- Latest available (Revised)

- Point in Time (01/04/2022)

- Original (As enacted)

Hydrocarbon Oil Duties Act 1979

You are here:

- UK Public General Acts

- 1979 c. 5

- Schedules only

What Version

Advanced Features

- Show Geographical Extent(e.g. England, Wales, Scotland and Northern Ireland)

- Show Timeline of Changes

Opening Options

More Resources

Changes over time for: Hydrocarbon Oil Duties Act 1979 (Schedules only)

Version Superseded: 15/03/2023

Alternative versions:

- 01/02/1991- Amendment

- 21/05/1991- Amendment

- 01/10/1991- Amendment

- 01/09/1994- Amendment

- 01/07/1995- Amendment

- 01/12/1995- Amendment

- 01/01/1996- Amendment

- 01/11/1996- Amendment

- 15/11/1996- Amendment

- 15/08/1997- Amendment

- 17/03/1998- Amendment

- 28/07/2000- Amendment

- 01/10/2000- Amendment

- 07/03/2001- Amendment

- 08/03/2001- Amendment

- 24/07/2002- Amendment

- 22/07/2004- Amendment

- 01/09/2004- Amendment

- 01/04/2007- Amendment

- 01/04/2008- Amendment

- 01/11/2008- Amendment

- 01/11/2013- Amendment

- 29/06/2021- Amendment

- 01/10/2021- Amendment

- 01/04/2022- Amendment

- 01/04/2022

Point in time - 15/03/2023- Amendment

- 22/02/2024- Amendment

Status:

Point in time view as at 01/04/2022.

Changes to legislation:

Hydrocarbon Oil Duties Act 1979 is up to date with all changes known to be in force on or before 11 November 2024. There are changes that may be brought into force at a future date. Changes that have been made appear in the content and are referenced with annotations.

Changes to Legislation

Changes and effects yet to be applied by the editorial team are only applicable when viewing the latest version or prospective version of legislation. They are therefore not accessible when viewing legislation as at a specific point in time. To view the ‘Changes to Legislation’ information for this provision return to the latest version view using the options provided in the ‘What Version’ box above.

SCHEDULES

F1SCHEDULE 1U.K. EXCEPTED VEHICLES

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F1Sch. 1 omitted (1.4.2022) by virtue of Finance Act 2021 (c. 26), s. 102(2), Sch. 21 para. 21

Section 27(1)

[F2SCHEDULE 1AU.K.Excepted machines

Textual Amendments

F2Sch. 1A inserted (1.4.2022) by Finance Act 2021 (c. 26), s. 102(2), Sch. 21 para. 22

1U.K.Any vehicle, vessel, machine or appliance of one of the following descriptions is an “excepted machine” for the purposes of this Act.

Agricultural vehicleU.K.

2(1)An agricultural vehicle at a time when it is used for—U.K.

(a)purposes relating to agriculture, horticulture, pisciculture or forestry,

(b)cutting verges bordering public roads,

(c)cutting hedges or trees bordering public roads or bordering verges which border public roads, or

(d)clearing or otherwise dealing with frost, ice, snow or flooding,

including when it is going to or from the place where it is to be or has been used for any of those purposes.

[F3(2)An agricultural vehicle that is primarily kept for use within sub-paragraph (1) at a time when it is used for any other purpose on private land where it is ordinarily kept.]

(3)An agricultural vehicle kept and used on a golf course or on land maintained by a community amateur sports club.

(4)An agricultural vehicle used in any other circumstances provided—

(a)it is not being used on a public road, and

(b)it uses fuel gas for fuel.

(5)In this paragraph, “an agricultural vehicle” means—

(a)a tractor;

(b)a vehicle designed and constructed primarily for use otherwise than on roads which—

(i)has a revenue weight not exceeding 1,000 kilograms, and

(ii)is designed and constructed to seat only the driver;

(c)any vehicle that is an exempt vehicle for the purposes of paragraph 20A of Schedule 2 to [F4the Vehicle Excise and Registration Act 1994 (vehicles used between different parts of land)];

[F5(d)any other vehicle that is used for the conveyance of machinery that is built into or permanently attached to the vehicle, provided that the machinery is used in the processing or handling of agricultural, horticultural, piscicultural or forestry produce or materials.]

Textual Amendments

F3Sch. 1A para. 2(2) substituted (1.4.2022) by Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(a)(i)

F4Words in Sch. 1A para. 2(5)(c) substituted (1.4.2022) by Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(a)(ii)

F5Sch. 1A para. 2(5)(d) substituted (1.4.2022) by Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(a)(iii)

Special vehiclesU.K.

3(1)A special vehicle at a time when it is used—U.K.

(a)for purposes relating to agriculture, horticulture, pisciculture or forestry, including when it is going to or from the place where it is to be or has been used for such purposes, F6...

(b)on a golf course or on land maintained by a community amateur sports club [F7, or

(c)to go to, or from, a golf course or land maintained by a community amateur sports club to be used, or after being used, on the golf course or land.]

(2)A special vehicle used in any other circumstances provided it uses fuel gas for fuel.

(3)In this paragraph, a “special vehicle” is a vehicle of any weight but otherwise designed, constructed and used as mentioned in Part 4 of Schedule 1 to the Vehicle Excise and Registration Act 1994.

Textual Amendments

F6Word in Sch. 1A para. 3(1)(a) omitted (1.4.2022) by virtue of Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(b)(i)

F7Sch. 1A para. 3(1)(c) and word inserted (1.4.2022) by Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(b)(ii)

Unlicensed vehiclesU.K.

4(1)An unlicensed vehicle at a time when it is used—U.K.

(a)for purposes relating to agriculture, horticulture, pisciculture or forestry,

(b)on a golf course or on land maintained by a community amateur sports club, or

(c)on land occupied by a travelling fair or travelling circus.

(2)An unlicensed vehicle used in any other circumstances provided it uses fuel gas for fuel.

(3)In this paragraph, “unlicensed vehicle” means a vehicle that is—

(a)unlicensed for the purposes of section 22(1D) of the Vehicle Excise and Registration Act 1994,

(b)kept by a person who has complied with such requirements relating to the vehicle as are prescribed for the time being in regulations under that section, and

(c)not used or kept on a public road.

Trains etcU.K.

5U.K.Any vehicle designed to be operated on a railway within the meaning of section 67(1) of the Transport and Works Act 1992.

VesselsU.K.

6(1)Any vessel other than a vessel F8... that is a private pleasure craft.U.K.

(2)Any machine or appliance that is permanently on a vessel within sub-paragraph (1).

(3)Any machine or appliance that is permanently on a private pleasure craft F9..., but that draws fuel from a supply other than the supply from which the engine provided for propelling the private pleasure craft draws fuel.

F10(4). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F8Words in Sch. 1A para. 6(1) omitted (1.4.2022) by virtue of Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(c)(i)

F9Words in Sch. 1A para. 6(3) omitted (1.4.2022) by virtue of Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(c)(ii)

F10Sch. 1A para. 6(4) omitted (1.4.2022) by virtue of Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(c)(iii)

Mowing machinesU.K.

7U.K.A machine designed only for mowing grass at a time when it is used on—

(a)land maintained for purposes relating to agriculture, horticulture, pisciculture or forestry;

(b)a golf course or on land maintained by a community amateur sports club;

(c)land occupied by a travelling fair or travelling circus.

Other machines or appliancesU.K.

8(1)A machine or appliance that is not a vehicle or vessel at a time when it is used—U.K.

(a)for purposes relating to agriculture, horticulture, pisciculture or forestry;

[F11(aa)for any purpose on land where it is kept and used for purposes relating to agriculture, horticulture, pisciculture or forestry;]

(b)on a golf course or on land maintained by a community amateur sports club;

(c)to operate or maintain equipment in a travelling fair or travelling circus;

(d)for heating, or to generate electricity, for premises that are not used for commercial purposes;

[F12(e)for heating of premises that are used for commercial purposes provided that it uses kerosene for fuel.]

(2)For the purposes of sub-paragraph (1)(d), caravans used for the accommodation of those who travel with a travelling fair or travelling circus are to be treated as premises that are not used for commercial purposes.

Textual Amendments

F11Sch. 1A para. 8(1)(aa) inserted (1.4.2022) by Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(d)(i)

F12Sch. 1A para. 8(1)(e) inserted (1.4.2022) by Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(d)(ii)

InterpretationU.K.

9(1)In this Schedule—U.K.

“caravan” has the meaning given by section 29(1) of the Caravan Sites and Control of Development Act 1960;

“community amateur sports club” has the meaning given by section 658 of the Corporation Tax Act 2010;

“fair” means a fair consisting wholly or principally of the provision of amusements;

“fuel gas” means any substance which would be road fuel gas within the meaning given by section 5(1) if it were for use as fuel in a road vehicle;

“golf course” includes driving range (whether or not on the site of a golf course).

(2)In this Schedule, references to a vehicle being used—

(a)on a golf course, or

(b)on land maintained by a community amateur sports club,

include references, when two parts of the golf course or land are on either side of a road, to the vehicle going between the two parts by the shortest practicable route.

(3)In this Schedule, a fair or circus is a travelling fair or circus if—

(a)it is provided or operated wholly or principally by persons who travel from place to place for the purpose of providing or operating fairs or circuses, F13...

[F14(b)it is fully dismantled at least once a year, and]

[F15(c)the persons who provide or operate it are able to demonstrate that, when the fair or circus is dismantled, it is capable of being transported to another location.]]

Textual Amendments

F13Word in Sch. 1A para. 9(3)(a) omitted (1.4.2022) by virtue of Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(e)(i)

F14Sch. 1A para. 9(3)(b) substituted (1.4.2022) by Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(e)(ii)

F15Sch. 1A para. 9(3)(c) inserted (1.4.2022) by Finance Act 2022 (c. 3), s. 76(2), Sch. 11 para. 9(e)(iii)

Section 17(7).

SCHEDULE 2U.K. MEANING OF “HORTICULTURAL PRODUCE” FOR PURPOSES OF RELIEF UNDER SECTION 17

In section 17 of this Act “horticultural produce” means—

(a)fruit;

(b)vegetables of a kind grown for human consumption, including fungi, but not including maincrop potatoes or peas grown for seed, for harvesting dry or for vining;

(c)flowers, pot plants and decorative foliage;

(d)herbs;

(e)seeds other than pea seeds, and bulbs and other material, being seeds, bulbs or material for sowing or planting for the production of—

(i)fruit,

(ii)vegetables falling within paragraph (b) above,

(iii)flowers, plants or foliage falling within paragraph (c) above, or

(iv)herbs,

or for reproduction of the seeds, bulbs or other material planted; or

(f)trees and shrubs, other than trees grown for the purpose of afforestation;

but does not include hops.

F16 SCHEDULE 2AU.K. Mixing of rebated oil

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F16Sch. 2A repealed (with effect in accordance with s. 9(4) of the amending Act) by Finance Act 2004 (c. 12), s. 9(3), Sch. 42 Pt. 1(1)

Section 21(1).

SCHEDULE 3U.K. SUBJECTS FOR REGULATIONS UNDER SECTION 21

Part IU.K. hydrocarbon oil

1U.K.Prohibiting the production of hydrocarbon oil or any description of hydrocarbon oil except by a person holding a licence.

2U.K.[F17Specifying the circumstances in which any such licence may be surrendered or revoked]

Textual Amendments

F17Words substituted by Finance Act 1986 (c. 41, SIF 40:1), s. 8(6), Sch. 5 para. 4

3U.K.Regulating the production, storage and warehousing of hydrocarbon oil or any description of hydrocarbon oil and the removal of any such oil to or from premises used for the production of any such oil.

Modifications etc. (not altering text)

C1Sch. 3 para. 3 modified (1.9.2004) by The Biofuels and Other Fuel Substitutes (Payment of Excise Duties etc.) Regulations 2004 (S.I. 2004/2065), regs. 1(1), 3(1)(e)

C2Sch. 3 para. 3 modified by S.I. 2004/2065, reg. 3(2)(g) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(c))

4U.K.Prohibiting the refining of hydrocarbon oil elsewhere than in a refinery.

5U.K.Prohibiting the incorporation of gas in hydrocarbon oil elsewhere than in a refinery.

6U.K.Regulating the use and storage of hydrocarbon oil in a refinery.

Modifications etc. (not altering text)

C3Sch. 3 paras. 6-11 modified by S.I. 2004/2065, reg. 3(2)(g) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(c))

7U.K.Regulating or prohibiting the removal to a refinery of hydrocarbon oil in respect of which any rebate has been allowed.

Modifications etc. (not altering text)

C3Sch. 3 paras. 6-11 modified by S.I. 2004/2065, reg. 3(2)(g) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(c))

8U.K.Regulating the removal of imported hydrocarbon oil to a refinery without payment of the excise duty on such oil.

Modifications etc. (not altering text)

C3Sch. 3 paras. 6-11 modified by S.I. 2004/2065, reg. 3(2)(g) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(c))

9U.K.Making provision for securing payment of the excise duty on any imported hydrocarbon oil received into a refinery.

Modifications etc. (not altering text)

C3Sch. 3 paras. 6-11 modified by S.I. 2004/2065, reg. 3(2)(g) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(c))

10U.K.Relieving from the excise duty chargeable on hydrocarbon oil produced in the United Kingdom any such oil intended for exportation or shipment as stores.

Modifications etc. (not altering text)

C3Sch. 3 paras. 6-11 modified by S.I. 2004/2065, reg. 3(2)(g) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(c))

F1810A U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F18Sch. 3 para. 10A omitted (1.11.2008) by virtue of Finance Act 2008 (c. 9), Sch. 6 paras. 7, 21

Modifications etc. (not altering text)

C3Sch. 3 paras. 6-11 modified by S.I. 2004/2065, reg. 3(2)(g) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(c))

10B F19U.K.Conferring power to require information relating to the supply or use of aviation gasoline to be given by producers, dealers and users.

Textual Amendments

F19Sch. 3 Pt. I paras. 10A-C inserted by Finance Act 1992 (c. 39), s. 4(5)

Modifications etc. (not altering text)

C3Sch. 3 paras. 6-11 modified by S.I. 2004/2065, reg. 3(2)(g) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(c))

10C F20U.K.Requiring producers and users of and dealers in aviation gasoline to keep and produce records relating to aviation gasoline.

Textual Amendments

F20Sch. 3 Pt. I paras. 10A-C inserted by Finance Act 1992 (c. 39), s. 4(5)

Modifications etc. (not altering text)

C3Sch. 3 paras. 6-11 modified by S.I. 2004/2065, reg. 3(2)(g) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(c))

11U.K.Generally for securing and collecting the excise duty chargeable on hydrocarbon oil . . . F21.

Textual Amendments

F21Words repealed by Finance Act 1985 (c. 54, SIF 40:1), s. 7, Sch. 4 para. 4, Sch. 27 Pt. I Note 2

Modifications etc. (not altering text)

C3Sch. 3 paras. 6-11 modified by S.I. 2004/2065, reg. 3(2)(g) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(c))

C4Sch. 3 para. 11 modified (26.7.2002) by S.I. 2002/1928, reg. 3(1)(d)

C5Sch. 3 para. 11 modified (1.9.2004) by The Biofuels and Other Fuel Substitutes (Payment of Excise Duties etc.) Regulations 2004 (S.I. 2004/2065), regs. 1(1), 3(1)(e)

F22Part IIU.K.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F22Sch. 3 Pt. II repealed (1.12.1995) by 1993 c. 34, ss. 11(5), 213, Sch. 23 Pt.I; S.I. 1995/2715, art. 2

Part IIIU.K. road fuel gas

17U.K.Prohibiting the production of gas, and dealing in gas on which the excise duty has not been paid, except by persons holding a licence.

18U.K.[F24Specifying the circumstances in which any such licence may be surrendered or revoked].

Textual Amendments

F24Words substituted by Finance Act 1986 (c. 41, SIF 40:1), s. 8(6), Sch. 5 para. 4

19U.K.Regulating the production, dealing in, storage and warehousing of gas and the removal of gas to and from premises used therefor.

20U.K.Requiring containers for gas to be marked in the manner prescribed by the regulations.

21U.K.Conferring power to require information relating to the supply or use of gas and containers for gas to be given by producers of and dealers in gas, and by the person owning or possessing or for the time being in charge of any road vehicle which is constructed or adapted to use gas as fuel.

22U.K.Requiring a person owning or possessing a road vehicle which is constructed or adapted to use gas as fuel to keep such accounts and records in such manner as may be prescribed by the regulations, and to preserve such books and documents relating to the supply of gas to or by him, or the use of gas by him, for such period as may be so prescribed.

23U.K.Requiring the production of books or documents relating to the supply or use of gas or the use of any road vehicle.

24U.K.Authorising the entry and inspection of premises (other than private dwelling-houses) and the examination of road vehicles, and authorising, or requiring the giving of facilities for, the inspection of gas found on any premises entered or on or in any road vehicle.

25U.K.Generally for securing and collecting the excise duty.

In this Part of this Schedule “the excise duty” means the excise duty chargeable under section 8 of this Act on gas, and “gas” means road fuel gas.

Section 24(1).

SCHEDULE 4U.K. SUBJECTS FOR REGULATIONS UNDER SECTION 24

As to grant of relief . . . F25U.K.

Textual Amendments

F25Words repealed by Finance Act 1981 (c. 35, SIF 40:1), s. 139(6), Sch. 19 Pt. III Note 4 (by Note 4 it is provided that the repeal has effect in relation to oil used on or after 1.1.1982)

1U.K.Regulating the approval of persons for purposes of section 9(1) or (4) or 14(1) of this Act, whether individually or by reference to a class, and whether in relation to particular descriptions of oil or generally; enabling approval to be granted subject to conditions and providing for the conditions to be varied, or the approval revoked, for reasonable cause.

2U.K.Enabling permission under section 9(1) of this Act to be granted subject to conditions as to the giving of security and otherwise.

[F263U.K.Requiring claims or applications for repayment under section 9(4), 17, F27... F28... 19 or 19A of this Act to be made at such times and in respect of such periods as are prescribed; providing that no such claim or application shall lie where the amount to be paid is less than the prescribed minimum; and preventing, where a claim or application can be made under section 9(4) or 19, the payment of drawback.]

Textual Amendments

F26Sch. 4 Pt. II para. 3 substituted by Finance Act 1981 (c.35, SIF 40:1), s. 6(1)(3)

F27Word in Sch. 4 para. 3 omitted (retrospective to 1.4.2008) by virtue of Finance Act 2008 (c. 9), Sch. 5 paras. 23(a), 26(b)

F28Words in Sch. 4 para. 3 repealed (1.11.1996) by 1996 c. 8, ss. 8(2), 205, Sch. 41 Pt. I; S.I. 1996/2536, art. 2

As to mixing of oilU.K.

4U.K.Imposing restrictions on the mixing with other oil of any rebated oil or oil delivered without payment of duty.

As to marking of oilU.K.

5U.K.Requiring as a condition of allowing rebate on, or delivery without payment of duty of, any oil (subject to any exceptions provided by or under the regulations) that there shall have been added to that oil, at such times, in such manner and in such proportions as may be prescribed, one or more prescribed markers, with or without a prescribed colouring substance (not being a prescribed marker), and that a declaration to that effect is furnished.

Modifications etc. (not altering text)

C6Sch. 4 para 5 modified by S.I. 2004/2065, reg. 3(1A)(b) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(a))

C7Sch. 4 para 5 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d))

6U.K.Prescribing the substances which are to be used as markers.

7U.K.Providing that the presence of a marker shall be disregarded if the proportion in which it is present is less than that prescribed for the purposes of this paragraph.

8U.K.Prohibiting the addition to any oil of any prescribed marker or prescribed colouring substance except in such circumstances as may be prescribed.

Modifications etc. (not altering text)

C8Sch. 4 paras. 8-10 modified by S.I. 2004/2065, reg. 3(1A)(b) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(a))

C9Sch. 4 paras. 8-10 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d))

9U.K.Prohibiting the removal from any oil of any prescribed marker or prescribed colouring substance.

Modifications etc. (not altering text)

C10Sch. 4 paras. 8-10 modified by S.I. 2004/2065, reg. 3(1A)(b) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(a))

C11Sch. 4 paras. 8-10 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d))

10U.K.Prohibiting the addition to oil of any substance, not being a prescribed marker, which is calculated to impede the identification of a prescribed marker.

Modifications etc. (not altering text)

C12Sch. 4 paras. 8-10 modified by S.I. 2004/2065, reg. 3(1A)(b) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(a))

C13Sch. 4 paras. 8-10 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d))

11U.K.Regulating the storage or movement of prescribed markers.

12U.K.Requiring any person who adds a prescribed marker to any oil to keep in such manner and to preserve for such period as may be prescribed such accounts and records in connection with his use of that marker as may be prescribed, and requiring the production of the accounts and records.

Modifications etc. (not altering text)

C14Sch. 4 paras. 12-16 modified by S.I. 2004/2065, reg. 3(1A)(b) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(a))

C15Sch. 4 paras. 12-17 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d))

13U.K.Requiring, in such circumstances or subject to such exceptions as may be prescribed, that any drum, storage tank, delivery pump or other container or outlet which contains any oil in which a prescribed marker is present shall be marked in the prescribed manner to indicate that the oil is not to be used as road fuel or for any other prohibited purpose.

Modifications etc. (not altering text)

C16Sch. 4 paras. 12-16 modified by S.I. 2004/2065, reg. 3(1A)(b) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(a))

C17Sch. 4 paras. 12-17 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d))

14U.K.Requiring any person who supplies oil in which a prescribed marker is present to deliver to the recipient a document containing a statement in the prescribed form to the effect that the oil is not to be used as road fuel or for any other prohibited purpose.

Modifications etc. (not altering text)

C18Sch. 4 paras. 12-16 modified by S.I. 2004/2065, reg. 3(1A)(b) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(a))

C19Sch. 4 paras. 12-17 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d))

15U.K.Prohibiting the sale of any oil the colour of which would prevent any prescribed colouring substance from being readily visible if present in the oil.

Modifications etc. (not altering text)

C20Sch. 4 paras. 12-16 modified by S.I. 2004/2065, reg. 3(1A)(b) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(a))

C21Sch. 4 paras. 12-17 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d))

16U.K.Prohibiting the importation of oil in which any prescribed marker, or any other substance which is calculated to impede the identification of a prescribed marker, is present.

Modifications etc. (not altering text)

C22Sch. 4 paras. 12-16 modified by S.I. 2004/2065, reg. 3(1A)(b) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(a))

C23Sch. 4 paras. 12-17 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d))

As to control of storage, supply etc. of oil, entry of premises etc.U.K.

17U.K.Regulating the storage or movement of oil.

Modifications etc. (not altering text)

C24Sch. 4 para. 17 modified (1.9.2004) by The Biofuels and Other Fuel Substitutes (Payment of Excise Duties etc.) Regulations 2004 (S.I. 2004/2065), regs. 1(1), 3(1)(f)

C25Sch. 4 paras. 12-17 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d))

18U.K.Restricting the supplying of oil in respect of which rebate has been allowed and not repaid or on which excise duty has not been paid.

[F2918AU.K.Prohibiting the use of aviation gasoline otherwise than as a fuel for aircraft.]

Textual Amendments

F29Sch. 4 paras. 18A, 18B inserted by Finance Act 1982 (c. 39, SIF 40:1), s. 4(6)

F3018BU.K.Prohibiting the taking of aviation gasoline into fuel tanks for engines other than aircraft engines.

Textual Amendments

F30Sch. 4 paras. 18A,18B inserted by Finance Act 1982 (c. 39, SIF 40:1), s. 4(6)

19U.K.Requiring a person owning or possessing a [F31vehicle, vessel, machine or appliance] which is constructed or adapted to use heavy oil as fuel to keep such accounts and records in such manner as may be prescribed, and to preserve such books and documents relating to the supply of heavy oil to or by him, or the use of heavy oil by him, for such period as may be prescribed.

Textual Amendments

F31Words in Sch. 4 para. 19 substituted (1.4.2022) by Finance Act 2021 (c. 26), s. 102(2), Sch. 21 paras. 23(2), (5)(a)

20U.K.Requiring the production of books or documents relating to the supply or use of oil or the use of any vehicle [F32, vessel, machine or appliance].

Textual Amendments

F32Words in Sch. 4 para. 20 inserted (cond.) (1.4.2022) by Finance Act 2021 (c. 26), s. 102(2), Sch. 21 paras. 23(3), (5)(b)

21[F33(1)]Authorising the entry and inspection of premises [F34(including places of any description, and in particular tents or movable structures, other] than private dwelling-houses) and the examination of vehicles [F35, vessels, machines or appliances ], and authorising, or requiring the giving of facilities for, the inspection of oil found on any premises entered or on or in any vehicle [F36, vessel, machine or appliance ] and the taking of samples of any oil inspected.U.K.

[F37(2)In this paragraph “premises” includes any floating structure.

(3)Nothing in sub-paragraph (1) enables regulations to be made authorising the examination of the interior of part of a vessel if that part is used as a dwelling.]

Textual Amendments

F33Sch. 4 para. 21 renumbered as Sch. 4 para. 21(1) (29.6.2021 for N.I. for specified purposes, 1.10.2021 for N.I. in so far as not already in force) by Finance Act 2020 (c. 14), Sch. 11 paras. 13(4)(a), 18; S.I. 2021/740, regs. 2, 3 (with reg. 1(2))

F34Words in Sch. 4 para. 21 substituted (1.4.2022) by Finance Act 2021 (c. 26), s. 102(2), Sch. 21 para. 23(4)(a)

F35Words in Sch. 4 para. 21 substituted (cond.) (1.4.2022) by Finance Act 2021 (c. 26), s. 102(2), Sch. 21 paras. 23(4)(b), (5)(c)

F36Words in Sch. 4 para. 21 substituted (cond.) (1.4.2022) by Finance Act 2021 (c. 26), s. 102(2), Sch. 21 paras. 23(4)(c), (5)(d)

F37Sch. 4 para. 21(2)(3) inserted (29.6.2021 for N.I. for specified purposes, 1.10.2021 for N.I. in so far as not already in force) by Finance Act 2020 (c. 14), Sch. 11 paras. 13(4)(c), 18; S.I. 2021/740, regs. 2, 3 (with reg. 1(2))

Modifications etc. (not altering text)

C26Sch. 4 para. 21 modified (1.9.2004) by The Biofuels and Other Fuel Substitutes (Payment of Excise Duties etc.) Regulations 2004 (S.I. 2004/2065), regs. 1(1), 3(1)(f)

C27Sch. 4 para. 21 modified by S.I. 2004/2065, reg. 3(2A)(c) (as inserted (1.4.2008) by The Hydrocarbon Oil, Biofuels and Other Fuel Substitutes (Determination of Composition of a Substance and Miscellaneous Amendments) Regulations 2008 (S.I. 2008/753), regs. 1(2), 8(2)(d)

InterpretationU.K.

22U.K.In this Schedule—

“oil” means hydrocarbon oil;

“prescribed” means prescribed by regulations made under section 24 of this Act;

F38. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F38Words in Sch. 4 para. 22 omitted (retrospective to 1.4.2008) by virtue of Finance Act 2008 (c. 9), Sch. 5 paras. 23(b), 26(b)

Section 24(5).

SCHEDULE 5U.K. SAMPLING

1U.K.The person taking a sample—

(a)if he takes it from a [F39motor vehicle] [F39vehicle or a vessel], shall if practicable do so in the presence of a person appearing to him to be the owner or person for the time being in charge of the vehicle [F40or the vessel];

(b)if he takes the sample on any premises but not from a [F41motor vehicle] [F41vehicle or a vessel], shall if practicable take it in the presence of a person appearing to him to be the occupier of the premises or for the time being in charge of the part of the premises from which it is taken.

Textual Amendments

F39Words in Sch. 5 para. 1(a) substituted (1.10.2021 for N.I.) by Finance Act 2020 (c. 14), Sch. 11 paras. 14(2)(a)(i), 18; S.I. 2021/740, reg. 3 (with reg. 1(2))

F40Words in Sch. 5 para. 1(a) inserted (1.10.2021 for N.I.) by Finance Act 2020 (c. 14), Sch. 11 paras. 14(2)(a)(ii), 18; S.I. 2021/740, reg. 3 (with reg. 1(2))

F41Words in Sch. 5 para. 1(b) substituted (1.10.2021 for N.I.) by Finance Act 2020 (c. 14), Sch. 11 paras. 14(2)(b), 18; S.I. 2021/740, reg. 3 (with reg. 1(2))

2(1)The result of an analysis of a sample shall not be admissible—U.K.

(a)in criminal proceedings under the Customs and Excise Acts 1979; or

(b)on behalf of the Commissioners in any civil proceedings under those Acts,

unless the analysis was made by an authorised analyst and the requirements of paragraph 1 above (where applicable) and of the following provisions of this paragraph have been complied with.

(2)The person taking a sample must at the time have divided it into three parts (including the part to be analysed), marked and sealed or fastened up each part, and—

(a)delivered one part to the person in whose presence the sample was taken in accordance with paragraph 1 above, if he requires it; and

(b)retained one part for future comparison.

(3)Where it was not practicable to comply with the relevant requirements of paragraph 1 above, the person taking the sample must have served notice on the owner or person in charge of the vehicle [F42or the vessel] or, as the case may be, the occupier of the premises informing him that the sample has been taken and that one part of it is available for delivery to him, if he requires it, at such time and place as may be specified in the notice.

Textual Amendments

F42Words in Sch. 5 para. 2(3) inserted (1.10.2021 for N.I.) by Finance Act 2020 (c. 14), Sch. 11 paras. 14(3), 18; S.I. 2021/740, reg. 3 (with reg. 1(2))

3(1)Subject to sub-paragraph (2) below, in any such proceedings as are mentioned in paragraph 2(1) above a certificate purporting to be signed by an authorised analyst and certifying the presence of any substance in any such sample F43... as may be specified in the certificate shall be evidence, and in Scotland sufficient evidence, of the facts stated in it.U.K.

(2)Without prejudice to the admissibility of the evidence of the analyst (which shall be sufficient in Scotland as well as in England), such a certificate shall not be admissible as evidence—

(a)unless a copy of it has, not less than 7 days before the hearing, been served by the prosecutor or, in the case of civil proceedings, the Commissioners on all other parties to the proceedings; or

(b)if any of those other parties, not less than 3 days before the hearing or within such further time as the court may in special circumstances allow, serves notice on the prosecutor or, as the case may be, the Commissioners requiring the attendance at the hearing of the person by whom the analysis was made.

Textual Amendments

F43Words in Sch. 5 para. 3(1) omitted (retrospective to 1.4.2008) by virtue of Finance Act 2008 (c. 9), Sch. 5 paras. 24, 26(b)

4(1)Any notice required or authorised to be given under this Schedule shall be in writing.U.K.

(2)Any such notice shall be deemed, unless the contrary is shown, to have been received by a person if it is shown to have been left for him at his last-known residence or place of business in the United Kingdom.

(3)Any such notice may be given by post, and the letter containing the notice may be sent to the last-known residence or place of business in the United Kingdom of the person to whom it is directed.

(4)Any such notice given to the secretary or clerk of a company or body of persons (incorporated or unincorporated) on behalf of the company or body shall be deemed to have been given to the company or body; and for the purpose of the foregoing provisions of this paragraph any such company or body of persons having an office in the United Kingdom shall be treated as resident at that office or, if it has more then one, at the registered or principal office.

(5)Where any such notice is to be given to any person as the occupier of any land, and it is not practicable after reasonable inquiry to ascertain—

(a)what is the name of any person being the occupier of the land; or

(b)whether or not there is a person being the occupier of the land,

the notice may be addressed to the person concerned by any sufficient description of the capacity in which it is given to him.

(6)In any case to which sub-paragraph (5) above applies, and in any other case where it is not practicable after reasonable inquiry to ascertain an address in the United Kingdom for the service of a notice to be given to a person as being the occupier of any land, the notice shall be deemed to have been received by the person concerned on being left for him on the land, either in the hands of a responsible person or conspicuously affixed to some building or object on the land.

[F44(6A)In sub-paragraphs (5) and (6) “land” includes any floating structure.]

(7)Sub-paragraphs (2) to (6) above shall not affect the validity of any notice duly given otherwise than in accordance with those sub-paragraphs.

Textual Amendments

F44Sch. 5 para. 4(6A) inserted (1.10.2021 for N.I.) by Finance Act 2020 (c. 14), Sch. 11 paras. 14(4), 18; S.I. 2021/740, reg. 3 (with reg. 1(2))

5U.K.In this Schedule “authorised analyst” means—

(a)the Government Chemist or a person acting under his direction;

(b)the Government Chemist for Northern Ireland or a person acting under his direction;

(c)any chemist authorised by the Treasury to make analyses for the purposes of this Schedule; or

(d)any other person appointed as a public analyst or deputy public analyst under—

[F45section 27 of the Food Safety Act 1990], or

[F46Article 27(1) of the Food Safety (Northern Ireland) Order 1991].

Textual Amendments

F45Words substituted (E.W.S.) by virtue of Food Safety Act 1990 (c. 16, SIF 53:1, 2), s. 59(1), Sch. 3 para. 22

F46Words in Sch. 5 para. 5(d) substituted (N.I.) (21. 5.1991) by S.I. 1991/762, art. 51(1), Sch. 2 para.13; S.R. 1991/175, art. 2(1).

5N.I.In this Schedule “authorised analyst” means—

(a)the Government Chemist or a person acting under his direction;

(b)the Government Chemist for Northern Ireland or a person acting under his direction;

(c)any chemist authorised by the Treasury to make analyses for the purposes of this Schedule; or

(d)any other person appointed as a public analyst or deputy public analyst under—

[F52section 27 of the Food Safety Act 1990], or

[F53Article 27(1) of the Food Safety (Northern Ireland) Order 1991].

Textual Amendments

F52Words substituted (E.W.S.) by virtue of Food Safety Act 1990 (c. 16, SIF 53:1, 2), s. 59(1), Sch. 3 para. 22

F53Words in Sch. 5 para. 5(d) substituted (N.I.) (21.5.1991) by S.I. 1991/762, art. 1(2), Sch. 2 para.13; S.R. 1991/175, art. 2(1)

6U.K.References in this Schedule to the taking of a sample or to a sample shall be construed respectively as references to the taking of a sample in pursuance of regulations under section [F4720AA or] 24 of this Act and to a sample so taken.

Textual Amendments

F47Words inserted by Finance Act 1989 (c. 26, SIF 40:1), s. 2(2)

7U.K.This Schedule shall have effect in its application to a vehicle [F48, vessel, machine or appliance] of which a person other than the owner is, or is for the time being, entitled to possession as if for references to the owner there were substituted references to the person entitled to possession.

Textual Amendments

F48Words in Sch. 5 para. 7 inserted (1.4.2022) by Finance Act 2021 (c. 26), s. 102(2), Sch. 21 para. 24

Section 28(1).

SCHEDULE 6U.K. CONSEQUENTIAL AMENDMENTS

Finance Act 1965 and Finance Act (Northern Ireland) Act 1965U.K.

1U.K.In section 92(2) of the M1Finance Act 1965 and section 14(2) of the M2Finance Act (Northern Ireland) Act 1966 (grants towards duty on bus fuel) for the words “hydrocarbon oil” there shall be substituted the words “ heavy oil ”.

Modifications etc. (not altering text)

C28The text of s. 28(1)(2)(5), Sch. 6 paras. 1, 2 and 6, and Sch. 7 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991.

Marginal Citations

Transport Act 1968U.K.

F492U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F49Sch. 6 para. 2 repealed (1.1.1996) by 1995 c. 23, s. 60(2), Sch. 8 Pt. I (with ss. 54, 55); S.I. 1995/2181, art. 2

3, 4, 5.U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F50

Textual Amendments

F50Sch. 6 paras. 3, 4, 5 and 7 repealed by Value Added Tax Act 1983 (c. 55, SIF 40:2), s. 50(2), Sch. 11

Excise Duties (Gas as Road Fuel) Order 1972U.K.

6U.K.In Article 3 of the M3Excise Duties (Gas as Road Fuel) Order 1972 for the words “hydrocarbon oil” there shall be substituted the words “ light oil ”.

Modifications etc. (not altering text)

C29The text of s. 28(1)(2)(5), Sch. 6 paras. 1, 2 and 6, and Sch. 7 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991.

Marginal Citations

7U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F51

Textual Amendments

F51Sch. 6 paras. 3, 4, 5 and 7 repealed by Value Added Tax Act 1983 (c. 55, SIF 40:2), s. 50(2), Sch. 11

Section 28(2)

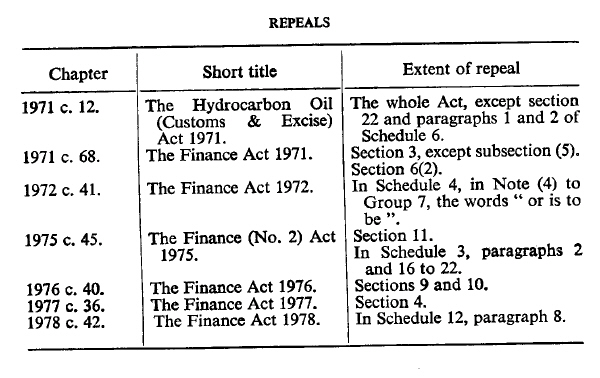

SCHEDULE 7U.K. REPEALS

Modifications etc. (not altering text)

C30The text of s. 28(1)(2)(5), Sch. 6 paras. 1, 2 and 6, and Sch. 7 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991.

Options/Help

Print Options

PrintThe Whole Act

PrintThe Schedules only

Legislation is available in different versions:

Latest Available (revised):The latest available updated version of the legislation incorporating changes made by subsequent legislation and applied by our editorial team. Changes we have not yet applied to the text, can be found in the ‘Changes to Legislation’ area.

Original (As Enacted or Made): The original version of the legislation as it stood when it was enacted or made. No changes have been applied to the text.

Point in Time: This becomes available after navigating to view revised legislation as it stood at a certain point in time via Advanced Features > Show Timeline of Changes or via a point in time advanced search.

See additional information alongside the content

Geographical Extent: Indicates the geographical area that this provision applies to. For further information see ‘Frequently Asked Questions’.

Show Timeline of Changes: See how this legislation has or could change over time. Turning this feature on will show extra navigation options to go to these specific points in time. Return to the latest available version by using the controls above in the What Version box.

Opening Options

Different options to open legislation in order to view more content on screen at once

More Resources

Access essential accompanying documents and information for this legislation item from this tab. Dependent on the legislation item being viewed this may include:

- the original print PDF of the as enacted version that was used for the print copy

- lists of changes made by and/or affecting this legislation item

- confers power and blanket amendment details

- all formats of all associated documents

- correction slips

- links to related legislation and further information resources

Timeline of Changes

This timeline shows the different points in time where a change occurred. The dates will coincide with the earliest date on which the change (e.g an insertion, a repeal or a substitution) that was applied came into force. The first date in the timeline will usually be the earliest date when the provision came into force. In some cases the first date is 01/02/1991 (or for Northern Ireland legislation 01/01/2006). This date is our basedate. No versions before this date are available. For further information see the Editorial Practice Guide and Glossary under Help.

More Resources

Use this menu to access essential accompanying documents and information for this legislation item. Dependent on the legislation item being viewed this may include:

- the original print PDF of the as enacted version that was used for the print copy

- correction slips

Click 'View More' or select 'More Resources' tab for additional information including:

- lists of changes made by and/or affecting this legislation item

- confers power and blanket amendment details

- all formats of all associated documents

- links to related legislation and further information resources

All content is available under the Open Government Licence v3.0 except where otherwise stated. This site additionally contains content derived from EUR-Lex, reused under the terms of the Commission Decision 2011/833/EU on the reuse of documents from the EU institutions. For more information see the EUR-Lex public statement on re-use.

All content is available under the Open Government Licence v3.0 except where otherwise stated. This site additionally contains content derived from EUR-Lex, reused under the terms of the Commission Decision 2011/833/EU on the reuse of documents from the EU institutions. For more information see the EUR-Lex public statement on re-use.