Tobacco Products Duty Act 1979

1979 c.7

An Act to consolidate the enactments relating to the excise duty on tobacco products.

Act amended by Value Added Tax Act 1983 (c. 55, SIF 40:2), s. 24(1)(3) and Police and Criminal Evidence Act 1984 (c. 60, SIF 95), s. 114(1)

Act modified by S.I. 1990/2167, art. 5

1 Tobacco products.

1

In this Act “tobacco products” means any of the following products, namely,—

a

cigarettes;

b

cigars;

c

hand-rolling tobacco;

d

other smoking tobacco; and

e

chewing tobacco,

which are manufactured wholly or partly from tobacco or any substance used as a substitute for tobacco, but does not include herbal smoking products.

2

Subject to subsection (3) below, in this Act “hand-rolling tobacco” means tobacco—

a

which is sold or advertised by the importer or manufacturer as suitable for making into cigarettes; or

F1aa

which is of a kind used for making into cigarettes; or

b

of which more than 25 per cent. by weight of the tobacco particles have a width of less than F21 mm.

F32A

For the purposes of subsection (2)(aa) above the use for making into cigarettes must amount to more than occasional use but need not amount to common use.

3

The Treasury may by order made by statutory instrument provide that in this Act references to cigarettes, cigars, hand-rolling tobacco, other smoking tobacco and chewing tobacco shall or shall not include references to any product of a description specified in the order, being a product manufactured as mentioned in subsection (1) above but not including herbal smoking products; and any such order may amend or repeal subsection (2) F4or (2A) above.

4

Subject to subsection (5) below, a statutory instrument by which there is made an order under subsection (3) above shall be laid before the House of Commons after being made; and unless the order is approved by that House before the expiration of 28 days beginning with the date on which it was made, it shall cease to have effect on the expiration of that period, but without prejudice to anything previously done under it or to the making of a new order.

In reckoning any such period no account shall be taken of any time during which Parliament is dissolved or prorogued or during which the House of Commons is adjourned for more than 4 days.

5

Subsection (4) above shall not apply to any order containing a statement by the Treasury that the order does not extend the incidence of the duty or involve a greater charge to duty or a reduction of any relief; and a statutory instrument by which any such order is made shall be subject to annulment in pursuance of a resolution of the House of Commons.

6

In this section “herbal smoking products” means products commonly known as herbal cigarettes or herbal smoking mixtures.

2 Charge and remission or repayment of tobacco products duty.

1

There shall be charged on tobacco products imported into or manufactured in the United Kingdom a duty of excise at the rates shown, . . . F17, in the Table in Schedule 1 to this Act.

C32

Subject to such conditions as they see fit to impose, the Commissioners shall remit or repay the duty charged by this section where it is shown to their satisfaction that the products in question have been—

a

exported or shipped as stores; or

b

used solely for the purposes of research or experiment;

and the Commissioners may by regulations provide for the remission or repayment of the duty in such other cases as may be specified in the regulations and subject to such conditions as they see fit to impose.

3. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F5

4 Calculation of duty in case of cigarettes more than 9 cm. long.

For the purposes of the references to a thousand cigarettes in paragraph 1 in the Table in Schedule 1 to this Act . . . F6 any cigarette more than 9 cm. long (excluding any filter or mouthpiece) shall be treated as if each 9 cm. or part thereof were a separate cigarette.

5 Retail price of cigarettes.

1

For the purposes of the duty chargeable at any time under section 2 above in respect of cigarettes of any description, the retail price of the cigarettes shall be taken to be—

a

in a case in which paragraph (b) below does not apply, the highest price at which cigarettes of that description are normally sold by retail at that time in the United Kingdom;

F191A

In subsection (1) above “recommended price”—

a

in relation to a case in which cigarettes of the applicable description are manufactured by a manufacturer in a member State, means any price recommended by that manufacturer; and

b

in relation to a case which does not fall within paragraph (a) above, means any price recommended by an importer of cigarettes of the applicable description.

2

The duty in respect of any number of cigarettes shall be charged by reference to the price which, in accordance with subsection (1) above, is applicable to cigarettes sold in packets of 20 or of such other number as the Commissioners may determine in relation to cigarettes of the description in question; and the whole of the price of a packet shall be regarded as referable to the cigarettes it contains notwithstanding that it also contains a coupon, token, card or other additional item.

3

In any case in which duty is chargeable in accordance with paragraph (a) of subsection (1) above—

a

the question as to what price is applicable under that paragraph shall, subject to subsection (4) below, be determined by the Commissioners; and

b

the Commissioners may require security (by deposit of money or otherwise to their satisfaction) for the payment of duty to be given pending their determination.

4

Any person who has paid duty in accordance with a determination of the Commissioners under subsection (3)(a) above and is dissatisfied with their determination may require the question of what price was applicable under subsection (1)(a) above to be referred to the arbitration of a referee appointed by the Lord Chancellor, not being an official of any government department.

5

If, on a reference to him under subsection (4) above, the referee determines that the price was lower than that determined by the Commissioners, they shall repay the duty overpaid together with interest on the overpaid duty from the date of the overpayment at such rate as the referee may determine.

6

The procedure on any reference to a referee under subsection (4) above shall be such as may be determined by the referee; and the referee’s decision on any such reference shall be final and conclusive.

6 Alteration of rates of duty.

1

The Treasury may by order made by statutory instrument increase or decrease any of the rates of duty for the time being in force under the Table in Schedule 1 to this Act by such percentage of the rate, not exceeding 10 per cent., as may be specified in the order, but any such order shall cease to be in force at the expiration of a period of one year from the date on which it takes effect unless continued in force by a further order made under this subsection.

2

In relation to any order made under subsection (1) above to continue, vary or replace a previous order so made, the reference in that subsection to the rate for the time being in force is a reference to the rate that would be in force if no order under that subsection had been made.

3

A statutory instrument under subsection (1) above by which there is made an order increasing the rate in force at the time of making the order shall be laid before the House of Commons after being made; and unless the order is approved by that House before the expiration of 28 days beginning with the date on which it was made, it shall cease to have effect on the expiration of that period, but without prejudice to anything previously done under it or to the making of a new order.

In reckoning any such period no account shall be taken of any time during which Parliament is dissolved or prorogued or during which the House of Commons is adjourned for more than 4 days.

4

A statutory instrument made under subsection (1) above to which subsection (3) above does not apply shall be subject to annulment in pursuance of a resolution of the House of Commons.

5

For the purposes of this section—

a

the percentage and the amount per thousand cigarettes in paragraph 1 in the Table in Schedule 1 to this Act shall be treated as separate rates of duty; . . . F7

b

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F7

7 Regulations for management of duty.

1

The Commissioners may with a view to managing the duty charged by section 2 above make regulations—

a

prescribing the method of charging the duty and for securing and collecting the duty;

b

for the registration of premises for the safe storage of tobacco products and for requiring the deposit of tobacco products in, and regulating their treatment in and removal from, premises so registered;

c

for the registration of premises where—

i

tobacco products are manufactured;

ii

materials for the manufacture of tobacco products are grown, produced, stored or treated; or

iii

refuse from the manufacture of tobacco products is stored or treated,

and for regulating the storage and treatment in, and removal from, premises so registered of such materials and refuse;

d

for requiring the keeping and preservation of such records, and the making of such returns, as may be specified in the regulations; and

e

for the inspection of goods, documents and premises.

2

If any person fails to comply with any regulation made under subsection (1) above F20his failure to comply shall attract a penalty under section 9 of the Finance Act 1994 (civil penalities), and any article in respect of which any person fails to comply with any such regulation, or which is found on premises in respect of which any person has failed to comply with any such regulation, shall be liable to forfeiture

8 Charge in cases of default.

1

Where the records or returns kept or made by any person in pursuance of regulations under section 2 or 7 above show that any tobacco products or materials for their manufacture are or have been in his possession or under his control, the Commissioners may from time to time require him to account for those products or materials.

2

Unless a person required under subsection (1) above to account for any products or materials proves—

a

that duty has been paid or secured under section 7 above in respect of the products or, as the case may be, products manufactured from the materials; or

b

that the products or materials are being or have been otherwise dealt with in accordance with regulations under section 2 or 7 above,

the Commissioners may require him to pay duty under section 2 above in respect of those products or, as the case may be, in respect of such products as in their opinion might reasonably be expected to be manufactured from those materials.

F213

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F88A Fiscal marks: introductory.

Fiscal marking applies to tobacco products that are—

a

cigarettes, or

b

hand-rolling tobacco.

F98B Power to alter range of products to which fiscal marking applies.

1

The Commissioners may by order made by statutory instrument amend section 8A above for the purpose of causing fiscal marking—

a

to apply to any description of tobacco products to which it does not apply, or

b

to cease to apply to any description of tobacco products to which it does apply.

2

Where fiscal marking applies to any description of tobacco products, the Commissioners may by regulations provide that fiscal marking does not apply to such products of that description as are of a description specified in the regulations.

3

A statutory instrument containing (whether alone or with other provisions) an order under subsection (1)(a) above shall not be made unless a draft of the instrument has been laid before, and approved by a resolution of, each House of Parliament.

4

A statutory instrument that—

a

contains (whether alone or with other provisions) an order under subsection (1) above, and

b

is not subject to any requirement that a draft of the instrument be laid before and approved by a resolution of each House of Parliament,

shall be subject to annulment in pursuance of a resolution of either House of Parliament.

F108C Fiscal mark regulations.

1

The Commissioners may make provision by regulations—

a

requiring the carrying of fiscal marks by tobacco products to which fiscal marking applies, and

b

as to such matters relating to fiscal marks as appear to the Commissioners to be necessary or expedient.

2

In this Act “fiscal mark” means a mark carried by tobacco products indicating all or any of the following—

a

that excise duty has been paid on the products;

b

the rate at which excise duty was paid on the products;

c

the amount of excise duty paid on the products;

d

when excise duty was paid on the products;

e

that sale of the products—

i

is only permissible on dates ascertainable from the mark;

ii

is not permissible after (or on or after) a date so ascertainable;

iii

is not permissible before (or before or on) a date so ascertainable.

3

Regulations under this section may, in particular, make provision about—

a

the contents of a fiscal mark;

b

the appearance of a fiscal mark;

c

in the case of tobacco products that have more than one layer of packaging, which of the layers is (or are) to carry a fiscal mark;

d

the positioning of a fiscal mark on the packaging of any tobacco products;

e

when tobacco products are required to carry a fiscal mark.

4

Regulations under this section may make different provision for different cases.

F118D Fiscal marks: public notices.

1

The Commissioners may by notices published by them regulate any of the matters mentioned in paragraphs (a) to (d) of section 8C(3) above.

2

A notice under this section may provide for provision made by regulations under section 8C above to have effect subject to provisions of the notice.

3

A notice under this section may make different provision for different cases.

F128E Failure to comply with fiscal mark regulations and public notices.

1

This section applies if a person fails to comply with any requirement imposed by or under—

a

regulations made under section 8C above, or

b

a notice published under section 8D above.

2

Any article in respect of which the person fails to comply with the requirement shall be liable to forfeiture.

3

The person’s failure to comply shall attract a penalty under section 9 of the M1Finance Act 1994 (civil penalties).

4

The Commissioners may by regulations make such provision as is mentioned in subsection (5) below about the calculation of the penalty in a case where the failure involves post-dating of any tobacco products.

For this purpose “post-dating” means that the products carry a fiscal mark (“the later period mark”) that—

a

is not one they are required to carry by virtue of this Act, and

b

is one they would be required to carry by virtue of this Act if the requirement to pay the duty charged on them under section 2 above took effect at a time later than that at which it in fact takes effect.

5

The provision that may be made by regulations under subsection (4) above is for the penalty to be calculated by reference to the duty currently charged on the products.

For this purpose “the duty currently charged” on the products is the amount of the duty charged under section 2 above that would be payable on the products if the requirement to pay the duty took effect at the time of the failure.

F138F Sale of marked tobacco when not permitted: penalties.

1

This section applies if provision made by or under—

a

regulations made under section 8C above, or

b

a notice published under section 8D above,

provides for any tobacco products to carry a period of sale mark.

2

In this section—

“a period of sale mark” means a fiscal mark indicating any of the matters mentioned in subsection (2)(e) of section 8C above; and

“prohibited time”, in relation to tobacco products that carry a period of sale mark, means a time when, according to the mark, sale of the products is not permissible.

3

If—

a

a person sells by way of retail sale, or exposes for retail sale, any tobacco products that carry a period of sale mark, and

b

he so sells or exposes the products at a prohibited time,

his so selling or exposing the products shall attract a penalty under section 9 of the M2Finance Act 1994 (civil penalties) and the products are liable to forfeiture.

F148G Offences: possession and sale etc. of unmarked tobacco.

1

In this section “unmarked products” means tobacco products that are subject to fiscal marking but do not carry a compliant duty-paid fiscal mark.

2

For the purposes of this section “duty-paid fiscal mark” means a fiscal mark carried by tobacco products indicating that excise duty has been paid on the products.

3

For the purposes of this section a duty-paid fiscal mark carried by tobacco products of any description is “compliant” if it complies with all relevant requirements for any duty-paid fiscal mark that by virtue of this Act is required to be carried by such tobacco products of that description as are by virtue of this Act required to carry such a mark.

For this purpose “relevant requirement” means a requirement, imposed by virtue of this Act, as to any of the matters mentioned in paragraphs (a) to (d) of section 8C(3) above (contents, appearance and positioning etc. of fiscal marks).

4

If a person—

a

is in possession of, transports or displays, or

b

sells, offers for sale or otherwise deals in,

unmarked products then, except in such cases as may be prescribed in regulations made by the Commissioners, that person commits an offence and the products are liable to forfeiture.

5

It is a defence for a person charged with an offence under subsection (4) above to prove that the unmarked products were not required by virtue of this Act to carry a duty paid fiscal mark.

6

A person guilty of an offence under subsection (4) above shall be liable on summary conviction to a fine not exceeding level 5 on the standard scale.

F158H Offences: use of premises for sale of unmarked tobacco.

1

A manager of premises commits an offence if he suffers the premises to be used for the sale of unmarked products.

In this section “unmarked products” has the same meaning as in section 8G above.

2

It is a defence for a person charged with an offence under subsection (1) above to prove that the unmarked products were not required by virtue of this Act to carry a duty-paid fiscal mark.

For this purpose “duty-paid fiscal mark” has the same meaning as in section 8G above.

3

A person guilty of an offence under subsection (1) above shall be liable on summary conviction to a fine not exceeding level 5 on the standard scale.

4

A court by or before which a person is convicted of an offence under subsection (1) above may make an order prohibiting the use of the premises in question for the sale of tobacco products during a period specified in the order.

5

The period specified in an order under subsection (4) above shall not exceed six months; and the first day of the period shall be the day specified as such in the order.

6

A manager of premises commits an offence if he suffers the premises to be used in breach of an order under subsection (4) above.

7

A person guilty of an offence under subsection (6) above shall be liable on summary conviction to a fine not exceeding level 5 on the standard scale.

8

For the purposes of this section a person is a manager of premises if he—

a

is entitled to control their use,

b

is entrusted with their management, or

c

is in charge of them.

F168J Interfering with fiscal marks: penalties.

1

This section applies where a person—

a

alters or overprints any fiscal mark carried by any tobacco products in compliance with any provision made under this Act, or

b

causes any such mark to be altered or overprinted.

2

His altering or overprinting of the mark, or his causing it to be altered or overprinted, shall attract a penalty under section 9 of the M3Finance Act 1994 (civil penalties).

3

The products that carried the mark shall be liable to forfeiture.

4

The penalty under subsection (2) above shall be calculated by reference to the duty currently charged on the products.

For this purpose “the duty currently charged” on the products is the amount of the duty charged under section 2 above that would be payable on the products if the requirement to pay the duty took effect at the time of the conduct attracting the penalty.

9 Regulations.

Any power to make regulations under this Act shall be exercisable by statutory instrument and any statutory instrument by which the power is exercised shall be subject to annulment in pursuance of a resolution of either House of Parliament.

10 Interpretation.

1

In this Act—

“hand-rolling tobacco” has the meaning given by section 1(2) above; and

“tobacco products” has the meaning given by section 1(1) above.

2

This Act and the other Acts included in the Customs and Excise Acts 1979 shall be construed as one Act but where a provision of this Act refers to this Act that reference is not to be construed as including a reference to any of the others.

3

Any expression used in this Act or in any instrument made under this Act to which a meaning is given by any other Act included in the Customs and Excise Acts 1979 has, except where the context otherwise requires, the same meaning in this Act or in any such instrument as in that Act; and for ease of reference the Table below indicates the expressions used in this Act to which a meaning is given by any other such Act—

Customs and Excise Management Act 1979

“the Commissioners”

“the Customs and Excise Acts 1979”

“goods”

“importer”

“shipped”

“stores”.

11 Repeals, savings and transitional and consequential provisions.

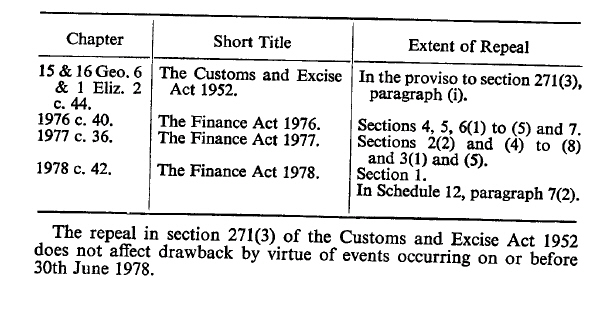

C41

The enactments specified in Schedule 2 to this Act are hereby repealed to the extent specified in the third column of that Schedule, but subject to the provision at the end of that Schedule.

2

Any provision of this Act relating to anything done or required or authorised to be done under or by reference to that provision or any other provision of this Act shall have effect as if any reference to that provision, or that other provision, as the case may be, included a reference to the corresponding provision of the enactments repealed by this Act.

C43

In section 3(2) of the M4Finance Act 1977 (which makes provision in consequence of the replacement from 1st January 1978 of duty under section 4 of the M5Finance Act 1964 with duty under the M6Finance Act 1976) for the words “the said Act of 1964” there shall be substituted the words “the Finance Act 1964”, for the words “the said Act of 1976”there shall be substituted the words “the Finance Act 1976” and after the words “the said 1st January” there shall be inserted the words “or under section 2 of the Tobacco Products Duty Act 1979 on or after 1st April 1979”.

4

Nothing in this section shall be taken as prejudicing the operation of sections 15 to 17 of the M7Interpretation Act 1978 (which relate to the effect of repeals).

12 Citation and commencement.

1

This Act may be cited as the Tobacco Products Duty Act 1979 and is included in the Acts which may be cited as the Customs and Excise Acts 1979.

2

This Act shall come into operation on 1st April 1979

SCHEDULES

SCHEDULE 1 Table of Rates of Tobacco Products Duty

Sch. 1 table substituted (1.1.1995) by 1995 c. 4, s. 11(1)(2).

1. Cigarettes | An amount equal to 20 per cent. of the retail price plus £57.64 per thousand cigarettes. |

2. Cigars | £85.61 per kilogram. |

3. Hand-rolling tobacco | £85.94 per kilogram. |

4. Other smoking tobacco and chewing tobacco | £37.64 per kilogram.] |

SCHEDULE 1 Table of Rates of Tobacco Products Duty

Sch. 1 table substituted (retrospectively with effect from 6 p.m. 29.11.1994) by 1995 c. 4, s. 10(1)(2).

1. Cigarettes | An amount equal to 20 per cent. of the retail price plus £55.58 per thousand cigarettes. |

2. Cigars | £82.56 per kilogram. |

3. Hand-rolling tobacco | £85.94 per kilogram. |

4. Other smoking tobacco and chewing tobacco | £36.30 per kilogram.] |

X1SCHEDULE 2 REPEALS

The text of Sch. 2 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991.

Act wholly in force at 1.4.1979 see s. 12(2)