Finance Act 1990

1990 c. 29

An Act to grant certain duties, to alter other duties, and to amend the law relating to the National Debt and the Public Revenue, and to make further provision in connection with Finance.

X1X2Most Gracious Sovereign,WE, Your Majesty’s most dutiful and loyal subjects, the Commons of the United Kingdom in Parliament assembled, towards raising the necessary supplies to defray Your Majesty’s public expenses, and making an addition to the public revenue, have freely and voluntarily resolved to give and grant unto Your Majesty the several duties hereinafter mentioned; and do therefore most humbly beseech Your Majesty that it may be enacted, and be it enacted by the Queen’s most Excellent Majesty, by and with the advice and consent of the Lords Spiritual and Temporal, and Commons, in this present Parliament assembled, and by the authority of the same, as follows:—

General amendments to Tax Acts, Income Tax Acts, and/or Corporation Tax Acts made by legislation after 1.2.1991 are noted against Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1) but not against each Act

Part I Customs and Excise and Value Added Tax

chapter I Customs and Excise

Rates of duty

1 Spirits, beer, wine, made-wine and cider.

1

In section 5 of the M1Alcoholic Liquor Duties Act 1979 (spirits) for “£15.77” there shall be substituted “

£17.35

”

.

2

In section 36 of that Act (beer) for “£0.90” there shall be substituted “

£0.97

”

.

3

For the Table of rates of duty in Schedule 1 to that Act (wine and made-wine) there shall be substituted the Table in Schedule 1 to this Act.

4

In section 62(1) of that Act (cider) for “£17.33” there shall be substituted “

£18.66

”

.

5

This section shall be deemed to have come into force at 6 o’clock in the evening of 20th March 1990.

2 Tobacco products.

1

For the Table in Schedule 1 to the M2Tobacco Products Duty Act 1979 there shall be substituted—

TABLE

1. Cigarettes

An amount equal to 21 per cent. of the retail price plus £34.91 per thousand cigarettes.

2. Cigars

£53.67 per kilogram.

3. Hand-rolling tobacco

£56.63 per kilogram.

4. Other smoking tobacco and chewing tobacco

£24.95 per kilogram.

2

This section shall be deemed to have come into force on 23rd March 1990.

3 Hydrocarbon oil.

1

In section 6 of the M3Hydrocarbon Oil Duties Act 1979—

a

in subsection (1), for “£0.2044”

(duty on light oil) and “£0.1729”

(duty on heavy oil) there shall be substituted “

£0.2248

”

and “

£0.1902

”

respectively; and

b

subsection (2A) (special rate of duty on petrol below 4 star) shall cease to have effect.

2

In section 11(1) of that Act, for “£0.0077”

(rebate on fuel oil) and “£0.0110”

(rebate on gas oil) there shall be substituted “

£0.0083

”

and “

£0.0118

”

respectively.

3

In section 13A(1) of that Act (rebate on unleaded petrol), for “£0.0272” there shall be substituted “

£0.0299

”

.

4

In section 14(1) of that Act (rebate on light oil for use as furnace fuel), for “£0.0077” there shall be substituted “

£0.0083

”

.

F1695

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6

Subsections (1) to (4) above shall be deemed to have come into force at 6 o’clock in the evening of 20th March 1990.

4 Pool betting duty.

1

In section 7(1) of the M4Betting and Gaming Duties Act 1981 (which specifies 42½ per cent. as the rate of pool betting duty), for the words “42½ per cent.” there shall be substituted the words “

40 per cent.

”

.

2

This section shall apply in relation to bets made at any time by reference to an event taking place on or after 6th April 1990.

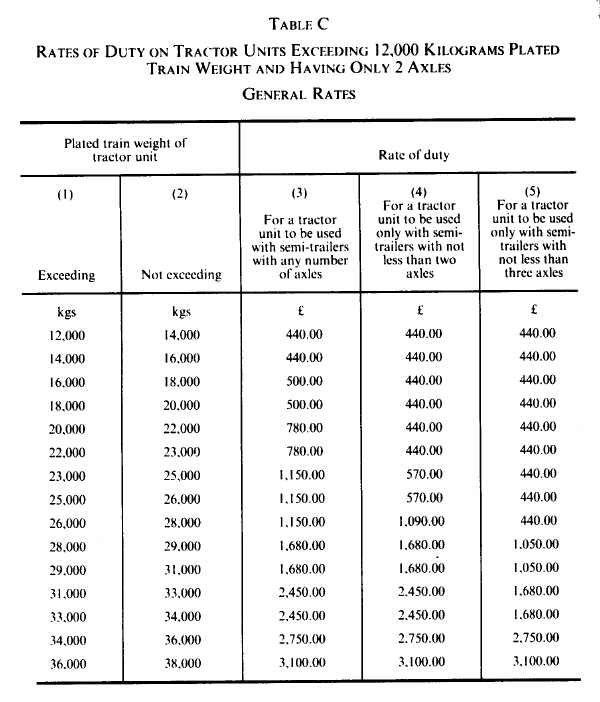

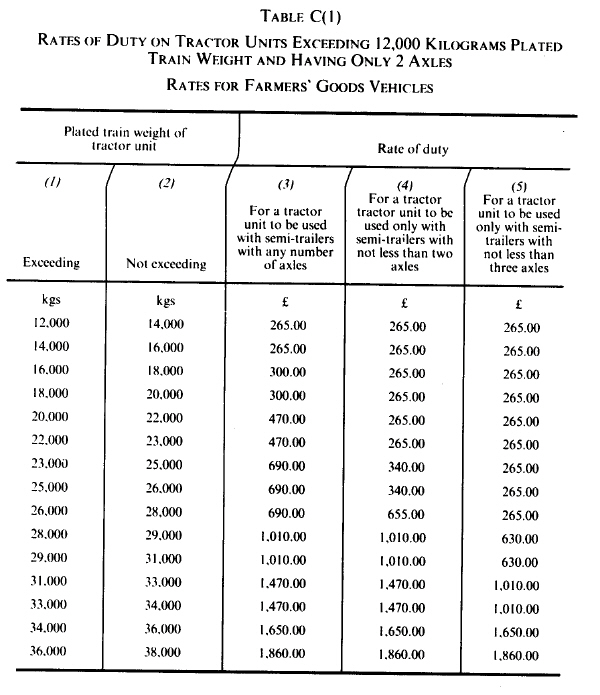

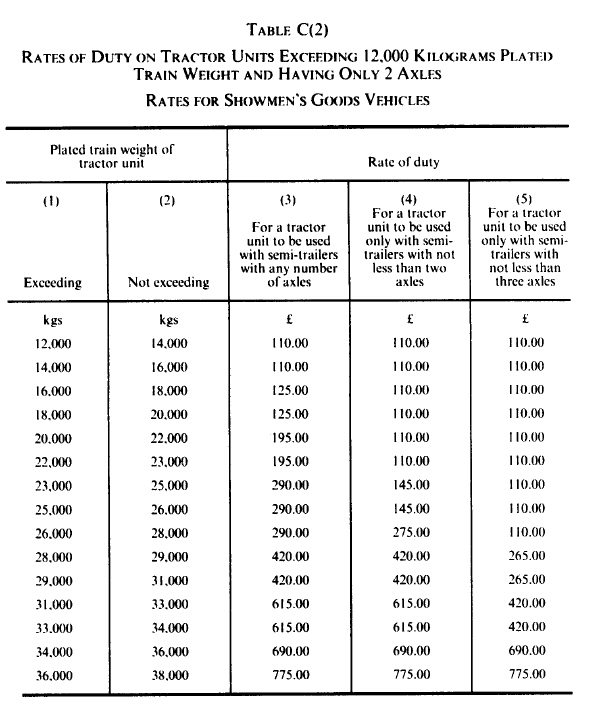

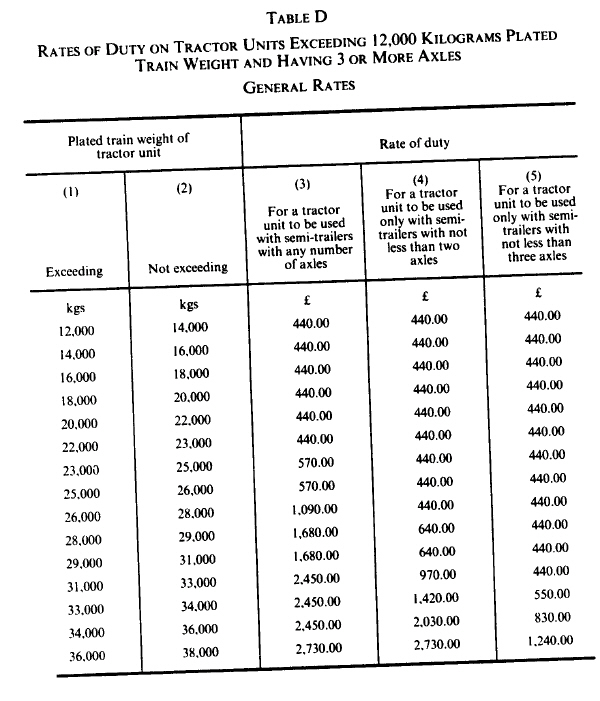

5 Vehicles excise duty.

F11

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F12

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F13

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F24

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F35

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F26

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F47

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F18

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F19

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Other provisions

F56. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7 Entry of goods on importation.

Schedule 3 to this Act (which amends the provisions of the M5Customs and Excise Management Act 1979 about initial and supplementary entries and postponed entry) shall have effect in relation to goods imported on or after the day on which this Act is passed.

F1548 Spirits methylated abroad.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9 Lodgings for officers in charge of distillery.

In section 12 of the Alcoholic Liquor Duties Act 1979 (licence to manufacture spirits) subsections (6) to (9) (requirement that distiller provide lodgings for officers in charge of distillery) shall cease to have effect.

chapter II Value Added Tax

F610. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F711. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F812. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F913. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1014. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1115. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1216. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Part II Income Tax, Corporation Tax and Capital Gains Tax

Chapter I General

Income tax rates and allowances

F15717 Rates and main allowances.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F15818 Relief for blind persons.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Corporation tax rates

C119 Charge and rate of corporation tax for 1990.

Corporation tax shall be charged for the financial year 1990 at the rate of 35 per cent.

F18620 Small companies.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Benefits in kind

F14121 Care for children.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

22 Car benefits.

1

In Schedule 6 to the Taxes Act 1988 (taxation of directors and others in respect of cars) for Part I (tables of flat rate cash equivalents) there shall be substituted—

Part I Tables of Flat Rate Cash Equivalents

Table ACars with an original market value up to £19,250 and having a cylinder capacity

Cylinder capacity of car in cubic centimetres

Age of car at end of relevant year of assessment

Under 4 years

4 years or more

1400 or less

£1,700

£1,150

More than 1400 but not more than 2000

£2,200

£1,500

More than 2000

£3,550

£2,350

Table BCars with an original market value up to £19,250 and not having a cylinder capacity

Original market value of car

Age of car at end of relevant year of assessment

Under 4 years

4 years or more

Less than £6,000

£1,700

£1,150

£6,000 or more but less than £8,500

£2,200

£1,500

£8,500 or more but not more than £19,250

£3,550

£2,350

Table CCars with an original market value of more than £19,250

Original market value of car

Age of car at end of relevant year of assessment

Under 4 years

4 years or more

More than £19,250 but not more than £29,000

£4,600

£3,100

More than £29,000

£7,400

£4,900

(2) This section shall have effect for the year 1990-91 and subsequent years of assessment.

Mileage allowances

F1323. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Charities

F1424. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

25 Donations to charity by individuals.

F1611

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1612

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1613

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1613A

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1614

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615A

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615B

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615C

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615D

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615E

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615F

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615G

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615H

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615I

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1615J

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1616

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1617

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1618

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1619

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1619A

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F18710

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F18910A

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F16011

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F18812

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F15913

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F19026 Company donations to charity.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

27 Maximum qualifying company donations.

F151

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1912

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F153

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1924

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Savings

28 Tax-exempt special savings accounts.

F1501

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1502

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F16F1503

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F15129 Extension of SAYE.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

30 Building societies.

Schedule 5 to this Act (which contains provisions relating to building societies, deposit-takers and investors) shall have effect.

Insurance companies and friendly societies

F20241 Apportionment of income etc.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20342 Overseas life assurance business.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F14743 Deduction for policy holders’ tax.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F14944 Reinsurance commissions.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

45 Policy holders’ share of profits etc.

F2041

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2042

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2043

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2044

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1485

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F276

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2047

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F288

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F299

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20510

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20511

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F3046. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F3147. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F20648 Transfers of long term business.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

49 Friendly societies: increased tax exemption.

F2071

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2072

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2073

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2074

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5

In paragraph 3(8)(b)(ii) of Schedule 15 to that Act (amount of premiums to be disregarded in determining whether a policy meets conditions for it to be a qualifying policy), after the word “premiums” there shall be inserted the words “

or, where those premiums are payable otherwise than annually, an amount equal to 10 per cent. of those premiums if that is greater

”

.

F20850 Friendly societies: application of enactments.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Unit and investment trusts etc.

F3251. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

52 Unit trusts: repeals.

1

The Taxes Act 1988 shall have effect subject to the following provisions of this section.

2

In section 468 (authorised unit trusts) subsection (5) shall not apply as regards a distribution period beginning after 31st December 1990.

3

Where a particular distribution period is by virtue of subsection (2) above the last distribution period as regards which section 468(5) applies in the case of a trust, the trustees’ liability to income tax in respect of any source of income chargeable under Case III of Schedule D shall be assessed as if they had ceased to possess the source of income on the last day of that distribution period.

4

But where section 67 of the Taxes Act 1988 applies by virtue of subsection (3) above, it shall apply with the omission from subsection (1)(b) of the words from “and shall” to “this provision”.

5

Section 468B (certified unit trusts: corporation tax) shall not apply as regards an accounting period ending after 31st December 1990.

6

Section 468C (certified unit trusts: distributions) shall not apply as regards a distribution period ending after 31st December 1990.

7

Section 468D (funds of funds: distributions) shall not apply as regards a distribution period ending after 31st December 1990.

8

In this section “distribution period” has the same meaning as in section 468 of the Taxes Act 1988.

F16853 Unit trust managers: exemption from bond-washing provisions.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F3354. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F19355 Investment trusts.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Securities

F3456. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F3557 Deep gain securities.

1

In Schedule 11 to the M6Finance Act 1989 (deep gain securities) paragraph 1 (meaning of deep gain security) shall be amended as follows.

2

The following sub-paragraph shall be inserted after sub-paragraph (3)—

3A

In the case of a security issued on or after 9th June 1989, for the purposes of sub-paragraph (2) above “redemption” does not include any redemption which may be made before maturity only if—

a

the person who issued the security fails to comply with the duties imposed on him by the terms of issue,

b

the person who issued the security becomes unable to pay his debts, or

c

the security was issued by a company and a person gains control of the company in pursuance of the acceptance of an offer made by that person to acquire shares in the company.

3

The amendment made by this section shall be deemed always to have had effect.

F3658. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F3759. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Oil industry

F3860. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F3961. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

62 CT treatment of PRT repayment.

F1941

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1942

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F195F1963

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F4063. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F4164. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

International

F4265. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F4366. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

67 Dual resident companies: controlled foreign companies.

F441

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F442

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3

In Schedule 25 to that Act—

a

paragraphs 2(1)(c) and 4(1)(c) shall be omitted,

F175b

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F175c

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4

Subsections (1) and (2) above shall apply on and after 20th March 1990 and subsection (3) above shall apply to dividends paid on or after that date.

68 Movements of capital between residents of member States.

F1761

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1762

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3

M7In section 98 of the Taxes Management Act 1970 (penalties for failure to furnish information and for false information)—

a

in subsection (1), after the words “Subject to” there shall be inserted the words “

the provisions of this section and

”

;

F177b

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F177c

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F177d

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4

This section shall apply to transactions carried out on or after 1st July 1990.

69 European Economic Interest Groupings.

Schedule 11 to this Act (which makes provision about the taxation of income and gains in the case of European Economic Interest Groupings) shall have effect.

F4570. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Miscellaneous

71 Relief for interest.

For the year 1990-91 the qualifying maximum defined in section 367(5) of the Taxes Act 1988 (limit on relief for interest on certain loans) shall be £30,000.

F4672. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F4773. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F4874. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F4975. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F17276 Training and enterprise councils and local enterprise companies.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F14277 Expenses of entertainers.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F17378 Waste disposal.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F14379 Priority share allocations for employees etc.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

80 Broadcasting: transfer of undertakings of Independent Broadcasting Authority and Cable Authority.

Schedule 12 to this Act shall have effect.

81 Futures and options: exemptions.

1

F50. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2

The following section shall be inserted at the end of Part XIV of the Taxes Act 1988 (pension schemes etc.)—

659A Futures and options.

1

For the purposes of sections 592(2), 608(2)(a), 613(4), 614(3) and (4), 620(6) and 643(2)—

a

“investments” (or “investment”)

includes futures contracts and options contracts, and

b

income derived from transactions relating to such contracts shall be regarded as income derived from (or income from) such contracts,

and paragraph 7(3)(a) of Schedule 22 to this Act shall be construed accordingly.

2

For the purposes of subsection (1) above a contract is not prevented from being a futures contract or an options contract by the fact that any party is or may be entitled to receive or liable to make, or entitled to receive and liable to make, only a payment of a sum (as opposed to a transfer of assets other than money) in full settlement of all obligations.

F513

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4

Section 659 of the Taxes Act 1988 (financial futures and traded options) shall cease to have effect.

5

Subsections (1) and (2) above apply in relation to income derived after the day on which this Act is passed.

F516

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7

Insofar as section 659 of the Taxes Act 1988 relates to provisions of that Act, subsection (4) above applies in relation to income derived after the day on which this Act is passed.

8

Insofar as section 659 of the Taxes Act 1988 relates to section 149B of the M8Capital Gains Tax Act 1979, subsection (4) above applies in relation to disposals made after the day on which this Act is passed.

F5282. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F5383. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F5484. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F5585. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F5686. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F5787. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

88 Capital allowances: miscellaneous amendments.

Schedule 13 to this Act shall have effect.

89 Correction of errors in Taxes Act 1988.

Schedule 14 to this Act shall have effect.

Chapter II Management

Returns and information

90 Income tax returns.

1

The following sections shall be substituted for sections 8 and 9 of the M9Taxes Management Act 1970 (return of income)—

8 Personal return.

1

For the purposes of assessing a person to income tax, he may be required by a notice given to him by an inspector—

a

to make and deliver to the inspector within the time limited by the notice a return containing such information as may be required in pursuance of the notice, and

b

to deliver with the return such accounts and statements, relating to information contained in the return, as may be required in pursuance of the notice.

2

Every return under this section shall include a declaration by the person making the return to the effect that the return is to the best of his knowledge correct and complete.

3

A notice under this section may require different information, accounts and statements for different periods or in relation to different descriptions of source of income.

4

Notices under this section may require different information, accounts and statements in relation to different descriptions of person.

8A Trustee’s return.

1

For the purpose of assessing a trustee of a settlement, and the settlors and beneficiaries, to income tax an inspector may by a notice given to the trustee require the trustee—

a

to make and deliver to the inspector within the time limited by the notice a return containing such information as may be required in pursuance of the notice, and

b

to deliver with the return such accounts and statements, relating to information contained in the return, as may be required in pursuance of the notice;

and a notice may be given to any one trustee or separate notices may be given to each trustee or to such trustees as the inspector thinks fit.

2

Every return under this section shall include a declaration by the person making the return to the effect that the return is to the best of his knowledge correct and complete.

3

A notice under this section may require different information, accounts and statements for different periods or in relation to different descriptions of source of income.

4

Notices under this section may require different information, accounts and statements in relation to different descriptions of settlement.

9 Partnership return.

1

Where a trade or profession is carried on by two or more persons jointly, for the purposes of making an assessment to income tax in the partnership name an inspector may act under subsection (2) or (3) below (or both).

2

An inspector may by a notice given to the partners require such person as is identified in accordance with rules given with the notice—

a

to make and deliver to the inspector within the time limited by the notice a return containing such information as may be required in pursuance of the notice, and

b

to deliver with the return such accounts and statements as may be required in pursuance of the notice.

3

An inspector may by a notice given to any partner require the partner—

a

to make and deliver to the inspector within the time limited by the notice a return containing such information as may be required in pursuance of the notice, and

b

to deliver with the return such accounts and statements as may be required in pursuance of the notice;

and a notice may be given to any one partner or separate notices may be given to each partner or to such partners as the inspector thinks fit.

4

Every return under this section shall include—

a

a declaration of the names and residences of the partners;

b

a declaration by the person making the return to the effect that the return is to the best of his knowledge correct and complete.

5

A notice under this section may require different information, accounts and statements for different periods or in relation to different descriptions of source of income.

6

Notices under this section may require different information, accounts and statements in relation to different descriptions of partnership.

2

In section 12 of that Act (information about chargeable gains)—

a

in subsection (1) for the words “Section 8” there shall be substituted the words “

Sections 8 and 8A

”

and for the words “it applies” there shall be substituted the words “

they apply

”

;

F180b

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

c

in subsection (4) the words “of income of a partnership” shall be omitted.

3

In section 93 of that Act (penalties) in subsection (1) for the words “9 of this Act (or either” there shall be substituted the words “

8A or 9 of this Act (or any

”

.

4

In section 95 of that Act (penalties) in subsection (1)(a) for the words “9 of this Act (or either” there shall be substituted the words “

8A or 9 of this Act (or any

”

.

5

This section applies where a notice to deliver a return was, or falls to be, given after 5th April 1990.

F5891. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

92 Information powers relating to interest.

1

Section 17 of the M10Taxes Management Act 1970 (interest paid or credited by banks etc. without deduction of income tax) shall be amended as mentioned in subsections (2) and (3) below.

2

In subsection (1)—

a

after the words “without deduction of income tax” there shall be inserted the words “

or after deduction of income tax

”

;

b

after the words “the amount of the interest” there shall be inserted the words “

actually paid or credited and (where the interest was paid or credited after deduction of income tax) the amount of the interest from which the tax was deducted and the amount of the tax deducted

”

;

c

paragraph (a) of the proviso shall be omitted.

3

The following subsections shall be inserted after subsection (4)—

5

The Board may by regulations provide as mentioned in all or any of the following paragraphs—

a

that a return under subsection (1) above shall contain such further information as is prescribed if the notice requiring the return specifies the information and requires it to be contained in the return;

b

that a person required to make and deliver a return under subsection (1) above shall furnish with the return such further information as is prescribed if the notice requiring the return specifies the information and requires it to be so furnished;

c

that if a person is required to furnish information under any provision made under paragraph (b) above, and the notice requiring the return specifies the form in which the information is to be furnished, the person shall furnish the information in that form;

d

that a notice under subsection (1) above shall not require prescribed information;

and in this subsection “prescribed” means prescribed by the regulations.

6

Regulations under subsection (5) above—

a

shall be made by statutory instrument subject to annulment in pursuance of a resolution of the House of Commons,

b

may make different provision in relation to different cases or descriptions of case, and

c

may include such supplementary, incidental, consequential or transitional provisions as appear to the Board to be necessary or expedient.

4

Section 18 of that Act (interest paid without deduction of income tax) shall be amended as mentioned in subsections (5) and (6) below.

5

In subsection (1)—

a

after the words “without deduction of income tax” there shall be inserted the words “

or after deduction of income tax

”

;

b

in paragraph (b) for the words “so paid or received” there shall be substituted the words “

actually paid or received and (where the interest has been paid or received after deduction of income tax) the amount of the interest from which the tax has been deducted and the amount of the tax deducted

”

;

c

for the words “its amount” there shall be substituted the words “

the amount actually received and (where the interest has been received after deduction of income tax) the amount of the interest from which the tax has been deducted and the amount of the tax deducted

”

.

6

The following subsections shall be inserted after subsection (3A)—

3B

The Board may by regulations provide as mentioned in all or any of the following paragraphs—

a

that a person required to furnish information under subsection (1) above shall furnish at the same time such further information as is prescribed if the notice concerned specifies the information and requires it to be so furnished;

b

that if a person is required to furnish information under subsection (1) above or under any provision made under paragraph (a) above, and the notice concerned specifies the form in which the information is to be furnished, the person shall furnish the information in that form;

c

that a notice under subsection (1) above shall not require prescribed information;

and in this subsection “prescribed” means prescribed by the regulations.

3C

Regulations under subsection (3B) above—

a

shall be made by statutory instrument subject to annulment in pursuance of a resolution of the House of Commons,

b

may make different provision in relation to different cases or descriptions of case, and

c

may include such supplementary, incidental, consequential or transitional provisions as appear to the Board to be necessary or expedient.

7

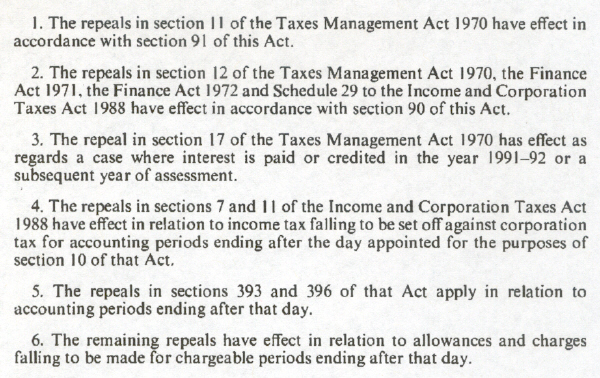

Subsections (1) to (3) above shall have effect as regards a case where interest is paid or credited in the year 1991-92 or a subsequent year of assessment.

8

Subsections (4) to (6) above shall have effect as regards a case where interest is paid in the year 1991-92 or a subsequent year of assessment.

93 Restrictions on Board’s power to call for information.

1

In section 20 of the M11Taxes Management Act 1970 (powers to call for information), after subsection (7) there shall be inserted—

7A

A notice under subsection (2) above is not to be given unless the Board have reasonable grounds for believing—

a

that the person to whom it relates may have failed or may fail to comply with any provision of the Taxes Acts; and

b

that any such failure is likely to have led or to lead to serious prejudice to the proper assessment or collection of tax.

2

This section shall apply with respect to notices given on or after the day on which this Act is passed.

F5994. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Corporation tax determinations

F6095. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F6196. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Claims by companies

F6297. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

98 Repayment of income tax deducted at source.

1

The Taxes Act 1988 shall be amended as follows.

2

In section 7(2) (set off against corporation tax of income tax deducted from payments received by resident companies) the words from “and accordingly” to the end shall be omitted.

F633

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4

In section 11(3) (set off against corporation tax of income tax deducted from payments received by non-resident companies) the words from “and accordingly” to the end shall be omitted.

5

This section applies in relation to income tax falling to be set off against corporation tax for accounting periods ending after the day appointed for the purposes of section 10 of the Taxes Act 1988 (pay and file).

F19799 Loss relief.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F64100. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F65101. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F66102. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F67103. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Miscellaneous

104 Officers.

1

In section 1 of the M12Taxes Management Act 1970 (appointment of inspectors etc.) the following subsections shall be inserted after subsection (2)—

2A

The Board may appoint a person to be an inspector or collector for general purposes or for such specific purposes as the Board think fit.

2B

Where in accordance with the Board’s administrative practices a person is authorised to act as an inspector or collector for specific purposes, he shall be deemed to have been appointed to be an inspector or collector for those purposes.

2

In section 55 of that Act (recovery of tax not postponed)—

a

in subsection (7) for the words “the inspector” there shall be substituted the words “

an inspector

”

;

F68b

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3

The amendment made by subsection (1) above shall be deemed always to have had effect.

4

The amendments made by subsection (2) above shall apply where notice of appeal is given on or after the day on which this Act is passed.

105 Recovery of excessive repayments of tax.

1

In section 30 of the M13Taxes Management Act 1970 (recovery of excessive repayments of tax) the following subsection shall be inserted after subsection (1)—

1A

Subsection (1)

above shall not apply where the amount of tax which has been repaid is assessable under section 29 of this Act.

2

This section applies in relation to amounts of tax repaid on or after the day on which this Act is passed.

106 Corporation tax: collection.

In section 10 of the Taxes Act 1988 (time for payment of tax) the following subsection shall be substituted for subsection (2)—

2

Where by virtue of subsection (1)(a) above corporation tax for an accounting period of a company is due without the making of an assessment, the amount for the time being shown in a return by the company under section 11 of the Management Act (corporation tax return) as the corporation tax for the period shall be treated for the purposes of Part VI of the Management Act (collection and recovery) as tax charged and due and payable under an assessment on the company.

Part IIIStamp Duty and Stamp Duty Reserve Tax

Repeals

F69107 Stamp duty to be abolished on bearer instruments.

1

Stamp duty shall not be chargeable under Schedule 15 to the Finance Act 1999 (bearer instruments).

2

Subsection (1) above applies in relation to the charge under paragraph 1 of that Schedule (charge on issue) where the instrument is issued on or after the abolition day.

3

Subsection (1) above applies in relation to the charge under paragraph 2 of that Schedule (charge on transfer of stock) where the stock constituted by or transferable by means of the instrument is transferred on or after the abolition day.

108 Transfer of securities: abolition of stamp duty.

F1451

Stamp duty shall not be chargeable under Schedule 13 to the Finance Act 1999 (transfer of securities) F167or section 67(3) or 70(3) of the Finance Act 1986 (stamp duty on certain transfers to depositary receipt systems and clearance systems).

7

Subject to subsection (8) below, this section applies if the instrument is executed in pursuance of a contract made on or after the abolition day.

8

In the case of an instrument—

a

which falls within section 67(1) or (9) of the M14Finance Act 1986 (depositary receipts) or section 70(1) or (9) of that Act (clearance services), or

b

which does not fall within section 67(1) or (9) or section 70(1) or (9) of that Act and is not executed in pursuance of a contract,

this section applies if the instrument is executed on or after the abolition day.

109 Stamp duty: other repeals.

1

Section 83 of the M15Stamp Act 1891 (fine for certain acts relating to securities) shall not apply where an instrument of assignment or transfer is executed, or a transfer or negotiation of the stock constituted by or transferable by means of a bearer instrument takes place, on or after the abolition day.

2

The following provisions (which relate to the cancellation of certain instruments) shall not apply where the stock certificate or other instrument is entered on or after the abolition day—

a

section 109(1) of the Stamp Act 1891,

b

section 5(2) of the M16Finance Act 1899,

F70c

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F70d

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3

Section 67 of the M17Finance Act 1963 (prohibition of circulation of blank transfers) shall not apply where the sale is made on or after the abolition day; and section 16 of the M18Finance Act (Northern Ireland) 1963 (equivalent provision for Northern Ireland) shall not apply where the sale is made on or after the abolition day.

4

No person shall be required to notify the Commissioners under section 68(1) or (2) or 71(1) or (2) of the Finance Act 1986 (depositary receipts and clearance services) if he first issues the receipts, provides the services or holds the securities as there mentioned on or after the abolition day.

5

No company shall be required to notify the Commissioners under section 68(3) or 71(3) of that Act if it first becomes aware as there mentioned on or after the abolition day.

6

The following provisions shall cease to have effect—

F70a

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F70b

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

c

section 33 of the M19Finance Act 1970 (composition by financial institutions in respect of stamp duty),

d

section 127(7) of the M20Finance Act 1976 (extension of composition provisions to Northern Ireland), and

e

section 85 of the M21Finance Act 1986 (provisions about stock, marketable securities, etc.).

7

The provisions mentioned in subsection (6) above shall cease to have effect as provided by the Treasury by order.

8

An order under subsection (7) above—

a

shall be made by statutory instrument;

b

may make different provision for different provisions or different purposes;

c

may include such supplementary, incidental, consequential or transitional provisions as appear to the Treasury to be necessary or expedient.

F709

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

110 Stamp duty reserve tax: abolition.

1

Stamp duty reserve tax shall cease to be chargeable.

2

In relation to the charge to tax under section 87 of the Finance Act 1986 subsection (1) above applies where—

a

the agreement to transfer is conditional and the condition is satisfied on or after the abolition day, or

b

the agreement is not conditional and is made on or after the abolition day.

3

In relation to the charge to tax under section 93(1) of that Act subsection (1) above applies where securities are transferred, issued or appropriated on or after the abolition day (whenever the arrangement was made).

4

In relation to the charge to tax under section 96(1) of that Act subsection (1) above applies where securities are transferred or issued on or after the abolition day (whenever the arrangement was made).

5

In relation to the charge to tax under section 93(10) of that Act subsection (1) above applies where securities are issued or transferred on sale, under terms there mentioned, on or after the abolition day.

6

In relation to the charge to tax under section 96(8) of that Act subsection (1) above applies where securities are issued or transferred on sale, under terms there mentioned, on or after the abolition day.

7

Where before the abolition day securities are issued or transferred on sale under terms mentioned in section 93(10) of that Act, in construing section 93(10) the effect of subsections (1) and (3) above shall be ignored.

8

Where before the abolition day securities are issued or transferred on sale under terms mentioned in section 96(8) of that Act, in construing section 96(8) the effect of subsections (1) and (4) above shall be ignored.

111 General.

1

In sections 107 to 110 above “the abolition day” means such day as may be appointed by the Treasury by order made by statutory instrument.

2

Sections 107 to 109 above shall be construed as one with the M22Stamp Act 1891.

International organisations

114 International organisations.

1

In section 126 of the M25Finance Act 1984 (tax exemptions in relation to designated international organisations) in subsection (3) the following paragraph shall be inserted after paragraph (c)—

d

no stamp duty reserve tax shall be chargeable under section 93 (depositary receipts) or 96 (clearance services) of the Finance Act 1986 in respect of the issue of securities by the organisation.

2

Where an organisation or body is designated under section 126(1) or (4) before the day on which this Act is passed, subsection (1) above applies in relation to the issue of securities by the organisation or body on or after that day.

3

Where an organisation or body is designated under section 126(1) or (4) on or after the day on which this Act is passed, subsection (1) above applies in relation to the issue of securities by the organisation or body after the designation.

Part IVMiscellaneous and General

Ports levy

F72115. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F73116. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F74117. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F75118. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F76119. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F77120. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Petroleum revenue tax

121 Limit on PRT repayment interest where loss carried back.

1

Schedule 2 to the M26Oil Taxation Act 1975 (management and collection of PRT) shall be amended as follows.

2

At the beginning of paragraph 16 (interest on repayments)

there shall be inserted the words “

Subject to paragraph 17 below

”

.

3

After that paragraph there shall be inserted the following paragraph—

17

1

This paragraph applies where—

a

an assessment made on a participator for a chargeable period or an amendment of such an assessment (in this paragraph referred to as “the relevant assessment or amendment”) gives effect to relief under subsection (2) or subsection (3) of section 7 of this Act for one or more allowable losses accruing in a later chargeable period (in this paragraph referred to, in relation to the relevant assessment or amendment, as “the relief for losses carried back”); and

b

the later chargeable period referred to in paragraph (a) above ends after 30th June 1991; and

c

an amount of tax becomes repayable to the participator by virtue of the relevant assessment or amendment (whether wholly or partly by reason of giving effect to the relief for losses carried back).

2

In the following provisions of this paragraph, so much of the repayment of tax referred to in sub-paragraph (1)(c) above as is attributable to giving effect to the relief for losses carried back is referred to as “the appropriate repayment”.

3

For the purpose of determining the amount of the appropriate repayment in a case where the relevant assessment or amendment not only gives effect to the relief for losses carried back but also takes account of any other matter (whether a relief or not) which goes to reduce the assessable profit of the period in question or otherwise to reduce the tax payable for that period, the amount of the repayment which is attributable to the relief for losses carried back is the difference between—

a

the total amount of tax repayable by virtue of the relevant assessment or amendment; and

b

the amount of tax (if any) which would have been so repayable if no account had been taken of the relief for losses carried back.

4

Where this paragraph applies, the amount of interest which, by virtue of paragraph 16 above, is carried by the appropriate repayment shall not exceed the difference between—

a

85 per cent. of the allowable loss or losses referred to in sub-paragraph (1)(a) above; and

b

the amount of the appropriate repayment.

F183122 Variation, on account of fraudulent or negligent conduct, of decision on expenditure claim etc.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Miscellaneous

F78123. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F184124 Inheritance tax: restriction on power to require information.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

125 Information for tax authorities in other member States.

F1701

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1712

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1793

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1794

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1465

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1786

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F209126 Pools payments for football ground improvements.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

127 Definition of “local authority” for certain tax purposes.

F1851

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F792

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3

Schedule 18 to this Act (consequential amendments) shall have effect.

4

This section shall be deemed to have come into force on 1st April 1990.

C2C4128 Repayment of fees and charges.

1

This section applies where at the beginning of the day on which this Act is passed—

a

an enactment confers power to make provision for payment of a fee or charge (however described), and

b

sums paid in pursuance of provision made in exercise of the power are payable into the Consolidated Fund.

2

Subject to subsection (3) below, the enactment shall be treated as also conferring power to make provision about repayment of sums paid, or purported to be paid, in pursuance of provision made in exercise of the power.

3

Subsection (2) above shall not apply if the fee or charge is one—

a

repayment of which is prohibited or regulated by an enactment, or

b

power to make provision about repayment of which is expressly conferred, or expressly negatived, to any extent.

4

Without prejudice to the generality of the power conferred by virtue of subsection (2) above, the provision which may be made by virtue of that subsection includes provision—

a

that repayment shall be made only if a specified person is satisfied that specified conditions are met or in other specified circumstances;

b

that repayment shall be made in part only;

c

that, in the case of partial repayment, the amount repaid shall be a specified sum or determined in a specified manner; and

d

for repayment of different amounts in different circumstances.

5

In subsection (4) above “specified” means specified in the instrument exercising the power.

6

In determining for the purposes of this section whether sums are payable into the Consolidated Fund, section 3 of the M27Government Trading Funds Act 1973 (payments into a trading fund) shall be disregarded.

7

In this section “enactment” includes Northern Ireland legislation as defined in section 24(5) of the M28Interpretation Act 1978.

8

An Order in Council under paragraph 1(1)(b) of Schedule 1 to the M29Northern Ireland Act 1974 (legislation for Northern Ireland in the interim period) which states that it is made only for purposes corresponding to those of this section—

a

shall not be subject to sub-paragraphs (4) and (5) of paragraph 1 of that Schedule (affirmative resolution of both Houses of Parliament); but

b

shall be subject to annulment in pursuance of a resolution of either House.

129 Settlement of stock disputes by deputy registrars.

In section 5 of the M30National Debt Act 1972 (settlement by Chief Registrar of friendly societies of disputes as to holdings on National Savings Stock Register)—

a

in subsection (1), after the words “Chief Registrar of friendly societies” there shall be inserted the words “

or a deputy appointed by him

”

,

b

in subsection (2), after the words “Chief Registrar” there shall be inserted the words “

or deputy

”

,

c

in subsection (3)(a), after the words “Chief Registrar of friendly societies” there shall be inserted the words “

or a deputy appointed by him

”

, and

d

subsection (3)(b) shall cease to have effect.

130 Limit for local loans.

In section 4(1) of the M31National Loans Act 1968 (which provides that the aggregate of any commitments of the Public Works Loan Commissioners in respect of undertakings to grant local loans and any amount outstanding in respect of the principal of such loans shall not exceed £42,000 million or such other sum not exceeding £50,000 million as the Treasury may specify by order) for the words “£42,000 million” and “£50,000 million” there shall be substituted respectively “

£55,000 million

”

and “

£70,000 million

”

.

General

131 Interpretation etc.

1

2

Chapter II of Part I of this Act shall be construed as one with the M34Value Added Tax Act 1983.

3

Part II of this Act, so far as it relates to capital gains tax, shall be construed as one with the M35Capital Gains Tax Act 1979.

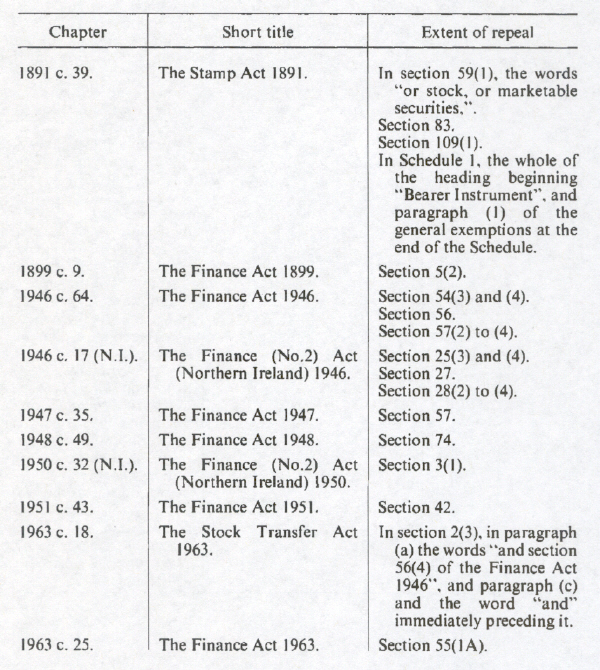

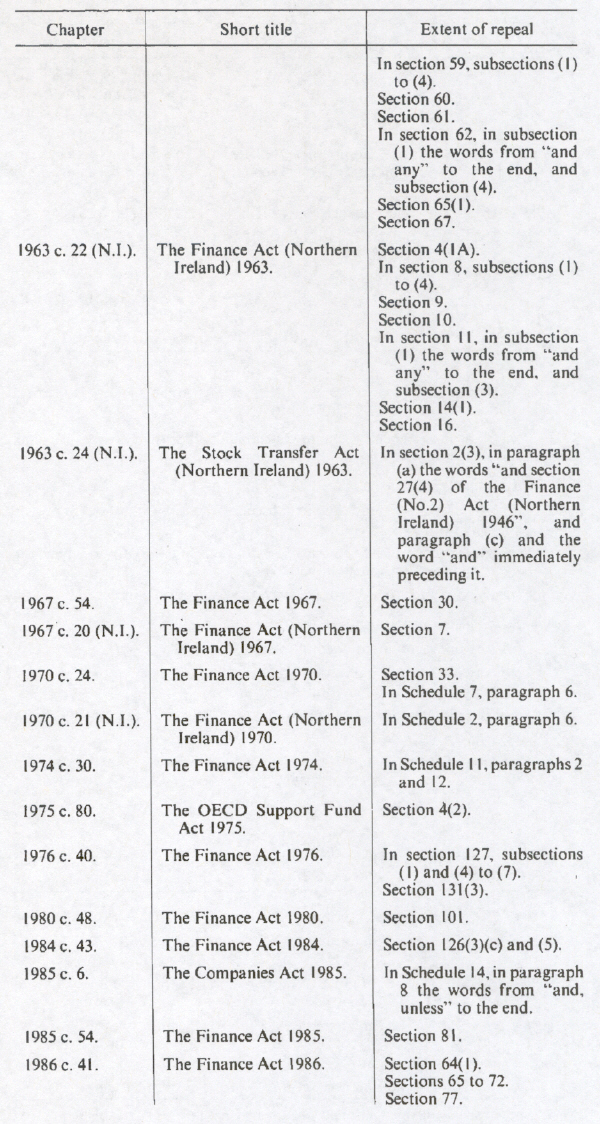

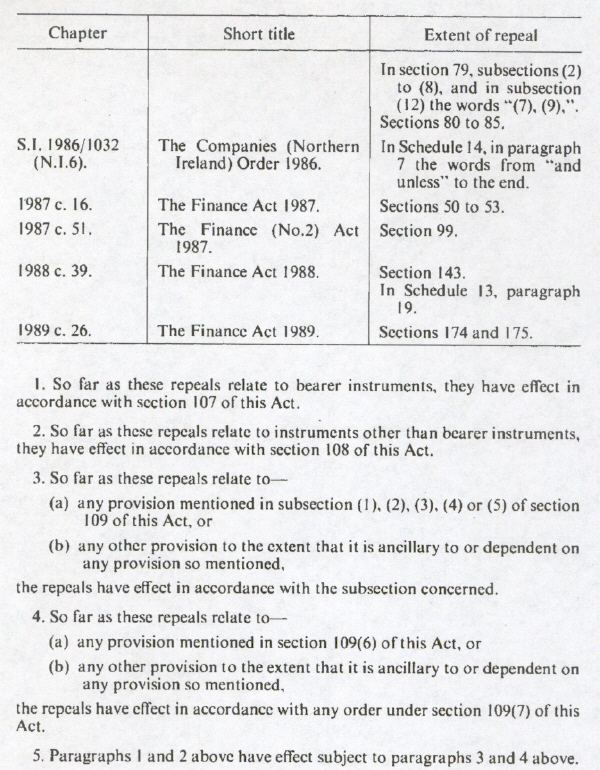

132 Repeals.

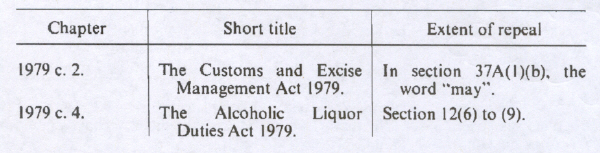

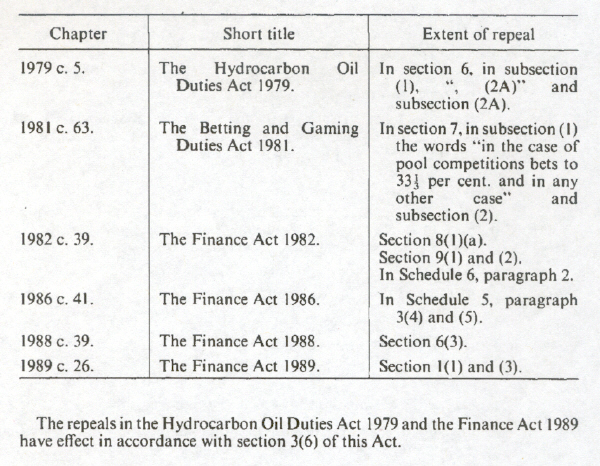

The enactments specified in Schedule 19 to this Act (which include spent or unnecessary enactments) are hereby repealed to the extent specified in the third column of that Schedule, but subject to any provision at the end of any Part of that Schedule.

133 Short title.

This Act may be cited as the Finance Act 1990.

SCHEDULES

SCHEDULE 1 Table of Rates of Duty on Wine and Made-Wine

Description of wine or made-wine | Rates of duty per hectolitre |

|---|---|

£ | |

Wine or made-wine of a strength not exceeding 2 per cent. | 11.03 |

Wine or made-wine of a strength exceeding 2 per cent. but not exceeding 3 per cent. | 18.38 |

Wine or made-wine of a strength exceeding 3 per cent. but not exceeding 4 per cent. | 25.73 |

Wine or made-wine of a strength exceeding 4 per cent. but not exceeding 5 per cent. | 33.09 |

Wine or made-wine of a strength exceeding 5 per cent. but not exceeding 5.5 per cent. | 40.44 |

Wine or made-wine of a strength exceeding 5.5 per cent. but not exceeding 15 per cent. and not being sparkling | 110.28 |

Sparkling wine or sparkling made-wine of a strength exceeding 5.5 per cent. but not exceeding 15 per cent. | 182.10 |

Wine or made-wine of a strength exceeding 15 per cent. but not exceeding 18 per cent. | 190.20 |

Wine or made-wine of a strength exceeding 18 per cent. but not exceeding 22 per cent. | 219.40 |

Wine or made-wine of a strength exceeding 22 per cent. | 219.40 plus £17.35 for every 1 per cent. or part of 1 per cent. in excess of 22 per cent. |

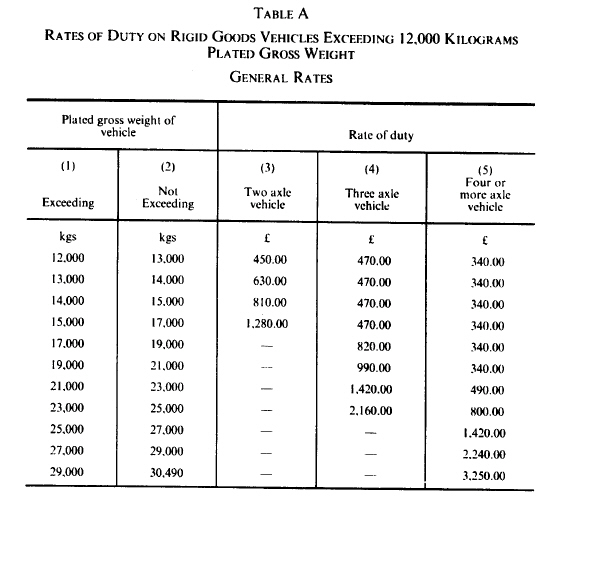

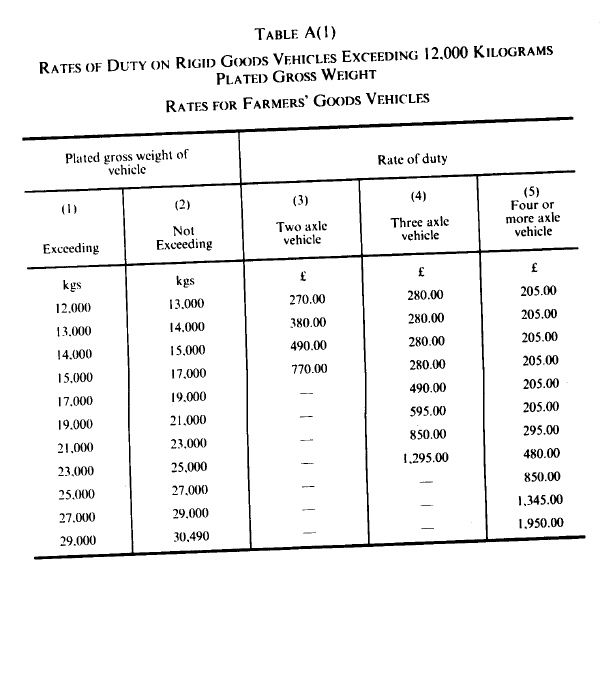

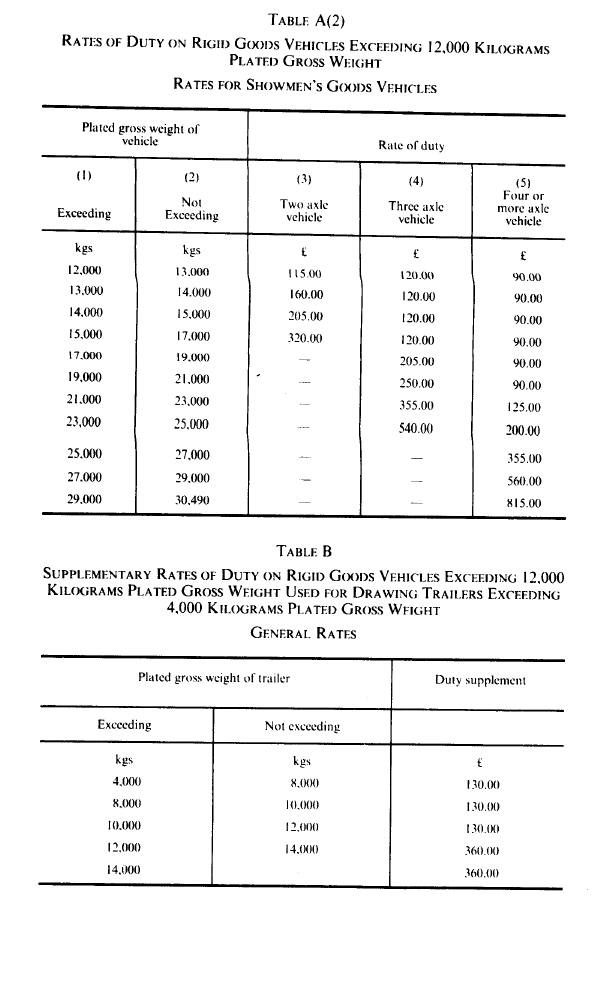

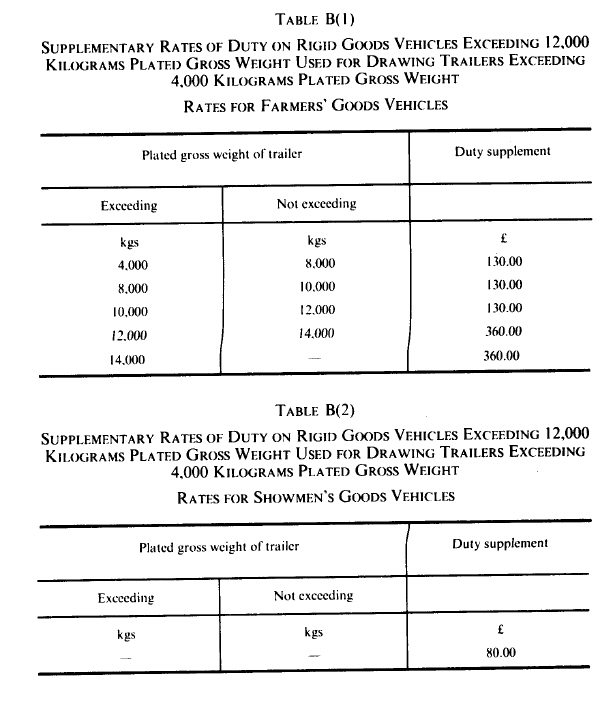

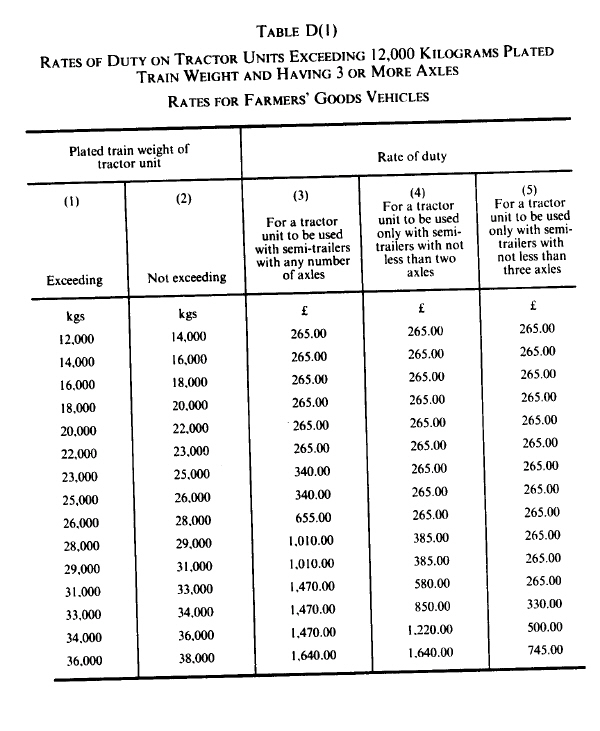

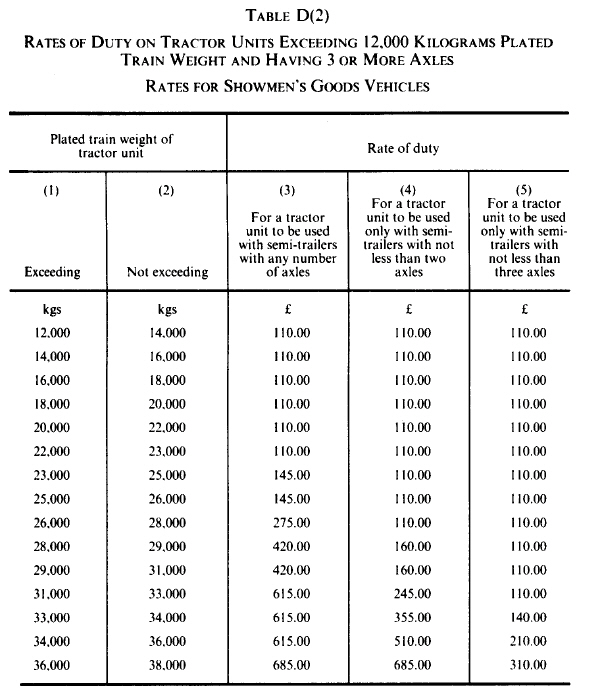

SCHEDULE 2 Vehicles Excise Duty: Rates

F80Part I

Sch. 2 Pt. I repealed (1.9.1994) by 1994 c. 22, ss. 65, 66(1), Sch. 5 Pt. I (with s. 57(4), Sch. 4 para. 6)

Part II Amendments of Part I of Schedule 4 to the 1971 Act

F811

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F822

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F833

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F844

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F855

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6

F861

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F874

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F887

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F898

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F909

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F93Part III

Sch. 2 Pt. III (paras. 10-11) repealed(1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt.IV; S.I. 1991/2021, art.2.

F9110

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F9211

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F94Part IV Tables Substituted in Part II of Schedule 4 to the 1971 Act and the 1972 Act

Sch. 2 Pt. IV repealed (8.11.1993) by S.I. 1993/2452, art. 3, Sch. 2.

SCHEDULE 3 Entry of Goods on Importation

1

The M36Customs and Excise Management Act 1979 shall be amended as follows.

2

1

Section 37A (initial and supplementary entries) shall be amended as follows.

2

In subsection (1)(b), the word “may” shall be omitted.

3

The following subsection shall be inserted after subsection (1)—

1A

Without prejudice to section 37 above, a direction under that section may—

a

provide that where the importer is not authorised for the purposes of this section but a person who is so authorised is appointed as his agent for the purpose of entering the goods, the entry may consist of an initial entry made by the person so appointed and a supplementary entry so made; and

b

make such supplementary provision in connection with entries consisting of initial and supplementary entries made as mentioned in paragraph (a) above as the Commissioners think fit.

4

In subsection (2), for the words from the beginning to “unpaid duty,” there shall be substituted the words—

2

Where—

a

an initial entry made under subsection (1) above has been accepted and the importer has given security by deposit of money or otherwise to the satisfaction of the Commissioners for payment of the unpaid duty, or

b

an initial entry made under subsection (1A) above has been accepted and the person making the entry on the importer’s behalf has given such security as is mentioned in paragraph (a) above,

the goods may

5

In subsection (3) after the words “initial entry” there shall be inserted the words “

under subsection (1) above

”

.

6

The following subsection shall be inserted after subsection (3)—

3A

A person who makes an initial entry under subsection (1A)

above on behalf of an importer shall complete the entry by delivering the supplementary entry within such time as the Commissioners may direct.

3

1

Section 37B (postponed entry) shall be amended as follows.

2

The following subsection shall be inserted after subsection (1)—

1A

The Commissioners may, if they think fit, direct that where—

a

such goods as may be specified in the direction are imported by an importer who is not authorised for the purposes of this subsection;

b

a person who is authorised for the purposes of this subsection is appointed as his agent for the purpose of entering the goods;

c

the person so appointed has delivered a document relating to the goods to the proper officer, in such form and manner, containing such particulars and accompanied by such documents as the Commissioners may direct; and

d

the document has been accepted by the proper officer,

the goods may be delivered before an entry of them has been delivered or any duty chargeable in respect of them has been paid.

3

The following subsections shall be inserted after subsection (3)—

3A

The Commissioners may, if they think fit, direct that where—

a

such goods as may be specified in the direction are imported by an importer who is not authorised for the purposes of this subsection;

b

a person who is authorised for the purposes of this subsection is appointed as his agent for the purpose of entering the goods;

c

the goods have been removed from the place of importation to a place approved by the Commissioners for the clearance out of charge of such goods; and

d

the conditions mentioned in subsection (3B) below have been satisfied,

the goods may be delivered before an entry of them has been delivered or any duty chargeable in respect of them has been paid.

3B

The conditions are that—

a

on the arrival of the goods at the approved place the person appointed as the agent of the importer for the purpose of entering the goods delivers to the proper officer a notice of the arrival of the goods in such form and containing such particulars as may be required by the directions;

b

within such time as may be so required the person appointed as the agent of the importer for the purpose of entering the goods enters such particulars of the goods and such other information as may be so required in a record maintained by him at such place as the proper officer may require; and

c

the goods are kept secure in the approved place for such period as may be required by the directions.

4

In subsection (4), after “(3)(a)” there shall be inserted “

or (3B)(a)

”

.

5

In subsection (5), for the words “this section” there shall be substituted the words “

subsection (1) or (2) above

”

.

6

The following subsection shall be inserted after subsection (5)—

5A

No goods shall be delivered under subsection (1A)

or (3A) above unless the person appointed as the agent of the importer for the purpose of entering the goods gives security by deposit of money or otherwise to the satisfaction of the Commissioners for the payment of any duty chargeable in respect of the goods which is unpaid.

7

In subsection (6), for the words “this section” there shall be substituted the words “

subsection (1) or (2) above

”

.

8

The following subsection shall be inserted after subsection (6)—

6A

Where goods of which no entry has been made have been delivered under subsection (1A) or (3A) above, the person appointed as the agent of the importer for the purpose of entering the goods shall deliver an entry of the goods under section 37(1) above within such time as the Commissioners may direct.

9

In subsection (7)—

a

in paragraph (a), after “(1)” there shall be inserted “

or (1A)

”

; and

b

after paragraph (b) there shall be inserted the words

and

c

in the case of goods delivered by virtue of a direction under subsection (3A) above, on the date on which particulars of the goods were entered as mentioned in subsection (3B)(b) above.

4

1

Section 37C (provisions supplementary to sections 37A and 37B) shall be amended as follows.

2

In subsection (1)(a)—

a

for the word “importer” there shall be substituted the word “

person

”

; and

b

for the words “or (2)” there shall be substituted the words “

, (1A), (2) or (3A)

”

.

3

In subsection (1)(b), for the word “importer” there shall be substituted the word “

person

”

.

4

In subsection (2)(a), for the word “importer” there shall be substituted the word “

person

”

.

F95SCHEDULE 4

Sch 4 repealed (11.5.2001 with effect for the year 2002-03 and for subsequent years of assessment) by 2001 c. 9, s. 110, Sch. 33 Pt. 2(1)

SCHEDULE 5 Building Societies and Deposit-Takers

Introduction

1

The Taxes Act 1988 shall be amended as mentioned in paragraphs 2 to 14 below.

Building societies

2

1

Section 476 (building societies: regulations for payment of tax) shall cease to have effect.

2

This paragraph shall apply as regards the year 1991-92 and subsequent years of assessment.

3

1

Section 477 (investments becoming or ceasing to be relevant building society investments) shall cease to have effect.

2

This paragraph shall apply as regards any time falling on or after 6th April 1991.

F2014

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Deposit-takers

5

1

Section 479 (interest paid on deposits with banks etc.) shall cease to have effect.

2

This paragraph shall apply as regards interest paid or credited on or after 6th April 1991.

6

1

Section 480 (deposits becoming or ceasing to be composite rate deposits) shall cease to have effect.

2

This paragraph shall apply as regards any time falling on or after 6th April 1991.

F1567

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1568

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1569

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

General

F15610

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F15611

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

12

1

In section 483 (determination of reduced rate for building societies and composite rate for banks etc.) subsections (1) to (3) and (5) shall cease to have effect.

2

This paragraph shall apply where the first year of assessment mentioned in section 483(1) is 1990-91 or a subsequent year of assessment.

13

1

In section 686 (liability to additional rate tax of certain income of discretionary trusts) subsection (5) shall cease to have effect.

2

This paragraph shall apply as regards a sum paid or credited on or after 6th April 1991.

14

1

In section 687 (payments under discretionary trusts) in subsection (3) the words following paragraph (i) shall cease to have effect.

2

This paragraph shall apply as regards an amount paid or credited on or after 6th April 1991.

Management

15

In the Table in section 98 of the M37Taxes Management Act 1970 (penalties for failure to comply with notices etc.) there shall be inserted in the first and second columns, after the entry relating to regulations under section 476(1) of the Taxes Act 1988— “

regulations under section 477A(1);

”

.

Transitional provision

F16216

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

SCHEDULE 6 Life Assurance: Apportionment of Income etc.

F2101

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1552

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F963

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2114

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F975

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F986

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1657

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2128

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1639

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F9910

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11

1

F164...

a

in so far as it relates to determinations of profits in accordance with section 83 of the M38Finance Act 1989, this Schedule shall apply in relation to any period for which such a determination falls to be made, other than a period for which it falls to be made only by virtue of an election under section 83(5) of the Finance Act 1989, and

b

in so far as it relates to section 432A of the Taxes Act 1988, this Schedule shall apply to income arising, and disposals occurring, on or after 1st January 1990.

2

Subject to sub-paragraph (1) above, this Schedule shall be deemed to have come into force on 1st January 1990.

3

The preceding provisions of this paragraph shall have effect subject to paragraph 12 below.

12

1

Where at the end of 1989 the assets of an insurance company include securities of a class some of which are regarded as a single 1982 holding, and the rest of which are regarded as a single new holding, for the purposes of corporation tax on chargeable gains—

a

at the beginning of 1990 there shall be both a 1982 holding and a new holding of the description mentioned in any paragraph of section 440A(2) of the Taxes Act 1988 within which any of the securities fall at that time (whether or not there would be apart from this sub-paragraph), and

b

the 1982 holding and the new holding of the description mentioned in any such paragraph shall at that time bear to one another the same proportions as the single 1982 holding and the single new holding at the end of 1989.

2

For the period beginning with 1st January 1990 and ending with 19th March 1990, section 440(4) of the Taxes Act 1988 (as substituted by paragraph 8 of this Schedule) and section 440A(2) of that Act shall have effect with the omission of paragraph (d) (so that all assets not within paragraphs (a) to (c) fall within paragraph (e)).

3

Sub-paragraph (4) below applies where—

a

at the end of 19th March 1990 the assets of an insurance company include securities of a class some of which are regarded as a relevant 1982 holding, and others of which are regarded as a relevant new holding, for the purposes of corporation tax on chargeable gains, and

b

some of the securities are included in the company’s long term business fund but others are not;

and for the purposes of this sub-paragraph a holding is a “relevant” holding if it is not linked to pension business or basic life assurance business and is not an asset of the overseas life assurance fund.

4

Where this sub-paragraph applies—

a

at the beginning of 20th March 1990 there shall be both a 1982 holding and a new holding of each of the descriptions mentioned in paragraphs (d) and (e) of section 440A(2) of the Taxes Act 1988 (whether or not there would be apart from this sub-paragraph), and

b

the 1982 holding and the new holding of each of those descriptions shall at that time bear to one another the same proportions as the 1982 holding and the new holding mentioned in sub-paragraph (3)(a) above at the end of 19th March 1990.

5

Except for the purposes of determining the assets of a company which are linked solely to basic life assurance business, the amendments made by this Schedule shall have effect in relation to a company with the omission of references to overseas life assurance business as respects any time before the provisions of Schedule 7 to this Act have effect in relation to the company.

6

Sub-paragraph (7) below applies where—

a

the first accounting period of an insurance company beginning on or after 1st January 1990 begins after 20th March 1990,

b

at some time during the accounting period the company carries on overseas life assurance business, and

c

immediately before the beginning of the accounting period the assets of the long term business fund of the company include both a relevant 1982 holding and a relevant new holding of securities of the same class;

and for the purposes of this sub-paragraph a holding is a “relevant” holding if it is not linked to pension business or basic life assurance business.

7

Where this sub-paragraph applies—

a

at the beginning of the accounting period there shall be both a 1982 holding and a new holding of each of the descriptions mentioned in paragraphs (c) and (d) of section 440A(2) of the Taxes Act 1988 (whether or not there would be apart from this sub-paragraph), and

b

the 1982 holding and the new holding of each of those descriptions shall at that time bear to one another the same proportions as the 1982 holding and the new holding mentioned in sub-paragraph (6)(c) above immediately before the beginning of the period.

8

No disposal or re-acquisition shall be deemed to occur by virtue of section 440 of the Taxes Act 1988 (as substituted by paragraph 8 of this Schedule) by reason only of the coming into force (in accordance with the provisions of paragraph 11 of this Schedule and this paragraph) of any provision of section 440A of that Act.

9

The substitution made by paragraph 8 of this Schedule shall not affect—

a

the operation of section 440 of the Taxes Act 1988 (as it has effect before the substitution) before 20th March 1990, or

b

the operation of subsections (6) and (7) of that section (as they have effect before the substitution) in relation to the disposal of an asset which has not been deemed to be disposed of by virtue of section 440 (as it has effect after the substitution) before the time of the disposal.

10

F216SCHEDULE 7 Overseas Life Assurance Business

Sch. 7 omitted (17.7.2012) by virtue of Finance Act 2012 (c. 14), Sch. 16 para. 247(b)(v)

F2161

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2162

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2163

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2164

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2165

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2166

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2167

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2168

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F2169

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F21610

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F106SCHEDULE 8

Sch. 8 repealed (6.3.1992 with effect as mentioned in s. 289 (1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), s. 290, Sch. 12 (with ss. 60, 101(1), 201(3), Sch. 11 paras. 22, 26(2), 27) and subject to amendments (17.2.1995) by S.I. 1995/171, reg. 4(2) and (10.8.1995) by S.I. 1992/1655, regs. 19A, 19B (as inserted by S.I. 1995/1916, reg. 9 ))

General

F1001

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Exemption for certain linked assets

F1012

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Replacement of assets

F1023

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1034

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1045

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Supplementary

F1056

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

SCHEDULE 9 Insurance Companies: Transfers of Long Term Business

Capital gains

F1071

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F1082

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Accounting periods

F1663

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Expenses of management and losses

F2134

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Capital allowances

F1095

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Transfer to friendly society

F2146

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Commencement

F2157

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F110SCHEDULE 10

Sch. 10 repealed (29.4.1996 with effect in accordance with the provisions of Chapter II of Part IV of the amending Act) by 1996 c. 8, ss. 104, 205, Sch. 14 para. 58, Sch. 41 Pt. V(3) Note (with Sch. 15 para. 21)

Part I Introduction

Qualifying provision for redemption

1

For the purposes of this Schedule a qualifying provision for redemption, in relation to a security, is a provision which—

a

provides for redemption before maturity only at the option of the person holding the security for the time being,

b

provides for such redemption on one occasion only,

c

provides for such redemption to occur on the last day of an income period, and

d

is such that the amount payable on redemption on exercise of the option is fixed (as opposed to variable), is determined at the time the security becomes subject to the provision, and constitutes a deep gain.

Qualifying convertible securities

2

1

For the purposes of this Schedule a security is a qualifying convertible security at the time of its issue if—

a

it fulfils each of the first eight conditions mentioned below, and

b

it fulfils the ninth condition mentioned below (where it applies) or it fulfils the ninth and tenth conditions mentioned below (where they apply).

2

The first condition is that the security was issued by a company on or after 9th June 1989.

3

The second condition is that the security—

a

is not a share in a company,

b

is redeemable, and

c

was not issued in circumstances such that, by virtue of section 209(2)(c) of the Taxes Act 1988, it (or part of it) constituted or fell within a distribution of a company.