Schedules

Schedules 1—4. . . . F1

Schedule 5. . . . F2

Sch. 5 repealed by Betting and Gaming Duties Act 1972 (c. 25), s. 29(2), Sch. 7

Schedule 6. . . . F3

Sch. 6 repealed by Finance Act 1972 (c. 41), ss. 54(8), 134(7), Sch. 28 Pt. II

Schedule 7. . . . F4

Sch. 7 repealed by Vehicles (Excise) Act 1971 (c. 10), s. 39(5), Sch. 8 Pt. I

Schedules 8—10. . . . F5

Schs. 8–10 repealed by Income and Corporation Taxes Act 1970 (c. 10), ss. 583(1), 539(1), Sch. 16

Schedules 11, 12. . . . F6

Schs. 11, 12 repealed (with savings) by Capital Gains Tax Act 1979 (c. 14), ss. 157(1), 158, Sch. 6 para. s. 10(2)(b), Sch. 8

Schedule 13. . . . F7

Sch. 13 repealed by Income and Corporation Taxes Act 1970 (c. 10), ss. 538(1), 539(1), Sch. 16

Schedule 14. . . . F8

Sch. 14 repealed (with savings) by Finance Act 1975 (c. 7), ss. 50, 52(2)(3), 59, Sch. 13 Pt. I

F20Schedule 15. Special Charge: Trusts

Sch. 15 repealed (21.7.2008) by Statute Law (Repeals) Act 2008 (c. 12), Sch. 1 Pt. 8

F20 Income out of capital, et ceteralaetc.

F201

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20 Recovery of charge from trustees

F202

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F203

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F204

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F205

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20 Income derived from another trust

F206

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20 Notice to persons answerable for a trust

F207

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20 Application of trust property in payment of charge

F208

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20 Foreign trusts

F209

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20 Limitation of liability of trustees

F2010

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20 Interpretation

F20ll

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2012

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2013

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F21Schedule 16. Special Charge: Close Companies

Sch. 16 repealed (21.7.2008) by Statute Law (Repeals) Act 2008 (c. 12), Sch. 1 Pt. 8

F21 Special Apportionments

F211

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F212

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F213

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F21 Recovery of special charge from company

F214

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Schedule 17. . . . F9

Sch. 17 repealed by Finance Act 1972 (c. 41), ss. 122(5), 134(7), Sch. 28 Pt. IX

SCHEDULE 18 Premium Savings Bonds: New Terms

1

Premium Savings Bonds are a Government Security and are eligible for inclusion in draws for cash prizes. These prizes are free from United Kingdom Income Tax, Surtax and Capital Gains Tax.

2

Premium Saving Bonds, (Series B) (hereinafter called Bonds) will be issued in units of £1 by the Treasury and will be subject to regulations made from time to time by the Treasury under section 12 of the M1National Debt Act 1958, or having effect by virtue of that Act. The principal of the Bonds and the prizes allotted will be a charge on the National Loans Fund with recourse to the Consolidated Fund.

F143

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4

Bonds are not transferable either during the lifetime or on the death of the registered holder. No responsibility can be accepted in respect of their use as security for a loan.

5

There will be a monthly prize fund which will be determined by calculating one month’s interest on each bond eligible for the draws in that month. The rate of interest will be 45/8% per annum or such other rate as may be prescribed under the provisions of paragraph 15 below.

F156

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7

F22... After a Bond has qualified for its first draw it will be included in each succeeding draw, unless it has been repaid before the first day of the month in which the draw is held or (subject to the provisions of paragraph 15 below) the registered holder has died before the first day of a period of twelve consecutive calendar months preceding the month in which the draw is held.

8

Each £1 unit Bond will have one chance in each draw for which it is eligible. Each £1 unit Bond may win not more than one prize in each draw for which it is eligible and in draws producing more that one prize will be allotted the highest prize for which it is drawn.

9

Notwithstanding the provisions of paragraph 7 above any Bond purchased in contravention of any regulation limiting the number of unit Bonds which may held by any person shall not be eligible for inclusion in any draw until the holding has been reduced to not more than the maximum number permitted by such regulation.

F1610

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11

12

All matters relating to the method and conduct of the draw and allotment of prizes shall be at the sole discretion of the Postmaster General, whose decision as to which Bonds have drawn prizes shall be final.

13

The purchase price of a Bond is repayable in full on application to the Bonds and Stock Office.

F1814

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

15

The Treasury reserve the right F11...:—

a

to vary the rate of interest specified in paragraph 5 above for determining the amount of the prize fund;

F12b

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

c

to vary the provisions of paragraph 7 above insofar as they relate to the eligibility of a Bond for inclusion in a draw after the death of the registered holder;

d

to declare any Bonds purchased on or before a date specified F13... to be ineligible for further draws.

F1916

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Schedule 19 . . . F10

Sch. 19 repealed by Finance Act 1971 (c. 68), s. 69(7), Sch. 14 Pt. VII

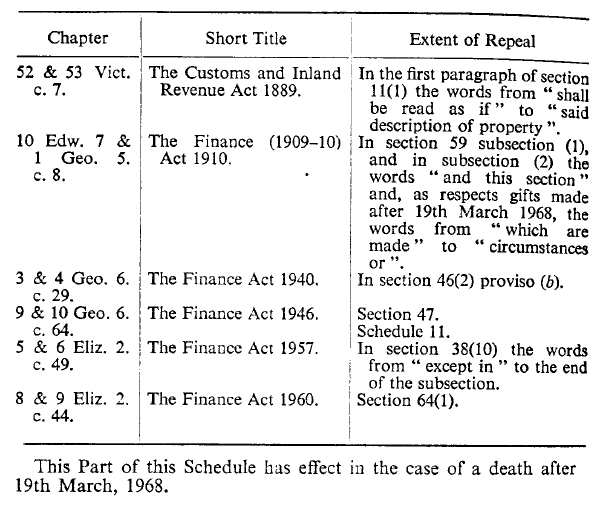

C1schedule 20 REPEALS

The text of Schedule 20 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and, does not reflect any amendments or repeals which may have been prior to 1.2.1991.

Schs. 1–4 repealed by Finance Act 1969 (c. 32), s. 61(6), Sch. 21 Pt. I