SCHEDULES

SCHEDULE 39U.K.Stamp duty land tax and stamp duty

Part 2U.K.Re-enactment, with changes, of amendments made by section 109 regulations

Introduction and revocationU.K.

14(1)This Part of this Schedule contains amendments to Parts 4 and 5 of the Finance Act 2003 (c. 14) (stamp duty land tax and stamp duty) corresponding, subject to certain changes, to those made by the Stamp Duty and Stamp Duty Land Tax (Variation of the Finance Act 2003) (No. 2) Regulations 2003 (S.I. 2003/2816) (made under section 109 of that Act).U.K.

(2)Those regulations are revoked.

Meaning of taking possessionU.K.

15(1)Section 44 (contract and conveyance) is amended as follows.U.K.

(2)In subsection (5)(a) (meaning of “substantial performance”: purchaser taking possession), after “the purchaser” insert “ , or a person connected with the purchaser, ”.

(3)In subsection (6) (meaning of taking possession)—

(a)for paragraph (a) substitute—

“(a)possession includes receipt of rents and profits or the right to receive them, and”; and

(b)in paragraph (b), for “the purchaser takes possession” substitute “ possession is taken ”.

(4)After subsection (10) add—

“(11)Section 839 of the Taxes Act 1988 (connected persons) has effect for the purposes of this section.”.

Relief for sale and leaseback arrangementsU.K.

16U.K.After section 57 (disadvantaged areas relief) insert—

“57ASale and leaseback arrangements

(1)The leaseback element of a sale and leaseback arrangement is exempt from charge if the qualifying conditions specified below are met.

(2)A “sale and leaseback”arrangement means an arrangement under which—

(a)A transfers or grants to B a major interest in land (the “sale”), and

(b)out of that interest B grants a lease to A (the “leaseback”).

(3)The qualifying conditions are—

(a)that the sale transaction is entered into wholly or partly in consideration of the leaseback transaction being entered into,

(b)that the only other consideration (if any) for the sale is the payment of money or the assumption, satisfaction or release of a debt (or both),

(c)that the sale is not a transfer of rights within the meaning of section 45 (contract and conveyance: effect of transfer of rights) or 45A (contract providing for conveyance to third party: effect of transfer of rights), and

(d)where A and B are both bodies corporate at the effective date of the leaseback transaction, that they are not members of the same group for the purposes of group relief (see paragraph 1 of Schedule 7) at that date.

(4)In this section—

“debt” means an obligation, whether certain or contingent, to pay a sum of money either immediately or at a future date; and

“money” means money in sterling or another currency.”.

Relief for certain acquisitions of residential propertyU.K.

17(1)For sections 58 and 59 (relief for certain exchanges of residential property and relocation relief) substitute—U.K.

“58ARelief for certain acquisitions of residential property

Schedule 6A provides for relief in the case of certain acquisitions of residential property.”.

(2)After Schedule 6 insert—

Section 58A

“SCHEDULE 6AU.K.Relief for certain acquisitions of residential property

Acquisition by house-building company from individual acquiring new dwelling

1(1)Where a dwelling (“the old dwelling”) is acquired by a house-building company from an individual (whether alone or with other individuals), the acquisition is exempt from charge if the following conditions are met.

(2)The conditions are—

(a)that the individual (whether alone or with other individuals) acquires from the house-building company a new dwelling,

(b)that the individual—

(i)occupied the old dwelling as his only or main residence at some time in the period of two years ending with the date of its acquisition, and

(ii)intends to occupy the new dwelling as his only or main residence,

(c)that each acquisition is entered into in consideration of the other, and

(d)that the area of land acquired by the house-building company does not exceed the permitted area.

(3)Where the conditions in sub-paragraph (2)(a) to (c) are met but the area of land acquired by the house-building company exceeds the permitted area, the chargeable consideration for the acquisition is taken to be the amount calculated by deducting the market value of the permitted area from the market value of the old dwelling.

(4)A “house-building company” means a company that carries on the business of constructing or adapting buildings or parts of buildings for use as dwellings.

References in this paragraph to such a company include any company connected with it.

(5)In this paragraph—

(a)references to the acquisition of the new dwelling are to the acquisition, by way of grant or transfer, of a major interest in the dwelling;

(b)references to the acquisition of the old dwelling are to the acquisition, by way of transfer, of a major interest in the dwelling; and

(c)references to the market value of the old dwelling and of the permitted area are, respectively, to the market value of that major interest in the dwelling and of that interest so far as it relates to that area.

Acquisition by property trader from individual acquiring new dwelling

2(1)Where a dwelling (“the old dwelling”) is acquired by a property trader from an individual (whether alone or with other individuals), the acquisition is exempt from charge if the following conditions are met.

(2)The conditions are—

(a)that the acquisition is made in the course of a business that consists of or includes acquiring dwellings from individuals who acquire new dwellings from house-building companies,

(b)that the individual (whether alone or with other individuals) acquires a new dwelling from a house-building company,

(c)that the individual—

(i)occupied the old dwelling as his only or main residence at some time in the period of two years ending with the date of its acquisition, and

(ii)intends to occupy the new dwelling as his only or main residence,

(d)that the property trader does not intend—

(i)to spend more than the permitted amount on refurbishment of the old dwelling, or

(ii)to grant a lease or licence of the old dwelling, or

(iii)to permit any of its principals or employees (or any person connected with any of its principals or employees) to occupy the old dwelling, and

(e)that the area of land acquired by the property trader does not exceed the permitted area.

Paragraph (d)(ii) does not apply to the grant of lease or licence to the individual for a period of no more than six months.

(3)Where the conditions in sub-paragraph (2)(a) to (d) are met, but the area of land acquired by the property trader exceeds the permitted area, the chargeable consideration for the acquisition is taken to be the amount calculated by deducting the market value of the permitted area from the market value of the old dwelling.

(4)The provisions of paragraph 1(4) (meaning of “house-building company” etc) also have effect for the purposes of this paragraph.

(5)In this paragraph—

(a)references to the acquisition of a new dwelling are to the acquisition, by way of grant or transfer, of a major interest in the dwelling;

(b)references to the acquisition of the old dwelling are to the acquisition, by way of transfer, of a major interest in the dwelling; and

(c)references to the market value of the old dwelling and of the permitted area are, respectively, to the market value of that major interest in the dwelling and of that interest so far as it relates to that area.

Acquisition by property trader from personal representatives

3(1)Where a dwelling is acquired by a property trader from the personal representatives of a deceased individual, the acquisition is exempt from charge if the following conditions are met.

(2)The conditions are—

(a)that the acquisition is made in the course of a business that consists of or includes acquiring dwellings from personal representatives of deceased individuals,

(b)that the deceased individual occupied the dwelling as his only or main residence at some time in the period of two years ending with the date of his death,

(c)that the property trader does not intend—

(i)to spend more than the permitted amount on refurbishment of the dwelling, or

(ii)to grant a lease or licence of the dwelling, or

(iii)to permit any of its principals or employees (or any person connected with any of its principals or employees) to occupy the dwelling, and

(d)that the area of land acquired does not exceed the permitted area.

(3)Where the conditions in sub-paragraph (2)(a) to (c) are met, but the area of land acquired exceeds the permitted area, the chargeable consideration for the acquisition is taken to be the amount calculated by deducting the market value of the permitted area from the market value of the dwelling.

(4)In this paragraph—

(a)references to the acquisition of the dwelling are to the acquisition, by way of transfer, of a major interest in the dwelling; and

(b)references to the market value of the dwelling and of the permitted area are, respectively, to the market value of that major interest in the dwelling and of that interest so far as it relates to that area.

Acquisition by property trader from individual where chain of transactions breaks down

4(1)Where a dwelling (“the old dwelling”) is acquired by a property trader from an individual (whether alone or with other individuals), the acquisition is exempt from charge if—

(a)the individual has made arrangements to sell a dwelling (“the old dwelling”) and acquire another dwelling (“the second dwelling”),

(b)the arrangements to sell the old dwelling fail, and

(c)the acquisition of the old dwelling is made for the purpose of enabling the individual’s acquisition of the second dwelling to proceed,

and the following conditions are met.

(2)The conditions are—

(a)that the acquisition is made in the course of a business that consists of or includes acquiring dwellings from individuals in those circumstances,

(b)that the individual—

(i)occupied the old dwelling as his only or main residence at some time in the period of two years ending with the date of its acquisition, and

(ii)intends to occupy the second dwelling as his only or main residence,

(c)that the property trader does not intend—

(i)to spend more than the permitted amount on refurbishment of the old dwelling, or

(ii)to grant a lease or licence of the old dwelling, or

(iii)to permit any of its principals or employees (or any person connected with any of its principals or employees) to occupy the old dwelling, and

(d)that the area of land acquired does not exceed the permitted area.

Paragraph (c)(ii) does not apply to the grant of a lease or licence to the individual for a period of no more than six months.

(3)Where the conditions in sub-paragraph (2)(a) to (c) are met, but the area of land acquired exceeds the permitted area, the chargeable consideration for the acquisition is taken to be the amount calculated by deducting the market value of the permitted area from the market value of the old dwelling.

(4)In this paragraph—

(a)references to the acquisition of the second dwelling are to the acquisition, by way of grant or transfer, of a major interest in the dwelling;

(b)references to the acquisition of the old dwelling are to the acquisition, by way of transfer, of a major interest in the dwelling; and

(c)references to the market value of the old dwelling and of the permitted area are, respectively, to the market value of that major interest in the dwelling and of that interest so far as it relates to that area.

Acquisition by employer in case of relocation of employment

5(1)Where a dwelling is acquired from an individual (whether alone or with other individuals) by his employer, the acquisition is exempt from charge if the following conditions are met.

(2)The conditions are—

(a)that the individual occupied the dwelling as his only or main residence at some time in the period of two years ending with the date of the acquisition,

(b)that the acquisition is made in connection with a change of residence by the individual resulting from relocation of employment,

(c)that the consideration for the acquisition does not exceed the market value of the dwelling, and

(d)that the area of land acquired does not exceed the permitted area.

(3)Where the conditions in sub-paragraph (2)(a) to (c) are met but the area of land acquired exceeds the permitted area, the chargeable consideration for the acquisition is taken to be the amount calculated by deducting the market value of the permitted area from the market value of the dwelling.

(4)In this paragraph “relocation of employment” means a change of the individual’s place of employment due to—

(a)his becoming an employee of the employer,

(b)an alteration of the duties of his employment with the employer, or

(c)an alteration of the place where he normally performs those duties.

(5)For the purposes of this paragraph a change of residence is one “resulting from” relocation of employment if—

(a)the change is made wholly or mainly to allow the individual to have his residence within a reasonable daily travelling distance of his new place of employment, and

(b)his former residence is not within a reasonable daily travelling distance of that place.

The individual’s “new place of employment” means the place where he normally performs, or is normally to perform, the duties of his employment after the relocation.

(6)In this paragraph—

(a)references to the acquisition of the dwelling are to the acquisition, by way of transfer, of a major interest in the dwelling;

(b)references to the market value of the dwelling and of the permitted area are, respectively, to the market value of that major interest in the dwelling and of that interest so far as it relates to that area; and

(c)references to an individual’s employer include a prospective employer.

Acquisition by property trader in case of relocation of employment

6(1)Where a dwelling is acquired by a property trader from an individual (whether alone or with other individuals), the acquisition is exempt from charge if the following conditions are met.

(2)The conditions are—

(a)that the acquisition is made in the course of a business that consists of or includes acquiring dwellings from individuals in connection with a change of residence resulting from relocation of employment,

(b)that the individual occupied the dwelling as his only or main residence at some time in the period of two years ending with the date of the acquisition,

(c)that the acquisition is made in connection with a change of residence by the individual resulting from relocation of employment,

(d)that the consideration for the acquisition does not exceed the market value of the dwelling,

(e)that the property trader does not intend—

(i)to spend more than the permitted amount on refurbishment of the dwelling, or

(ii)to grant a lease or licence of the dwelling, or

(iii)to permit any of its principals or employees (or any person connected with any of its principals or employees) to occupy the dwelling, and

(f)that the area of land acquired does not exceed the permitted area.

Paragraph (e)(ii) does not apply to the grant of a lease or licence to the individual for a period of no more than six months.

(3)Where the conditions in sub-paragraph (2)(a) to (e) are met but the area of land acquired exceeds the permitted area, the chargeable consideration for the acquisition is taken to be the amount calculated by deducting the market value of the permitted area from the market value of the dwelling.

(4)In this paragraph “relocation of employment” means a change of the individual’s place of employment due to—

(a)his becoming employed by a new employer,

(b)an alteration of the duties of his employment, or

(c)an alteration of the place where he normally performs those duties.

(5)For the purposes of this paragraph a change of residence is one “resulting from” relocation of employment if—

(a)the change is made wholly or mainly to allow the individual to have his residence within a reasonable daily travelling distance of his new place of employment, and

(b)his former residence is not within a reasonable daily travelling distance of that place.

An individual’s “new place of employment” means the place where he normally performs, or is normally to perform, the duties of his employment after the relocation.

(6)In this paragraph—

(a)references to the acquisition of the dwelling are to the acquisition, by way of transfer, of a major interest in the dwelling; and

(b)references to the market value of the dwelling and of the permitted area are, respectively, to the market value of that major interest in the dwelling and of that interest so far as it relates to that area.

Meaning of “dwelling”, “new dwelling” and “the permitted area”

7(1)“Dwelling” includes land occupied and enjoyed with the dwelling as its garden or grounds.

(2)A building or part of a building is a “new dwelling”if—

(a)it has been constructed for use as a single dwelling and has not previously been occupied, or

(b)it has been adapted for use as a single dwelling and has not been occupied since its adaptation.

(3)“The permitted area”, in relation to a dwelling, means land occupied and enjoyed with the dwelling as its garden or grounds that does not exceed—

(a)an area (inclusive of the site of the dwelling) of 0.5 of a hectare, or

(b)such larger area as is required for the reasonable enjoyment of the dwelling as a dwelling having regard to its size and character.

(4)Where sub-paragraph (3)(b) applies, the permitted area is taken to consist of that part of the land that would be the most suitable for occupation and enjoyment with the dwelling as its garden or grounds if the rest of the land were separately occupied.

Meaning of “property trader” and “principal”

8(1)A “property trader” means—

(a)a company,

(b)a limited liability partnership, or

(c)a partnership whose members are all either companies or limited liability partnerships,

that carries on the business of buying and selling dwellings.

(2)In relation to a property trader a “principal” means—

(a)in the case of a company, a director;

(b)in the case of a limited liability partnership, a member;

(c)in the case of a partnership whose members are all either companies or limited liability partnerships, a member or a person who is a principal of a member.

(3)For the purposes of this Schedule—

(a)anything done by or in relation to a company connected with a property trader is treated as done by or in relation to that property trader, and

(b)references to the principals or employees of a property trader include the principals or employees of any such company.

Meaning of “refurbishment” and “the permitted amount”

9(1)“Refurbishment”of a dwelling means the carrying out of works that enhance or are intended to enhance the value of the dwelling, but does not include—

(a)cleaning the dwelling, or

(b)works required solely for the purpose of ensuring that the dwelling meets minimum safety standards.

(2)The “permitted amount”, in relation to the refurbishment of a dwelling, is—

(a)10,000, or

(b)5% of the consideration for the acquisition of the dwelling,

whichever is the greater, but subject to a maximum of £20,000.

Connected companies etc

10Section 839 of the Taxes Act 1988 (connected persons) has effect for the purposes of this Schedule.

Withdrawal of relief under this Schedule

11(1)Relief under this Schedule is withdrawn in the following circumstances.

(2)Relief under paragraph 2 (acquisition by property trader from individual acquiring new dwelling) is withdrawn if the property trader—

(a)spends more than the permitted amount on refurbishment of the old dwelling, or

(b)grants a lease or licence of the old dwelling, or

(c)permits any of its principals or employees (or any person connected with any of its principals or employees) to occupy the old dwelling.

Paragraph (b) does not apply to the grant of lease or licence to the individual for a period of no more than six months.

(3)Relief under paragraph 3 (acquisition by property trader from personal representatives) is withdrawn if the property trader—

(a)spends more than the permitted amount on refurbishment of the dwelling, or

(b)grants a lease or licence of the dwelling, or

(c)permits any of its principals or employees (or any person connected with any of its principals or employees) to occupy the dwelling.

(4)Relief under paragraph 4 (acquisition by property trader from individual where chain of transactions breaks down) is withdrawn if the property trader—

(a)spends more than the permitted amount on refurbishment of the old dwelling, or

(b)grants a lease or licence of the old dwelling, or

(c)permits any of its principals or employees (or any person connected with any of its principals or employees) to occupy the old dwelling.

Paragraph (b) does not apply to the grant of lease or licence to the individual for a period of no more than six months.

(5)Relief under paragraph 6 (acquisition by property trader in case of relocation of employment) is withdrawn if the property trader—

(a)spends more than the permitted amount on refurbishment of the dwelling, or

(b)grants a lease or licence of the dwelling, or

(c)permits any of its principals or employees (or any person connected with any of its principals or employees) to occupy the dwelling.

Paragraph (b) does not apply to the grant of lease or licence to the individual for a period of no more than six months.

(6)Where relief is withdrawn the amount of tax chargeable is the amount that would have been chargeable in respect of the acquisition but for the relief.”.

(3)In section 81 (further return where relief withdrawn)—

(a)in subsection (1) (obligation to deliver a further return), before paragraph (a) insert—

“(za)paragraph 11 of Schedule 6A (relief for certain acquisitions of residential property),”; and

(b)in subsection (4) (meaning of disqualifying event), before paragraph (a) insert—

“(za)in relation to the withdrawal of relief under Schedule 6A, an event mentioned in paragraph (a), (b) or (c) of paragraph 11(2), (3), (4) or (5) of that Schedule;”.

(4)In section 87 (interest on unpaid tax)—

(a)in subsection (3)(a) (relevant date where relief is withdrawn), before sub-paragraph (i) insert—

“(ia)Schedule 6A (relief for certain acquisitions of residential property),”; and

(b)in subsection (4) (meaning of disqualifying event), before paragraph (a) insert—

“(za)in relation to the withdrawal of relief under Schedule 6A an event mentioned in paragraph (a), (b) or (c) of paragraph 11(2), (3), (4) or (5) of that Schedule;”.

Initial transfer of assets to trustees of unit trust schemeU.K.

F118U.K.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Textual Amendments

F1Sch. 39 para. 18 repealed (with effect in accordance with Sch. 26 Pt. 7(3) Note of the amending Act) by Finance Act 2006 (c. 25), Sch. 26 Pt. 7(3)

Return or further return in consequence of later linked transactionU.K.

19(1)After section 81 (further return where relief withdrawn) insert—U.K.

“81AReturn or further return in consequence of later linked transaction

(1)Where the effect of a transaction (“the later transaction”) that is linked to an earlier transaction is that the earlier transaction becomes notifiable, or that additional tax is payable in respect of the earlier transaction or that tax is payable in respect of the earlier transaction where none was payable before—

(a)the purchaser under the earlier transaction must deliver a return or further return in respect of that transaction before the end of the period of 30 days after the effective date of the later transaction,

(b)the return must include a self-assessment of the amount of tax chargeable as a result of the later transaction,

(c)the tax so chargeable is to be calculated by reference to the rates in force at the effective date of the earlier transaction, and

(d)the return must be accompanied by payment of the tax or additional tax payable.

(2)The provisions of Schedule 10 (returns, enquiries, assessments and other matters) apply to a return under this section as they apply to a return under section 76 (general requirement to deliver land transaction return), with the following adaptations—

(a)in paragraph 5 (formal notice to deliver return), the requirement in sub-paragraph (2)(a) that the notice specify the transaction to which it relates shall be read as requiring both the earlier and later transactions to be specified;

(b)references to the effective date of the transaction to which the return relates shall be read as references to the effective date of the later transaction.

(3)This section does not affect any requirement to make a return under section 76 in respect of the later transaction.”.

(2)In section 81(3) for “land transaction return” substitute “ return under section 76 (general requirement to deliver land transaction return) ”.

(3)In section 87 (interest on unpaid tax), in subsection (3) (meaning of “the relevant date”), after paragraph (a) insert—

“(aa)in the case of an amount payable under section 81A in respect of an earlier transaction because of the effect of a later linked transaction, the effective date of the later transaction;”.

Declaration by person authorised to act on behalf of purchaserU.K.

20U.K.After section 81A (inserted by paragraph 19 above) insert—

“81BDeclaration by person authorised to act on behalf of individual

(1)This section applies to the declaration mentioned in paragraph 1(1)(c) of Schedule 10 or paragraph 2(1)(c) of Schedule 11 (declaration that return or self-certificate is correct and complete).

(2)The requirement that an individual make such a declaration (alone or jointly with others) is treated as met if a declaration to that effect is made by a person authorised to act on behalf of that individual in relation to the matters to which the return or certificate relates.

(3)For the purposes of this section a person is not regarded as authorised to act on behalf of an individual unless he is so authorised by a power of attorney in writing, signed by that individual.

In this subsection as it applies in Scotland “power of attorney” includes factory and commission.

(4)Nothing in this section affects the making of a declaration in accordance with—

(a)section 100(2) (persons through whom a company acts), or

(b)section 106 (1) or (2) (person authorised to act on behalf of incapacitated person or minor).”.

Crown applicationU.K.

21(1)Section 107 (Crown application) is amended as follows.U.K.

(2)For subsection (1) (extent of Crown application) substitute—

“(1)This Part binds the Crown, subject to the following provisions of this section.”.

(3)After subsection (3) add—

“(4)Nothing in this section shall be read as making the Crown liable to prosecution for an offence.”.

Further provision relating to leasesU.K.

22(1)For section 120 (meaning of “lease” and other supplementary provisions) substitute—U.K.

“120Further provisions relating to leases

Schedule 17A contains further provisions relating to leases.”.

(2)After Schedule 17 insert—

Section 120

“SCHEDULE 17AU.K.

Further provisions relating to leasesU.K.

Meaning of “lease”

1In the application of this Part to England and Wales or Northern Ireland “lease” means—

(a)an interest or right in or over land for a term of years (whether fixed or periodic), or

(b)a tenancy at will or other interest or right in or over land terminable by notice at any time.

Leases for a fixed term

2In the application of the provisions of this Part to a lease for a fixed term, no account shall be taken of—

(a)any contingency as a result of which the lease may determine before the end of the fixed term, or

(b)any right of either party to determine the lease or renew it.

Leases that continue after a fixed term

3(1)This paragraph applies to—

(a)a lease for a fixed term and thereafter until determined, or

(b)a lease for a fixed term that may continue beyond the fixed term by operation of law.

(2)For the purposes of this Part (except section 77 (notifiable transactions)), a lease to which this paragraph applies is treated—

(a)in the first instance as if it were a lease for the original fixed term and no longer,

(b)if the lease continues after the end of that term, as if it were a lease for a fixed term one year longer than the original fixed term,

(c)if the lease continues after the end of the term resulting from the application of paragraph (b), as if it were a lease for a fixed term two years longer than the original fixed term,

and so on.

(3)Where the effect of sub-paragraph (2) in relation to the continuation of the lease after the end of a fixed term is that additional tax is payable in respect of a transaction or that tax is payable in respect of a transaction where none was payable before—

(a)the purchaser must deliver a return or further return in respect of that transaction before the end of the period of 30 days after the end of that term,

(b)the return must include a self-assessment of the amount of tax chargeable in respect of the transaction on the basis of the information contained in the return,

(c)the tax so chargeable is to be calculated by reference to the rates in force at the effective date of the transaction, and

(d)the return must be accompanied by payment of the tax or additional tax payable.

(4)The provisions of Schedule 10 (returns, enquiries, assessments and other matters) apply to a return under this paragraph as they apply to a return under section 76 (general requirement to deliver land transaction return), with the adaptation that references to the effective date of the transaction shall be read as references to the day on which the lease becomes treated as being for a longer fixed term.

(5)For the purposes of section 77 (notifiable transactions) a lease to which this paragraph applies is a lease for whatever is its fixed term.

Treatment of leases for indefinite term

4(1)For the purposes of this Part (except section 77 (notifiable transactions))—

(a)a lease for an indefinite term is treated in the first instance as if it were a lease for a fixed term of a year,

(b)if the lease continues after the end of the term resulting from the application of paragraph (a), it is treated as if it were a lease for a fixed term of two years,

(c)if the lease continues after the end of the term resulting from the application of paragraph (b), it is treated as if it were a lease for a fixed term of three years,

and so on.

(2)No account shall be taken for the purposes of this Part of any other statutory provision in England and Wales or Northern Ireland deeming a lease for an indefinite period to be a lease for a different term.

(3)Where the effect of sub-paragraph (1) in relation to the continuation of the lease after the end of a deemed fixed term is that additional tax is payable in respect of a transaction or that tax is payable in respect of a transaction where none was payable before—

(a)the purchaser must deliver a return or further return in respect of that transaction before the end of the period of 30 days after the end of that term,

(b)the return must include a self-assessment of the amount of tax chargeable in respect of the transaction on the basis of the information contained in the return,

(c)the tax so chargeable is to be calculated by reference to the rates in force at the effective date of the transaction, and

(d)the return must be accompanied by payment of the tax or additional tax payable.

(4)The provisions of Schedule 10 (returns, enquiries, assessments and other matters) apply to a return under this paragraph as they apply to a return under section 76 (general requirement to deliver land transaction return), with the adaptation that references to the effective date of the transaction shall be read as references to the day on which the lease becomes treated as being for a longer fixed term.

(4A)For the purposes of section 77 (notifiable transactions) a lease for an indefinite term is a lease for a term of less then seven years.

(5)References in this paragraph to a lease for an indefinite period include—

(a)a periodic tenancy or other interest or right terminable by a period of notice,

(b)a tenancy at will in England and Wales or Northern Ireland, or

(c)any other interest or right terminable by notice at any time.

Treatment of successive linked leases

5(1)This paragraph applies where—

(a)successive leases are granted or treated as granted (whether at the same time or at different times) of the same or substantially the same premises, and

(b)those grants are linked transactions.

(2)This Part applies as if the series of leases were a single lease—

(a)granted at the time of the grant of the first lease in the series,

(b)for a term equal to the aggregate of the terms of all the leases, and

(c)in consideration of the rent payable under all of the leases.

(3)The grant of later leases in the series is accordingly disregarded for the purposes of this Part except section 81A (return or further return in consequence of later linked transaction).

Rent

6(1)For the purposes of this Part a single sum expressed to be payable in respect of rent, or expressed to be payable in respect of rent and other matters but not apportioned, shall be treated as entirely rent.

(2)Sub-paragraph (1) is without prejudice to the application of paragraph 4 of Schedule 4 (chargeable consideration: just and reasonable apportionment) where separate sums are expressed to be payable in respect of rent and other matters.

Variable or uncertain rent

7(1)This paragraph applies to determine the amount of rent payable under a lease where that amount—

(a)varies in accordance with provision in the lease, or

(b)is contingent, uncertain or unascertained.

(2)As regards rent payable in respect of any period before the end of the fifth year of the term of the lease—

(a)the provisions of this Part apply as in relation to other chargeable consideration, and

(b)the provisions of section 51 (1) and (2) accordingly apply if the amount is contingent, uncertain or unascertained.

(3)As regards rent payable in respect of any period after the end of the fifth year of the term of the lease, the annual amount is assumed for the purposes of this Part to be, in every case, equal to the highest amount of rent payable in respect of any consecutive twelve month period in the first five years of the term.

In determining that amount take into account (if necessary) any amounts determined as mentioned in sub-paragraph (2)(b), but disregard paragraph 9(2) (deemed reduction of rent for overlap period in case of grant of further lease).

(4)This paragraph has effect subject to paragraph 8 (adjustment where rent payable ceases to be uncertain).

(5)No account shall be taken for the purposes of this Part of any provision for rent to be adjusted in line with the retail prices index.

First rent review in final quarter of fifth yearU.K.

7AWhere—

(a)a lease contains provision under which the rent may be adjusted,

(b)under that provision the first (or only) such adjustment—

(i)is to an amount that (before the adjustment) is uncertain, and

(ii)has effect from a date (the “review date”) that is expressed as falling five years after a specified date,

and

(c)the specified date falls within the three months before the beginning of the term of the lease,

this Schedule has effect as if references to the first five years of the term of the lease were to the period beginning with the start of the term of the lease and ending with the review date. References to the fifth year of the term of the lease shall be read accordingly.

Adjustment where rent ceases to be uncertainU.K.

8(1)Where the provisions of section 51 (1) and (2) (contingent, uncertain or unascertained consideration) apply in relation to a transaction by virtue of paragraph 7 (uncertain rent) and—

(a)the end of the fifth year of the term of the lease is reached, or

(b)the amount of rent payable in respect of the first five years of the term of the lease ceases to be uncertain at an earlier date,

the following provisions have effect to require or permit reconsideration of how this Part applies to the transaction (and to any transaction in relation to which it is a linked transaction).

(2)For the purposes of this paragraph the amount of rent payable ceases to be uncertain when—

(a)in the case of contingent rent, the contingency occurs or it becomes clear that it will not occur, and

(b)in the case of uncertain or unascertained rent, the amount becomes ascertained.

(3)If the result as regards the rent paid or payable in respect of the first five years of the term of the lease is that a transaction becomes notifiable, or that additional tax is payable in respect of a transaction or that tax is payable where none was payable before—

(a)the purchaser must make a return to the Inland Revenue within 30 days of the date referred to in sub-paragraph (1)(a) or (b),

(b)the return must contain a self-assessment of the tax chargeable in respect of the transaction on the basis of the information contained in the return,

(c)the tax so chargeable is to be calculated by reference to the rates in force at the effective date of the transaction, and

(d)the return must be accompanied by payment of any tax or additional tax payable.

(4)The provisions of Schedule 10 (returns, enquiries, assessment and other matters) apply to a return under this paragraph as they apply to a return under section 76 (general requirement to make land transaction return), subject to the adaptation that references to the effective date of the transaction shall be read as references to the date referred to in sub-paragraph (1)(a) or (b).

(5)If the result as regards the rent paid or payable in respect of the first five years of the term of the lease is that less tax is payable in respect of the transaction than has already been paid—

(a)the purchaser may, within the period allowed for amendment of the land transaction return, amend the return accordingly;

(b)after the end of that period he may (if the land transaction return is not so amended) make a claim to the Inland Revenue for repayment of the amount overpaid.

Rent for overlap period in case of grant of further leaseU.K.

9(1)This paragraph applies where—

(a)A surrenders an existing lease to B (“the old lease”) and in consideration of that surrender B grants a lease to A of the same or substantially the same premises (“the new lease”),

(b)the tenant under a lease (“the old lease”) of premises to which Part 2 of the Landlord and Tenant Act 1954 or the Business Tenancies (Northern Ireland) Order 1996 applies makes a request for a new tenancy (“the new lease”) which is duly executed,

(c)on termination of a lease (“the head lease”) a sub-tenant is granted a lease (“the new lease”) of the same or substantially the same premises as those comprised in his original lease (“the old lease”)—

(i)in pursuance of an order of a court on a claim for relief against re-entry or forfeiture, or

(ii)in pursuance of a contractual entitlement arising in the event of the head lease being terminated,

or

(d)a person who has guaranteed the obligations of a lessee under a lease that has been terminated (“the old lease”) is granted a lease of the same or substantially the same premises (“the new lease”) in pursuance of the guarantee.

(2)For the purposes of this Part the rent payable under the new lease in respect of any period falling within the overlap period is treated as reduced by the amount of the rent that would have been payable in respect of that period under the old lease.

(3)The overlap period is the period between the date of grant of the new lease and what would have been the end of the term of the old lease had it not been terminated.

(4)The rent that would have been payable under the old lease shall be taken to be the amount taken into account in determining the stamp duty land tax chargeable in respect of the acquisition of the old lease.

(5)This paragraph does not have effect so as to require the rent payable under the new lease to be treated as a negative amount.

Tenants' obligations etc that do not count as chargeable considerationU.K.

10(1)In the case of the grant of a lease none of the following counts as chargeable consideration—

(a)any undertaking by the tenant to repair, maintain or insure the demised premises (in Scotland, the leased premises);

(b)any undertaking by the tenant to pay any amount in respect of services, repairs, maintenance or insurance or the landlord’s costs of management;

(c)any other obligation undertaken by the tenant that is not such as to affect the rent that a tenant would be prepared to pay in the open market;

(d)any guarantee of the payment of rent or the performance of any other obligation of the tenant under the lease;

(e)any penal rent, or increased rent in the nature of a penal rent, payable in respect of the breach of any obligation of the tenant under the lease.

(2)Where sub-paragraph (1) applies in relation to an obligation, a payment made in discharge of the obligation does not count as chargeable consideration.

(3)The release of any such obligation as is mentioned in sub-paragraph (1) does not count as chargeable consideration in relation to the surrender of the lease.

Cases where assignment of lease treated as grant of leaseU.K.

11(1)This paragraph applies where—

(a)the grant of a lease is exempt from charge by virtue of any of the provisions specified in sub-paragraph (3), or

(b)a lease is granted to a person as bare trustee of the grantor, with the result that the lease is treated as vested in the grantor by virtue of paragraph 3 of Schedule 16.

(2)The first assignment of the lease that is not exempt from charge by virtue of any of the provisions specified in sub-paragraph (3), and in relation to which the assignee does not acquire the lease as a bare trustee of the assignor, is treated for the purposes of this Part as if it were the grant of a lease by the assignor—

(a)for a term equal to the unexpired term of the lease referred to in sub-paragraph (1), and

(b)on the same terms as those on which the assignee holds that lease after the assignment.

(3)The provisions are—

(a)section 57A (sale and leaseback arrangements);

(b)Part 1 or 2 of Schedule 7 (group relief or reconstruction or acquisition relief);

(c)section 66 (transfers involving public bodies);

(d)Schedule 8 (charities relief);

(e)any such regulations as are mentioned in section 123(3) (regulations reproducing in relation to stamp duty land tax the effect of enactments providing for exemption from stamp duty).

(4)This paragraph does not apply where the relief in question is group relief, reconstruction or acquisition relief or charities relief and is withdrawn as a result of a disqualifying event occurring before the effective date of the assignment.

(5)For the purposes of sub-paragraph (4) “disqualifying event” means—

(a)in relation to the withdrawal of group relief, the purchaser ceasing to be a member of the same group as the vendor (within the meaning of Part 1 of Schedule 7);

(b)in relation to the withdrawal of reconstruction or acquisition relief, the change of control of the acquiring company mentioned in paragraph 9(1)(a) of that Schedule or, as the case may be, the event mentioned in paragraph 11(1)(a) or (2)(a) of that Schedule;

(c)in relation to the withdrawal of charities relief, a disqualifying event as defined in paragraphs 2(3) or 3(2) of Schedule 8.

Assignment of lease: responsibility of assignee for returns etcU.K.

12(1)Where a lease is assigned, anything that but for the assignment would be required or authorised to be done by or in relation to the assignor under or by virtue of—

(a)section 80 (adjustment where contingency ceases or consideration is ascertained),

(b)section 81A (return or further return in consequence of later linked transaction),

(c)paragraph 3 or 4 of this Schedule (return or further return required where lease for indefinite period continues), or

(d)paragraph 8 of this Schedule (adjustment where rent ceases to be uncertain),

shall, if the event giving rise to the adjustment or return occurs after the effective date of the assignment, be done instead by or in relation to the assignee.

(2)So far as necessary for giving effect to sub-paragraph (1) anything previously done by or in relation to the assignor shall be treated as if it had been done by or in relation to the assignee.

(3)This paragraph does not apply if the assignment falls to be treated as the grant of a lease by the assignor (see paragraph 11).

Agreement for leaseU.K.

12A(1)This paragraph applies where in England and Wales or Northern Ireland—

(a)an agreement for a lease is entered into, and

(b)the agreement is substantially performed without having been completed.

(2)The agreement is treated as if it were the grant of a lease in accordance with the agreement (“the notional lease”), beginning with the date of substantial performance.

The effective date of the transaction is that date.

(3)Where a lease is subsequently granted in pursuance of the agreement—

(a)the notional lease is treated as if it were surrendered at that time, and

(b)the lease itself is treated for the purposes of paragraph 9 (rent for overlap period in case of grant of further lease) as if it were granted in consideration of that surrender.

(4)Where sub-paragraph (1) applies and the agreement is (to any extent) afterwards rescinded or annulled, or is for any other reason not carried into effect, the tax paid by virtue of that sub-paragraph shall (to that extent) be repaid by the Inland Revenue.

Repayment must be claimed by amendment of the land transaction return made in respect of the agreement.

(5)In this paragraph “substantially performed” and “completed” have the same meanings as in section 44 (contract and conveyance).

Assignment of agreement for leaseU.K.

12B(1)This paragraph applies, in place of section 45 (contract and conveyance: effect of transfer of rights), where in England and Wales or Northern Ireland a person assigns his interest as lessee under an agreement for a lease.

(2)If the assignment occurs without the agreement having been substantially performed, section 44 (contract and conveyance) has effect as if—

(a)the contract were with the assignee and not the assignor, and

(b)the consideration given by the assignee for entering into the contract included any consideration given by him for the assignment.

(3)If the assignment occurs after the agreement has been substantially performed—

(a)the assignment is a separate land transaction, and

(b)the effective date of that transaction is the date of the assignment.

(4)Where there are successive assignments, this paragraph has effect in relation to each of them.

Increase of rent treated as grant of new lease: variation of leaseU.K.

13(1)Where a lease is varied so as to increase the amount of the rent, the variation is treated for the purposes of this Part as if it were the grant of a lease in consideration of the additional rent made payable by it.

(2)Sub-paragraph (1) does not apply to an increase of rent in pursuance of a provision contained in the lease (but see paragraph 14).

Increase of rent treated as grant of new lease: abnormal increase after fifth yearU.K.

14(1)This paragraph applies if, after the end of the fifth year of the term of a lease—

(a)the amount of rent payable increases (or is increased) in accordance with the provisions of the lease, and

(b)the rent payable as a result (“the new rent”) is such that the increase falls to be regarded as abnormal (see paragraph 15).

(2)The increase in rent is treated as if it were the grant of a lease in consideration of the excess rent.

(3)The excess rent is the difference between the new rent and the rent previously taxed.

(4)The rent previously taxed is—

(a)where the provisions of this paragraph have not previously applied to a rent increase under the lease, the rent that is assumed to be payable after the fifth year of the term of the lease (in accordance with paragraph 7(3));

(b)where the provisions of this paragraph have previously so applied, the rent payable as a result of the last increase in relation to which the provisions of this paragraph applied.

(5)The deemed grant is treated as—

(a)made on the date on which the increased rent first became payable, and

(b)for a term equal to the unexpired part of the original lease,

and as linked with the grant of the original lease (and with any other transaction with which that transaction is linked).

(6)The assumption in paragraph 7(3) (that the rent does not change after the end of the fifth year of the term of a lease) does not apply for the purposes of this paragraph or paragraph 15 except for the purpose of determining the rent previously taxed.

Increase of rent after fifth year: whether regarded as abnormalU.K.

15Whether an increase in rent is to be regarded for the purposes of paragraph 14 as abnormal is determined as follows:— Step One

Find the start date, which is—

(a)where the provisions of that paragraph have not previously applied to a rent increase under the lease, the beginning of the period by reference to which the rent assumed to be payable after the fifth year of the term of the lease is determined in accordance with paragraph 7(3);

(b)where the provisions of that paragraph have previously so applied, the date of the last increase in relation to which the provisions of that paragraph applied.

Step Two

Divide the period between the start date and the date on which the new rent first becomes payable (“the reference period”) into—

(a)successive periods of twelve months running from the start date (if any), and

(b)any remaining period which does not fall within paragraph (a).

Step Three

Find the factor by which the retail prices index has increased over each period identified in step two.

This is a figure expressed as a decimal and determined by the formula—

where—

RD is the retail prices index for the month in which the last day of the period in question falls, and

RI is the retail prices index for the month in which the first day of the period in question falls.

If, in relation to any period, RD is equal to or less than RI, the factor by which the retail prices index has increased over the period in question shall be treated as nil.

If, in relation to any period, the figure determined in accordance with the formula would be a figure having more than 3 decimal places, round it to the nearest third decimal place.

Step Four

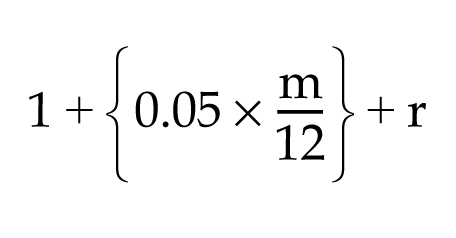

Find the relevant factor for each period identified in step two.

This is a figure expressed as a decimal and determined by the formula—

where—

m is the number of months in the period in question (treating part of a month as a whole month), and

r is the factor by which the retail prices index has increased over the period in question, determined under step three.

If, in relation to any period, the figure determined in accordance with the formula would have more than 3 decimal places, round it to the nearest third decimal place.

Step Five

Find the uplift factor for the reference period as follows.

If there is only one period identified in step two, the uplift factor for the reference period is the relevant factor for that period.

If there are only two periods identified in step two, the uplift factor for the reference period is calculated by multiplying the relevant factors for those periods.

If there are more than two periods identified in step two, the uplift factor for the reference period is calculated by—

(a)multiplying the relevant factors for the first two periods,

(b)multiplying the result by the relevant factor for the next period,

(c)if there are further periods, multiplying the result by the relevant factor for the next period,

until all periods have been taken into account.

If the uplift factor for the reference period would be a figure having more than 3 decimal places, round it to the nearest third decimal place.

Step Six

The rent increase is regarded as abnormal if the new rent is greater than:

where—

R is the rent previously taxed (see paragraph 14(4)), and

UF is the uplift factor for the reference period.

Reduction of rent or termU.K.

15A(1)Where a lease is varied so as to reduce the amount of the rent, the variation is treated for the purposes of this Part as an acquisition of a chargeable interest by the lessee.

(2)Where a lease is varied so as to reduce the term, the variation is treated for the purposes of this Part as an acquisition of a chargeable interest by the lessor.

Surrender of existing lease in return for new leaseU.K.

16Where a lease is granted in consideration of the surrender of an existing lease between the same parties—

(a)the grant of the new lease does not count as chargeable consideration for the surrender, and

(b)the surrender does not count as chargeable consideration for the grant of the new lease.

Paragraph 5 (exchanges) of Schedule 4 (chargeable consideration) does not apply in such a case.

Assignment of lease: assumption of obligations by assigneeU.K.

17In the case of an assignment of a lease the assumption by the assignee of the obligation—

(a)to pay rent, or

(b)to perform or observe any other undertaking of the tenant under the lease,

does not count as chargeable consideration for the assignment.

Reverse premiumU.K.

18(1)In the case of the grant, assignment or surrender of a lease a reverse premium does not count as chargeable consideration.

(2)A “reverse premium” means—

(a)in relation to the grant of a lease, a premium moving from the landlord to the tenant;

(b)in relation to the assignment of a lease, a premium moving from the assignor to the assignee;

(c)in relation to the surrender of a lease, a premium moving from the tenant to the landlord.

Provisions relating to leases in ScotlandU.K.

19(1)In the application of this Part to Scotland—

(a)any reference to the term of a lease is to the period of the lease, and

(b)any reference to the reversion on a lease is to the interest of the landlord in the property subject to the lease.

(2)Where in Scotland there is a lease constituted by concluded missives of let (“the first lease”) and at some later time a lease is executed (“the second lease”)—

(a)the first lease is treated as if it were surrendered at that time, and

(b)the second lease is treated for the purposes of paragraph 9 (rent for overlap period in case of grant of further lease) as if it were granted in consideration of that surrender.

(3)Where in Scotland—

(a)there is an agreement (including missives of let not constituting a lease) under which a lease is to be executed, and

(b)the agreement is substantially performed without a lease having been executed,

the agreement is treated as if it were the grant of a lease in accordance with the agreement (“the notional lease”), beginning with the date of substantial performance.

The effective date of the transaction is when the agreement is substantially performed.

(4)Where sub-paragraph (3) applies and at some later time a lease is executed—

(a)the notional lease is treated as if it were surrendered at that time, and

(b)the lease itself is treated for the purposes of paragraph 9 as if it were granted in consideration of that surrender.

(5)References in sub-paragraphs (2) to (4) to the execution of a lease are to the execution of a lease that either is in conformity with, or relates to substantially the same property and period as, the missives of let or other agreement.

(6)Where sub-paragraph (3) applies and the agreement is (to any extent) afterwards rescinded or annulled, or is for any other reason not carried into effect, the tax paid by virtue of that sub-paragraph shall (to that extent) be repaid by the Inland Revenue.

Repayment must be claimed by amendment of the land transaction return made in respect of the agreement.”.

(3)In section 51 (contingent, uncertain or unascertained consideration), after subsection (4) add—

“(5)This section applies in relation to chargeable consideration consisting of rent only to the extent that it is applied by paragraph 7 of Schedule 17A.”.

(4)In section 80 (adjustment where contingency ceases or consideration becomes certain)—

(a)in subsection (3) for “land transaction return” substitute “ return under section 76 (general requirement to make land transaction return), subject to the adaptation that references to the effective date of the transaction shall be read as references to the date of the event as a result of which the return is required ”; and

(b)after subsection (4) add—

“(5)This section does not apply so far as the consideration consists of rent (see paragraph 8 of Schedule 17A).”.

(5)In section 87 (interest on unpaid tax), in subsection (3) (meaning of “the relevant date”), after paragraph (aa) (inserted by paragraph 19(3) above) insert—

“(ab)in the case of an amount payable under paragraph 3(3) or 4(3) of Schedule 17A (leases that continue after a fixed term and treatment of leases for an indefinite term), the day on which the lease becomes treated as being for a longer fixed term;”.

(6)In section 90 (application to defer payment in case of contingent or uncertain consideration), after subsection (6) add—

“(7)This section does not apply so far as the consideration consists of rent.”.

(7)In the table in section 122 (index of defined expressions), in the second column of the entry for “lease and related expressions” for “section 120” substitute “ Schedule 17A ”.

(8)In paragraph 7 of Schedule 19 (commencement and transitional provisions: earlier related transactions under stamp duty), after sub-paragraph (3) add—

“(4)For the purposes of paragraph 5 of Schedule 17A (treatment of successive linked leases) no account shall be taken of any transaction that is not an SDLT transaction.”.

Abolition of stamp duty: application to duplicates and counterpartsU.K.

23U.K.In section 125(5) (abolition of stamp duty except on instruments relating to stock or marketable securities: instruments to which the section applies)—

(a)in paragraph (a), after “instrument effecting a land transaction”,

(b)in paragraph (b), after “instrument effecting a transaction other than a land transaction”, and

(c)in the second sentence, after “instrument effecting both a land transaction and a transaction other than a land transaction”, insert “ (or any duplicate or counterpart of such an instrument) ”.

Application of transitional provisions to certain contractsU.K.

24U.K.In Schedule 19 (commencement and transitional provisions), after paragraph 4 (contracts entered into before the implementation date) insert—

“Contracts substantially performed after implementation dateU.K.

4AWhere—

(a)a transaction is effected in pursuance of a contract entered into before the first relevant date,

(b)the contract is substantially performed, without having been completed, after the implementation date, and

(c)there is subsequently an event within paragraph 3(3) by virtue of which the transaction is an SDLT transaction,

the effective date of the transaction shall be taken to be the date of the event referred to in paragraph (c) (and not the date of substantial performance).

Application of provisions in case of transfer of rightsU.K.

4B(1)This paragraph applies where section 44 (contract and conveyance) has effect in accordance with section 45 (effect of transfer of rights).

(2)Any reference in paragraph 3, 4 or 4A to the date when a contract was entered into (or made) shall be read, in relation to a contract deemed to exist by virtue of section 45(3) (deemed secondary contract with transferee), as a reference to the date of the assignment, subsale or other transaction in question.”.

Stamping of contract or agreement where transaction on completion or grant of lease subject to stamp duty land taxU.K.

25(1)In Schedule 19 (commencement and transitional provisions), after paragraph 7 (earlier related transactions under stamp duty) insert—U.K.

“Stamping of contract where transaction on completion subject to stamp duty land taxU.K.

7A(1)This paragraph applies where—

(a)a contract that apart from paragraph 7 of Schedule 13 to the Finance Act 1999 (contracts chargeable as conveyances on sale) would not be chargeable with stamp duty is entered into before the implementation date,

(b)a conveyance made in conformity with the contract is effected on or after the implementation date, and

(c)the transaction effected on completion is an SDLT transaction or would be but for an exemption or relief from stamp duty land tax.

(2)If in those circumstances the contract is presented for stamping together with a Revenue certificate as to compliance with the provisions of this Part of this Act in relation to the transaction effected on completion—

(a)the payment of stamp duty land tax on that transaction or, as the case may be, the fact that no such tax was payable shall be denoted on the contract by a particular stamp, and

(b)the contract shall be deemed thereupon to be duly stamped.

(3)In this paragraph “conveyance” includes any instrument.”.

(2)In paragraph 8 of Schedule 19 (time for stamping agreement for lease: lease subject to stamp duty land tax)—

(a)for the heading substitute “ Stamping of agreement for lease where grant of lease subject to stamp duty land tax ”, and

(b)in sub-paragraph (1) for the opening words substitute “ This paragraph applies where— ”.

(3)For sub-paragraph (2) of that paragraph substitute—

“(2)If in those circumstances the agreement is presented for stamping together with a Revenue certificate as to compliance with the provisions of this Part of this Act in relation to the grant of the lease—

(a)the payment of stamp duty land tax in respect of the grant of the lease or, as the case may be, the fact that no such tax was payable shall be denoted on the agreement by a particular stamp, and

(b)the agreement shall be deemed thereupon to be duly stamped.”.

(4)In section 122 (index of defined expressions), at the appropriate place insert—

| “Revenue certificate | section 79(3)(a)”. |

CommencementU.K.

26U.K.This Part of this Schedule applies in relation to any transaction of which the effective date (within the meaning of Part 4 of the Finance Act 2003 (c. 14)) is on or after the day on which this Act is passed.