1) shall be deemed to have left the customs territory of the Community.

3.Freezing shall be without prejudice to compliance with paragraph 1.

This shall also apply to repackaging, provided that such repackaging does not result in a change of the product code in the refund nomenclature or the code of the goods in the Combined Nomenclature. Repackaging may take place only after the customs authorities have given their agreement.

Where repackaging takes place, the T5 control copy shall be completed accordingly.

The affixing or changing of labels may be authorised under the same conditions as repackaging under the second and third subparagraphs.

4.Where for reasons of force majeure an exporter cannot comply with the time limit laid down in paragraph 1, that time limit may, at the exporter’s request, be extended for such period as the competent authorities of the Member State of export deem necessary in the circumstances.

Article 8U.K.

If, before leaving the customs territory of the Community, a product covered by an accepted customs declaration crosses Community territory other than that of the Member State of export, proof that the product has left the customs territory of the Community shall be furnished by means of the duly endorsed original of the T5 control copy.

Boxes 33, 103, 104 and, where appropriate, 105 of the control copy shall be completed. The appropriate entry shall be, made in Box 104.

In case refunds are applied for, box 107 shall show one of the entries listed in Annex III.

Article 9U.K.

The exporter shall mention the rate of export refunds in EUR per unit of products or goods on the date of advanced fixing, as mentioned in the export license or certificate of Regulation (EC) No 376/2008 or the refund certificate of Chapter III of Regulation (EC) No 1043/2005, in box 44 of the export declaration or its electronic equivalent and in box 106 of the control copy T5 or its equivalent. If the export refunds have not been fixed in advance, information on previous refund payments for the same products or goods not older than 12 months may be used. If the product or good to be exported does not cross the border of another Member State and if the national currency is not the euro, the rates of refunds may be mentioned in national currency.

The competent authorities may exempt the exporter of the requirements provided for in the first paragraph if the administration operates a system by which the services concerned are informed with the same information.

The exporter may choose to mention one of the entries listed in Annex IV for export declarations and T5 control copies and equivalent documents covering an amount of export refunds less than EUR 1 000.

Article 10U.K.

1.For the purpose of granting refunds in the case of export by sea, the following special provisions shall apply:

(a)Where the T5 control copy or the national document proving that the products have left the customs territory of the Community has been endorsed by the competent authorities, the products concerned may not return or remain in temporary storage or under any customs-approved treatment or use on the customs territory of the Community, unless for the purposes of transhipment in any other port(s) located in the same or another Member State for not more than 28 days, except in cases of force majeure. That time limit shall not apply where the products have left the final port in the customs territory of the Community definitely within the original 60-day time limit.

(b)Refunds shall be paid subject to presentation to the paying agency of:

(b)a declaration by the exporter that the products are not to be transhipped in another Community port, or

proof of compliance with point (a). Such proof shall consist in particular of the transport document(s), or a copy or photocopy thereof, covering the products from departure from the first port at which the documents referred to in point (a) were endorsed, to arrival in the third country in which they are to be unloaded.

Declarations as referred to in the first indent shall be subject to suitable spot checks by the paying agency. The proof referred to in the second indent shall be required for that purpose.

In cases of export by vessels operating a direct shipping service to a third country port without calling at any other Community port, Member States may apply a simplified procedure for the purpose of the first indent.

(c)As an alternative to the conditions set out in point (b), the Member State of destination of the T5 control copy or the Member State where a national document is used as proof may stipulate that the T5 control copy or the national document proving that the products have left the customs territory of the Community is to be endorsed only on presentation of a transport document specifying a final destination outside the customs territory of the Community.

In such cases, one of the entries listed in Annex V shall be added by the competent authorities of the Member State of destination of the T5 control copy or the Member State where a national document is used as proof under the heading ‘Remarks’ in the section headed ‘Control of use and/or destination’ on the T5 control copy or under the corresponding heading of the national document.

Compliance with this point shall be verified by suitable spot checks conducted by the paying agency.

(d)Where it is found that the conditions set out in point (a) have not been complied with, for the purposes of Article 47 the day, or days, by which the 28-day time limit is exceeded shall be deemed to be days by which the time limit laid down in Article 7 is exceeded.

2.For the purpose of granting refunds in the case of export by road, by inland waterway or by rail, the following special provisions shall apply:

(a)Where the T5 control copy or the national document proving that the products have left the customs territory of the Community has been endorsed by the competent authorities, the products concerned may not return or remain in temporary storage or under any customs-approved treatment or use on the customs territory of the Community, unless for the purposes of transit operation for not more than 28 days, except in cases of force majeure. That time limit shall not apply where the products have left the customs territory of the Community definitely within the original 60-day time limit.

(b)Compliance with point (a) shall be verified by suitable spot checks conducted by the paying agency. In such cases the transport documents covering the products up to their arrival in the third country in which they are to be unloaded, shall be required.

In cases where it is found that the conditions set out in point (a) have not been complied with, for the purpose of Article 47 the day, or days, by which the 28-day time limit is exceeded shall be deemed to be days by which the time limit laid down in Article 7 is exceeded.

If both the 60-day time limit laid down in Article 7(1) and the 28-day time limit laid down in point (a) are exceeded, the amount by which the refund is to be reduced or the part of the security to be forfeited shall be equal to that due to the greater of the two overruns.

3.For the purpose of granting refunds in the case of export by air, the following special provisions shall apply:

(a)The T5 control copy or the national document proving that the products have left the customs territory of the Community may be endorsed by the competent authorities only on presentation of a transport document indicating a final destination outside the customs territory of the Community.

(b)In cases where it is found that, after completion of the formalities referred to in point (a), the products have remained, except in cases of force majeure, for more than 28 days for the purpose of transhipment in one or more other airports in the customs territory of the Community, the day, or days, by which the 28-day time limit is exceeded shall, for the purposes of Article 47, be deemed days by which the time limit laid down in Article 7 is exceeded.

If both the 60-day time limit stipulated in Article 7(1) and the 28-day time limit stipulated in this point are exceeded, the amount by which the refund is to be reduced or the part of the security to be forfeited shall be equal to that due to the greater of the two overruns.

(c)Compliance with this paragraph shall be verified by suitable spot checks conducted by the paying agency.

(d)The 28-day time limit laid down in point (b) shall not apply where the products concerned have left the customs territory of the Community definitively within the original 60-day time limit.

Article 11U.K.

1.Where the product is placed, in the Member State of export, under one of the simplified Community transit procedures for carriage of goods by rail or large containers provided for in Articles 412 to 442a of Regulation (EEC) No 2454/93 to a station of destination or for delivery to a consignee outside the customs territory of the Community, payment of the refund shall not be conditional on production of the T5 control copy.

2.For the purposes of paragraph 1, the competent customs office shall ensure that the words ‘Departure from the customs territory of the Community under the simplified Community transit procedure for carriage by rail or large containers’ are entered on the document issued with a view to payment of the refund.

3.The customs office where the products are placed under a procedure as referred to in paragraph 1 may not permit the contract of carriage to be amended so that carriage ends within the Community unless it is established that:

where the refund has been paid, such refund has been reimbursed, or

the necessary steps have been taken by the authorities concerned to ensure that the refund is not paid.

However, where the refund has been paid pursuant to paragraph 1 and the product has not left the customs territory of the Community within the time limit laid down, the competent customs office shall so inform the agency responsible for paying the refund and shall provide it as soon as possible with all the necessary particulars. In such cases the refund shall be regarded as over-paid.

4.Where a product circulating under the external Community transit procedure, set out in Articles 91 to 97 of Regulation (EC) No 2913/92, or the common transit procedure, set out in the Convention on a common transit procedure(18), is placed in a Member State other than that of export under a procedure as provided for in paragraph 1 for carriage to a station of destination or delivery to a consignee outside the customs territory of the Community, the customs office at which the product has been placed under a procedure as referred to above shall insert one of the entries listed in Annex VI under ‘Remarks’ in the section headed ‘Control of use and/or destination’ on the back of the original of the T5 control copy.

Where the contract of carriage is amended so that carriage terminates within the Community, paragraph 3 shall apply mutatis mutandis.

5.Where a product is taken over by the railways in the Member State of export or in another Member State and circulates under the external Community transit procedure or the common transit procedure under a contract of carriage for combined road-rail transport by rail to a destination outside the customs territory of the Community, the customs office competent for or nearest to the rail terminal at which the product is taken over by the railways shall insert one of the entries listed in Annex VII under ‘Remarks’ in the section headed ‘Control of use and/or destination’ on the back of the original of the T5 control copy.

A contract of carriage for combined road-rail transport which is amended so that carriage terminates within the Community instead of outside may not be performed by the railway authorities without prior authorisation from the office of departure. In such cases, paragraph 3 shall apply mutatis mutandis.

Article 12U.K.

1.Refunds shall be granted for products which, irrespective of the customs situation regarding the packaging, are in free circulation and of Community origin.

However, for sugar products referred to in Article 162(1)(a)(iii) and (b) of Regulation (EC) No 1234/2007, refunds can be granted when they are only in free circulation.

[F2Refunds shall not be granted for products which are used as equivalent goods within the meaning of Article 114(2)(e) of Regulation (EEC) No 2913/92.]

2.For the grant of the refund, products are of Community origin if they are wholly obtained in the Community or if they underwent their last substantial processing or working in the Community in accordance with the provisions of Article 23 or 24 of Regulation (EEC) No 2913/92.

However, without prejudice to paragraph 4, products obtained from the following shall not qualify for refund:

(a)materials originating in the Community; and

(b)agricultural materials covered by the regulations referred to in Article 1 imported from third countries which did not undergo a substantial processing in the Community.

3.Where the refund is granted on condition that the product is of Community origin, exporters shall declare the origin as defined in paragraph 2 in accordance with the Community rules in force.

4.Where compound products qualifying for a refund on one or more of their ingredients are exported, the refund on the latter shall be granted subject to its or their compliance with the condition set out in paragraph 1.

The refund shall also be granted where the ingredient, or ingredients, in respect of which the refund is claimed were originally of Community origin and/or in free circulation as provided for in paragraph 1 and are no longer in free circulation on account solely of their incorporation in other products.

5.For the purposes of paragraph 4, refunds on the following shall be deemed to be refunds fixed on the basis of an ingredient:

(a)products of the cereals, eggs, rice, sugar, milk and milk products sectors, exported in the form of goods referred to in Annex II to Regulation (EC) No 1043/2005;

(b)white sugar and raw sugar falling within CN code 1701, isoglucose falling within CN codes 1702 30 10, 1702 40 10, 1702 60 10 and 1702 90 30 and beet and cane syrups falling within CN codes 1702 60 95 and 1702 90 95, used in products referred to in point (j) of Article 1 of Regulation (EC) No 1234/2007;

(c)milk and milk products and sugar exported in the form of products falling within CN codes 0402 10 91 to 99, 0402 29, 0402 99, 0403 10 31 to 39, 0403 90 31 to 39, 0403 90 61 to 69, 0404 10 26 to 38, 0404 10 72 to 84 and 0404 90 81 to 89 and exported in the form of products falling within CN code 0406 30 which are not products originating in Member States or products coming from third countries which are in free circulation in Member States.

Textual Amendments

Article 13U.K.

1.The rate of refund applicable to mixtures falling within Chapters 2, 10 and 11 of the Combined Nomenclature shall be that applicable:

(a)in the case of mixtures one ingredient of which accounts for at least 90 % by weight, to that ingredient;

(b)in the case of other mixtures, to the ingredient to which the lowest refund rate applies. In cases where one or more of the ingredients does not qualify for a refund, no refund shall be payable on such mixtures.

2.For the purposes of calculating the refunds applicable to goods put up in sets and composite goods, each component shall be considered to be a separate product.

3.Paragraphs 1 and 2 shall not apply to mixtures, goods put up in sets and composite goods for which special rules of calculation are laid down.

Article 14U.K.

The provisions relating to the advance fixing of refunds and to adjustments to be made thereto shall apply only to products for which a rate of refund equal to or greater than zero is fixed.

Section 2U.K.Differentiated refunds

Article 15U.K.

Where the rate of refund varies according to destination, refunds shall be paid subject to the additional conditions laid down under Articles 16 and 17.

Article 16U.K.

1.Within 12 months of the date of acceptance of the export declaration, the products shall:

(a)be imported in their unaltered state into the third country or one of the third countries for which the refund applies; or

(b)be unloaded in their unaltered state in a remote refund zone for which the refund applies pursuant to the conditions set out in Article 24(1)(b) and (2).

However, an extension to the time limit may be granted in accordance with Article 46.

2.Products shall be considered to have been imported in their unaltered state if there is no evidence whatsoever of processing.

However the following operations conducted with a view to the safe keeping of the products may be carried out prior to import and shall be without prejudice to compliance with paragraph 1:

(a)stocktaking;

(b)the affixing of marks, seals, labels or other similar distinguishing signs to the products or goods or to their packaging, provided that this entails no risk of implying that the products originate elsewhere;

(c)altering the marks and numbers on packages or changing of labels, provided that this entails no risk of implying that the products originate elsewhere;

(d)packaging, unpacking, changing packaging or repairing packaging, provided that this entails no risk of implying that the products originate elsewhere;

(e)airing;

(f)chilling; and

(g)freezing.

In addition, products processed prior to import shall be considered to have been imported in their unaltered state provided that processing takes place in the third country into which all the products resulting from such processing are imported.

3.A product shall be considered to have been imported when the customs import formalities, in particular those concerning the collection of import duties in the third country have been completed.

4.The differentiated part of the refund shall be paid on the mass of the products which underwent the customs formalities for import in the third country; however, no account shall be taken of any variations in mass that might occur in the course of transport as a result of natural causes and which are recognised by the competent authorities or due to samples taken in accordance with the provisions of the second subparagraph of Article 7(1).

Article 17U.K.

1.Proof that customs formalities for importation have been completed shall, as the exporter chooses, be furnished by one of the following documents:

(a)the customs document, a copy or photocopy thereof, or a printout of equivalent information recorded electronically by the competent customs authority; such copy, photocopy or printout shall be certified as being a true copy or printout by one of the following:

(i)

the body which endorsed the original document or electronically recorded the equivalent information;

(ii)

an official agency of the third country concerned;

(iii)

an official agency of a Member State in the third country concerned;

(iv)

an agency responsible for paying the refund;

(b)a certificate of unloading and importation drawn up by an approved international control and supervisory agency (hereinafter referred to as ‘SA’) in accordance with the rules set out in Annex VIII, Chapter III, using the model set out in Annex IX; the date and number of the customs document of import must appear on the certificate concerned.

At the request of the exporter, a paying agency may waive the certification requirement referred to in point (a) of the first subparagraph where it is able to verify that customs formalities for importation have been completed by accessing electronically recorded information held by or on behalf of the competent authorities of the third country.

2.Where the exporter cannot obtain the document chosen in accordance with points (a) or (b) of paragraph 1 even after taking the appropriate steps, or where there are doubts as to the authenticity of the document furnished, or its accuracy in all respects, proof of completion of customs formalities for importation may be furnished by one or more of the following documents:

(a)a copy of the unloading document issued or endorsed in the third country for which a refund is payable;

(b)a certificate of unloading issued by an official agency of a Member State established in, or competent for, the country of destination, in accordance with the requirements and in conformity with the model set out in Annex X, certifying in addition that the product has left the place of unloading or at least that, to its knowledge, the product has not subsequently been loaded for re-exportation;

(c)a certificate of unloading drawn up by an approved SA in accordance with the rules set out in Annex VIII, Chapter III, using the model set out in Annex XI, certifying in addition that the product has left the place of unloading or at least that, to its knowledge, the product has not subsequently been loaded for re-exportation;

(d)a bank document issued by approved intermediaries established in the Community, certifying, in the case of the third countries listed in Annex XII, that payment for the exports in question has been credited to the exporter’s account with them;

(e)a certificate of acceptance of delivery issued by an official agency of the third country concerned, where the goods are purchased by that country or by an official agency of that country or where the goods constitute food aid;

(f)a statement of acceptance of delivery issued either by an international organisation or a humanitarian organisation approved by the Member State of exportation, where the goods constitute food aid;

(g)a statement of acceptance of delivery issued by a body in a third country whose invitations to tender are acceptable under Article 47 of Regulation (EC) No 376/2008 where the goods are purchased by that body.

3.Exporters shall in all cases produce a copy or photocopy of the transport documents, which shall relate to the transport of the products for which the export declaration was made.

At the exporter’s request, in the case of container transport by sea, a Member State may accept information equivalent to that contained in transport documents if they are generated by an information system managed by a third party responsible for the transport of the containers to the place of destination provided that the third party specialises in such operations and the information system security is approved by the Member State as meeting the criteria laid down in the version applicable to the period concerned of one of the internationally accepted standards set out in point 3(B) of Annex I to Commission Regulation (EC) No 885/2006(19).

4.The Commission may, in accordance with the procedure referred to in Article 195 of Regulation (EC) No 1234/2007 provide, in certain specific cases to be determined, for proof of import as referred to in paragraphs 1 and 2 of this Article to be furnished by a specific document or in any other way.

Article 18U.K.

1.An SA wishing to issue certificates as referred to in Article 17(1)(b) and (2)(c) has to be approved by the competent authority of the Member State where it has its registered office.

2.The SA shall be approved at its request for a renewable period of three years, if it fulfils the conditions set out in Annex VIII, Chapter I. The approval shall be valid for all Member States.

3.The approval shall specify whether the authorisation to issue certificates as referred to in Article 17(1)(b) and (2)(c) shall be on a worldwide basis or limited to a certain number of third countries.

Article 19U.K.

1.The SA shall act in accordance with the rules set out in Annex VIII, Chapter II, point 1.

If one or more of the conditions set out in those rules are not respected, the Member State which has approved the SA shall suspend the approval for such a period as is required to remedy the situation.

2.The Member State which has approved the SA shall control the performance and behaviour of the SA in accordance with the requirements set out in Annex VIII, Chapter II, point 2.

Article 20U.K.

Member States which have approved SAs shall provide for an effective system of sanctions for cases where an approved SA has issued a false certificate.

Article 21U.K.

1.The Member State which has approved the SA shall immediately withdraw the approval:

if the SA does no longer comply with the conditions for approval set out in Annex VIII, Chapter I, or

if the SA has repeatedly and systematically issued false certificates. In this case the sanction provided for in Article 20 shall not apply.

2.The withdrawal shall be total or limited to certain parts or activities of the SA according to the nature of the shortcomings detected.

3.Whenever an approval is withdrawn by a Member State from an SA belonging to a group of companies, Member States which have approved SAs belonging to the same group, shall suspend the approvals of these SAs for a period not exceeding three months in order to carry out the necessary investigations to verify whether the SAs also feature the shortcomings detected in relation to the SA whose approval has been withdrawn.

For the application of the first subparagraph, a group of companies shall comprise all companies whose capital is owned, directly or indirectly, for more than 50 % by one single parent company, as well as the parent company itself.

Article 22U.K.

1.Member States shall notify the approval of SAs to the Commission.

2.A Member State that withdraws or suspends the approval shall immediately notify the other Member States and the Commission, indicating the shortcomings that led to the withdrawal or suspension.

The notification to Member States shall be sent to the Member States central bodies listed in Annex XIII.

3.The Commission shall periodically publish for information an updated list of the SAs approved by Member States.

Article 23U.K.

1.Certificates as referred to in Article 17(1)(b) and (2)(c) issued after the date of withdrawal or suspension of the approval shall not be valid.

2.Member States shall refuse to accept certificates as referred to in Article 17(1)(b) and (2)(c) if they detect irregularities or deficiencies in the certificates. When such certificates have been issued by an SA approved by another Member State, the Member State which detects the irregularities shall notify these circumstances to the Member State which gave the approval.

Article 24U.K.

1.Member States may exempt exporters from furnishing the proof required pursuant to Article 17 other than the transport document or its electronic equivalent as referred to in Article 17(3), in case of an export declaration giving entitlement to a refund where:

(a)the differentiated part of the refund is no more than:

(i)

EUR 2 400 where the third country or territory of destination is listed in Annex XIV;

(ii)

EUR 12 000 where the third country or territory of destination is not listed in Annex XIV; or

(b)the port of destination is located in the remote refund zone for the product concerned.

2.The exemption referred to in paragraph 1(b) shall apply only where the following conditions are met:

(a)the products are transported in containers and transport of the containers to the port of unloading is done by sea;

(b)the transport document mentions as destination the country mentioned in the export declaration or a port normally used for unloading products destined for a hinterland country which is the country of destination mentioned in the export declaration;

(c)the proof of unloading is provided pursuant to point (a), (b) or (c) of Article 17(2).

At the request of the exporter, in the case of container transport by sea, a Member State may accept that the proof of unloading referred to in point (c) of the first subparagraph is provided instead by information equivalent to that of the unloading document if it is generated by an information system managed by a third party responsible for the transport of the containers to and unloading of the containers at the place of destination, provided that the third party specialises in such operations and the information system security is approved by the Member State as meeting the criteria laid down in the version applicable to the period concerned of one of the internationally accepted standards set out in point 3(B) of Annex I to Regulation (EC) No 885/2006.

The proof of unloading may be provided pursuant to point (c) of the first subparagraph or pursuant to the second subparagraph without the exporter having to prove that he has taken the appropriate steps to obtain the document referred to in points (a) or (b) of Article 17(1).

3.Eligibility for the exemptions referred to in paragraph 1(a) shall be automatic except in case of application of paragraph 4.

Eligibility for the exemption referred to in paragraph 1(b) shall be granted for three years, by means of a written authorisation, in advance of export, upon application by the exporter. Exporters using these authorisations shall refer to the number of the authorisation in the payment application.

4.If the Member State considers that products for which the exporter claims an exemption under this Article have been exported to a country other than that mentioned in the export declaration or, as the case may be, to a country outside the relevant remote refund zone for which the refund is fixed, or the exporter has artificially divided an export operation with the aim of benefiting from an exemption, the Member State shall immediately withdraw eligibility for any exemption under this Article from the exporter concerned.

The exporter concerned shall not be eligible for any further exemption under this Article for two years from the date of withdrawal.

In case of withdrawal of eligibility the entitlement to the export refund for the products concerned shall no longer exist and the refund shall be reimbursed, unless the exporter can provide the proof required under Article 17 for the products concerned.

In addition, the entitlement to export refunds shall no longer exist for products covered by any export declaration made after the date of the act which led to the withdrawal of eligibility and the refunds shall be reimbursed, unless the exporter can provide the proof required under Article 17 for the products concerned.

Article 25U.K.

1.By way of derogation from Article 15 and without prejudice to Article 27, part of the refund shall be paid on application by the exporter once proof is furnished that the product has left the customs territory of the Community.

2.The part of the refund referred to in paragraph 1 shall be calculated using the lowest rate for the refund, less 20 % of the difference between the rate fixed in advance and the lowest rate, the non-fixing of a rate being regarded as the lowest rate.

Where the amount to be paid does not exceed EUR 2 000, Member States may defer payment of that amount until the full refund concerned is paid, except in cases where the exporter declares that he will not apply for payment of any further amount in respect of the exports concerned.

3.Where the destination marked in box 7 of licences issued with advance fixing of the refund is not observed:

(a)if the rate of refund corresponding to the actual destination is equal to or higher than the rate for the destination marked in box 7, the refund for the destination marked in box 7 shall apply;

(b)if the rate of refund corresponding to the actual destination is lower than the rate for the destination marked in box 7, the refund to be paid shall be:

(b)that obtained by the application of the rate corresponding to the actual destination,

less, except in cases of force majeure, 20 % of the difference between the refund for the destination marked in box 7 and the refund for the actual destination.

For the purposes of this Article, the rates of refund to be taken into consideration shall be those applying on the day the licence application is submitted. Such rates shall be adjusted, where applicable, on the date of acceptance of the export declaration or the payment declaration.

Where the first and second subparagraphs of this paragraph and Article 48 apply to the same export operation, the amount obtained by the application of the first subparagraph shall be reduced by the penalty provided for in Article 48.

4.Where a rate of refund is determined by invitation to tender and the relevant contract stipulates a compulsory destination, any periodic refund fixed or the fact that no such refund is fixed for that destination on the date of submission of the licence application or the date of acceptance of the export declaration shall not be taken into account for the purposes of determining the lowest rate of refund.

Article 26U.K.

1.Paragraphs 2 to 5 shall apply where a product is exported under an export licence or advance-fixing certificate stipulating a compulsory destination.