SCHEDULES

SCHEDULE 1F15Table of rates of duty on wine and made-wine

Part 1Wine or made-wine of a strength not exceeding 22 per cent

Description of wine or made-wine | Rates of duty per hectolitre |

|---|---|

£ | |

Wine or made-wine of a strength not exceeding 4 per cent | 65.94 |

Wine or made-wine of a strength exceeding 4 per cent but not exceeding 5.5 per cent | 90.68 |

Wine or made-wine of a strength exceeding 5.5 per cent but not exceeding 15 per cent and not being sparkling | 214.02 |

Sparkling wine or sparkling made-wine of a strength exceeding 5.5 per cent but less than 8.5 per cent | 207.20 |

Sparkling wine or sparkling made-wine of a strength of 8.5 per cent or of a strength exceeding 8.5 per cent but not exceeding 15 per cent | 274.13 |

Wine or made-wine of a strength exceeding 15 per cent but not exceeding 22 per cent | 285.33 |

Part 2Wine or made-wine of a strength exceeding 22 per cent

Description of wine or made-wine | Rates of duty per litre of alcohol in wine or made-wine |

|---|---|

£ | |

Wine or made-wine of a strength exceeding 22 per cent | 22.64. |

Interpretation

F11

Paragraphs 2 and 3 below apply for the purposes of this Act.

2

1

Wine or made-wine which is for the time being in a closed container is sparkling if, due to the presence of carbon dioxide or any other gas, the pressure in the container, measured at a temperature of 20°C, is not less than 3 bars in excess of atmospheric pressure.

2

Wine or made-wine which is for the time being in a closed container is sparkling regardless of the pressure in the container if the container has a mushroom-shaped stopper (whether solid or hollow) held in place by a tie or fastening.

3

Wine or made-wine which is not for the time being in a closed container is sparkling if it has characteristics similar to those of wine or made-wine which has been removed from a closed container and which, before removal, fell within sub-paragraph (1) above.

3

1

Wine or made-wine shall be regarded as having been rendered sparkling if, as a result of aeration, fermentation or any other process, it either falls within paragraph 2(1) above or takes on such characteristics as are referred to in paragraph 2(3) above.

2

Wine or made-wine which has not previously been rendered sparkling by virtue of sub-paragraph (1) above shall be regarded as having been rendered sparkling if it is transferred into a closed container which has a mushroom-shaped stopper (whether solid or hollow) held in place by a tie or fastening.

3

Wine or made-wine which is in a closed container and has not previously been rendered sparkling by virtue of sub-paragraph (1) or (2) above shall be regarded as having been rendered sparkling if the stopper of its container is exchanged for a stopper of a kind mentioned in sub-paragraph (2) above.

SCHEDULE 2 . . . F2

Sch. 2 repealed by Finance Act 1984 (c. 43, SIF 40:1), s. 128(6), Sch. 23 Pt. I

F14SCHEDULE 2ADuty stamps

Sch. 2A inserted (with effect in accordance with s. 4(5) of the amending Act) by Finance Act 2004 (c. 12), Sch. 1; S.I. 2006/201, art. 2

Retail containers to be stamped

1

1

Retail containers of alcoholic liquors to which this Schedule applies shall be stamped—

a

in such cases and circumstances, and with a duty stamp of such a type, as may be prescribed; but

b

subject to such exceptions as may be prescribed.

2

In this Schedule “retail container”, in relation to an alcoholic liquor, means a container—

a

of a capacity of 35 centilitres or more, and

b

in which, or from which, the liquor is intended to be sold by retail.

3

This Schedule applies to the following alcoholic liquors—

a

spirits F12of a strength of 30 per cent or more;

b

wine or made-wine of a strength F13of 30 per cent or more.

4

For the purposes of this Schedule a retail container is “stamped” if—

a

it carries a duty stamp of a type mentioned in sub-paragraph (5)(a) below which has been affixed to the container in a way that complies with the requirements of regulations under this Schedule, or

b

it carries a label which has been so affixed to the container and the label incorporates a duty stamp of a type mentioned in sub-paragraph (5)(b) below.

5

In this Schedule “duty stamp” means any of the following—

a

a document (a “type A stamp”) issued by or on behalf of the Commissioners which—

i

is designed to be affixed to a retail container of alcoholic liquor, and

ii

indicates that the appropriate duty, or an amount representing some or all of the appropriate duty, has been (or is to be) paid;

b

a part of a label for a retail container of alcoholic liquor (a “type B stamp”) which—

i

is incorporated in the label under the authority of the Commissioners, and

ii

indicates that the appropriate duty, or an amount representing some or all of the appropriate duty, has been (or is to be) paid.

6

In sub-paragraph (5) above “the appropriate duty” means the duty chargeable on the quantity and description of alcoholic liquor contained, or to be contained, in the retail container to which the stamp, or the label incorporating the stamp, is, or is to be, affixed.

Power to alter liquors, and capacity of container, to which this Schedule applies

2

1

The Treasury may by order made by statutory instrument amend paragraph (a) of paragraph 1(2) above for the purpose of varying the capacity from time to time specified in that paragraph.

2

The Treasury may by order made by statutory instrument amend paragraph 1(3) above for the purpose of causing this Schedule—

a

to apply to any description of alcoholic liquor to which it does not apply, or

b

to cease to apply to any description of alcoholic liquor to which it does apply.

3

A statutory instrument containing an order under this paragraph shall not be made unless a draft of the instrument has been laid before, and approved by a resolution of, the House of Commons.

Acquisition of and payment for duty stamps

3

1

The Commissioners may by regulations make provision as to the terms and conditions on which a person may obtain—

a

a type A stamp,

b

authority to incorporate in a label a type B stamp,

c

authority to obtain a label incorporating a type B stamp,

d

authority to affix such a label to a retail container of alcoholic liquor.

2

Regulations under sub-paragraph (1) above may in particular make provision for or in connection with—

a

requiring a person in prescribed cases or circumstances to pay, or agree to pay, the prescribed amount to the Commissioners or to a person authorised by the Commissioners for this purpose;

b

requiring a person in prescribed cases or circumstances to provide to the Commissioners such security as they may require in respect of payment of the appropriate duty.

3

An amount prescribed for the purposes of sub-paragraph (2)(a) above must not exceed the aggregate of—

a

an amount representing the appropriate duty, and

b

in the case of a type A stamp, the cost of issuing the stamp.

4

Regulations under sub-paragraph (1) above may also in particular make provision for or in connection with requiring or enabling the Commissioners to bear, in prescribed circumstances, in the case of a type B stamp, all or part of so much of the cost of producing the label as is attributable to the incorporation in it of the stamp.

5

The whole of an amount payable for a duty stamp shall be treated for the purposes of the Customs and Excise Acts 1979 as an amount due by way of excise duty.

6

In this paragraph “the appropriate duty” means the duty chargeable on the quantity and description of alcoholic liquor contained, or to be contained, in the retail container to which the stamp, or the label incorporating the stamp, is to be affixed.

Regulations

4

1

The Commissioners may by regulations make provision as to such matters relating to duty stamps as appear to them to be necessary or expedient.

2

Regulations under this Schedule may in particular make provision about—

a

the times at which a retail container must bear a duty stamp;

b

the type of duty stamp (see paragraph 1(5)) with which a retail container is to be stamped in any particular case or circumstances;

c

the design and appearance of a duty stamp (including the production of a label incorporating a type B stamp);

d

the information that is to appear on a duty stamp;

e

the cost of issuing a type A stamp for the purposes of paragraph 3(3)(b) above;

f

the procedure for obtaining—

i

a type A stamp,

ii

authority to incorporate in a label a type B stamp,

iii

authority to obtain a label incorporating a type B stamp,

iv

authority to affix such a label to a retail container of alcoholic liquor,

(including provision setting periods of notice);

g

where on the container a type A stamp, or a label incorporating a type B stamp, is to be affixed;

h

repayment of, or credit for, in prescribed circumstances and subject to such conditions as may be prescribed, all or part of a payment made under or by virtue of this Schedule to the Commissioners or to a person authorised by the Commissioners;

i

liability to forfeiture in prescribed circumstances of some or all of a payment made, or security provided, under or by virtue of this Schedule to the Commissioners or to a person authorised by the Commissioners.

3

Regulations under this Schedule may also, in particular, make provision for or in connection with preventing a type A stamp, or a label incorporating a type B stamp, from being used by a person other than—

a

in the case of a type A stamp, the person to or for whom the stamp was issued or a person authorised by that person to affix the stamp to a retail container of alcoholic liquor,

b

in the case of a type B stamp, the person to or for whom authority to obtain the label incorporating the stamp, or to affix that label to a retail container of alcoholic liquor, was given by the Commissioners.

4

Regulations under this Schedule may also, in particular, make provision—

a

for or in connection with requiring a person who is not established, and does not have any fixed establishment, in the United Kingdom, in prescribed circumstances, to appoint another person (a “duty stamps representative”) to act on his behalf in relation to duty stamps, and

b

as to the rights, obligations or liabilities of duty stamps representatives.

5

The Commissioners may, with a view to the protection of the revenue, make regulations for securing and collecting duty payable in accordance with this Schedule.

6

Regulations under this Schedule may make different provision for different cases.

Offences of possession, sale etc of unstamped containers

5

1

Except in such cases as may be prescribed, a person commits an offence if he—

a

is in possession of, transports or displays, or

b

sells, offers for sale or otherwise deals in,

unstamped retail containers containing alcoholic liquor to which this Schedule applies.

2

It is a defence for a person charged with an offence under this paragraph to prove that the retail containers in question were not required to be stamped.

3

A person who commits an offence under this paragraph is liable on summary conviction to a fine not exceeding level 5 on the standard scale.

4

A retail container in relation to which an offence under this paragraph is committed is liable to forfeiture (together with its contents).

Offence of using premises for sale of liquor in or from unstamped containers

6

1

A manager of premises commits an offence if—

a

he suffers the premises to be used for the sale of liquor in an unstamped retail container, or for the sale of liquor that is from an unstamped retail container; and

b

the liquor is alcoholic liquor to which this Schedule applies.

2

It is a defence for a person charged with an offence under this paragraph to prove that the retail container in question was not required to be stamped.

3

A person who commits an offence under this paragraph is liable on summary conviction to a fine not exceeding level 5 on the standard scale.

4

Where an offence is committed under this paragraph, all unstamped retail containers of alcoholic liquor to which this Schedule applies that are on the premises at the time of the offence are liable to forfeiture (together with their contents).

5

For the purposes of this Schedule a person is a “manager” of premises if he—

a

is entitled to control their use,

b

is entrusted with their management, or

c

is in charge of them.

Alcohol sales ban following conviction for offence under paragraph 6

7

1

A court by or before which a person is convicted of an offence under paragraph 6 above may make an order prohibiting the use of the premises in question for the sale of alcoholic liquors during a period specified in the order.

2

The period specified in an order under this paragraph shall not exceed six months; and the first day of the period shall be the day specified as such in the order.

3

If a manager of premises suffers the premises to be used in breach of an order under this paragraph, he commits an offence and is liable on summary conviction to a fine not exceeding level 5 on the standard scale.

Penalty for altering duty stamps

8

1

This paragraph applies where a person—

a

alters a type A stamp, otherwise than in accordance with regulations under this Schedule, after it has been issued, or

b

so alters a type B stamp after the label in which it is incorporated has been produced.

2

His conduct attracts a penalty under section 9 of the Finance Act 1994 (civil penalties).

3

The stamp, or the label in which it is incorporated, is liable to forfeiture.

Penalty for affixing wrong, altered or forged stamps, or over-labelling

9

1

This paragraph applies where a person affixes to a retail container that is required to be stamped any of the items mentioned in sub-paragraphs (2) to (5) below.

2

The first is—

a

a type A stamp, or

b

a label incorporating a type B stamp,

if the stamp is not a correct stamp for that container in accordance with regulations under this Schedule.

3

The second is—

a

a type A stamp that has been altered, otherwise than in accordance with regulations under this Schedule, after it has been issued, or

b

a label incorporating a type B stamp if the stamp has been so altered after the label has been produced.

4

The third is an item that purports to be, but is not,—

a

a type A stamp, or

b

a label incorporating a type B stamp.

5

The fourth is any label or other item affixed in such a way as to cover up all or part of—

a

a type A stamp affixed to the container, or

b

a type B stamp incorporated in a label affixed to the container,

except where the label or other item is so affixed in accordance with regulations under this Schedule.

6

The person’s conduct attracts a penalty under section 9 of the Finance Act 1994 (civil penalties).

7

The container is liable to forfeiture (together with its contents).

Penalty for failing to comply with regulations

10

1

If a person fails to comply with a requirement imposed by or under regulations under this Schedule—

a

his conduct attracts a penalty under section 9 of the Finance Act 1994 (civil penalties);

b

any article in respect of which he fails to comply with the requirement is liable to forfeiture (including, in the case of a container, its contents).

2

Regulations under this Schedule may make provision as to the amount by reference to which the penalty under sub-paragraph (1)(a) above is to be calculated.

Forfeiture of forged, altered or stolen duty stamps

11

1

The following items are liable to forfeiture.

2

The first is an item that purports to be, but is not,—

a

a type A stamp, or

b

a label incorporating a type B stamp.

3

The second is—

a

a type A stamp that has been altered, otherwise than in accordance with regulations under this Schedule, after it has been issued, or

b

a label incorporating a type B stamp if the stamp has been so altered after the label has been produced.

4

The third is—

a

a type A stamp, or

b

a label incorporating a type B stamp,

that is in a person’s possession unlawfully.

Interpretation

12

In this Schedule—

“duty stamp” has the meaning given by paragraph 1(5) above;

“prescribed” means prescribed in regulations made by the Commissioners;

“retail container” has the meaning given by paragraph 1(2) above;

“stamped” and “unstamped” are to be read in accordance with paragraph 1(4) above;

“type A stamp” has the meaning given by paragraph 1(5)(a) above;

“type B stamp” has the meaning given by paragraph 1(5)(b) above.

SCHEDULE 3 CONSEQUENTIAL AMENDMENTS

1

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F3

3

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F4

M1Licensing Act 1964

F115

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F5

M2Licensing Act (Northern Ireland) 1971

8

1

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F6

2

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F7

4

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F8

5

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F9

M3Licensing (Scotland) Act 1976

C19

In section 139(1) of the Licensing (Scotland) Act 1976 the following amendments shall be made, that is to say—

a

in the definitions of “made-wine” and “wine”, for the words “Customs and Excise Act 1952” there shall be substituted the words “

section 1 of the Alcoholic Liquor Duties Act 1979

”

;

b

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F10

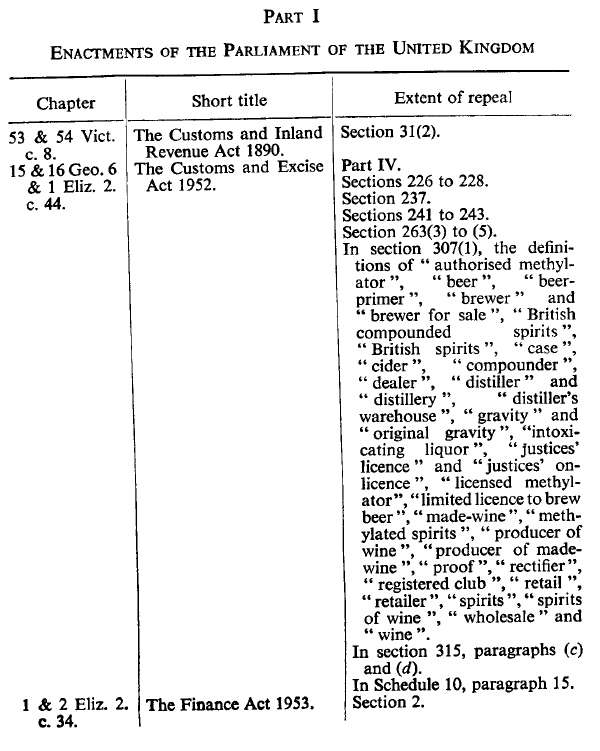

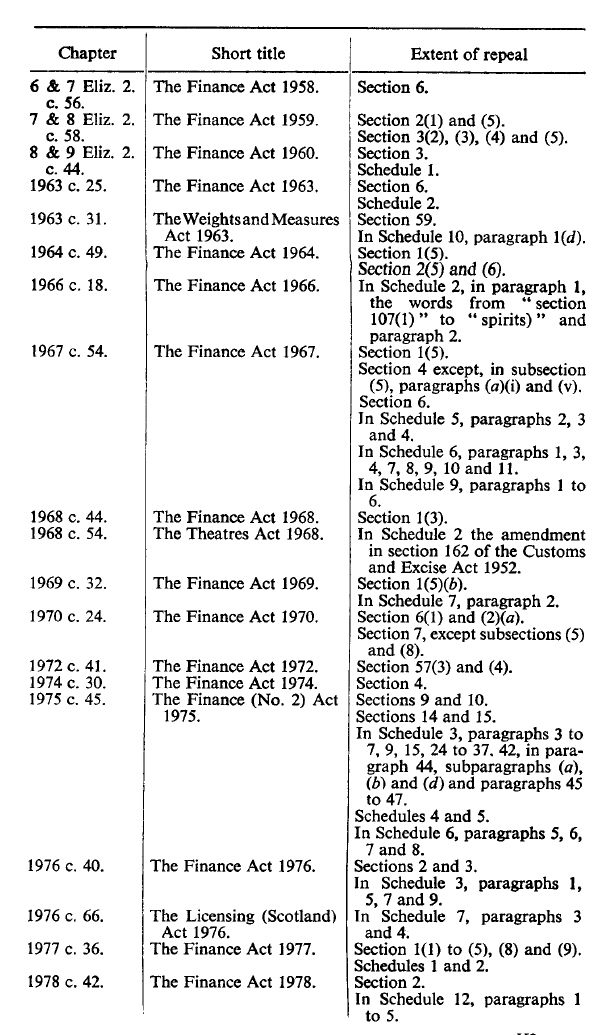

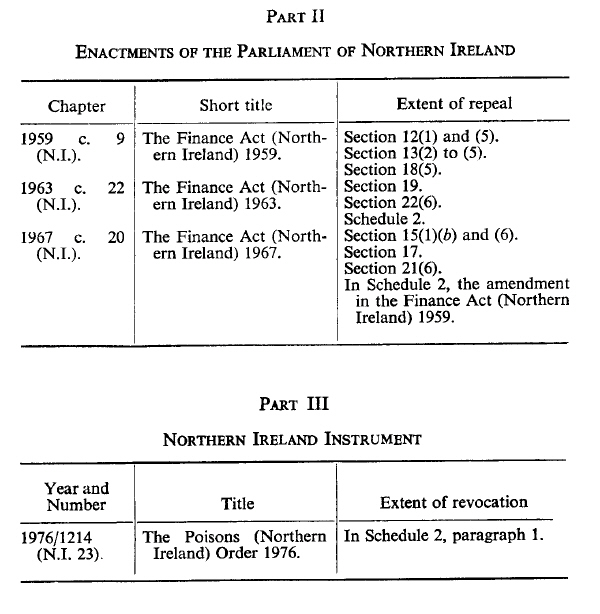

C2SCHEDULE 4 REPEALS

The text of Sch. 4 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991.

Sch. 1 Table substituted (23.4.2009) by Finance Act 2009 (c. 10), s. 11(5)(7)