Apportionment of housing costsE+W+S

7.—(1) Where the dwelling occupied as the home is a composite hereditament and—

(a)before 1st April 1990 for the purposes of section 48(5) of the General Rate Act 1967 F1 (reduction of rates on dwellings), it appeared to a rating authority or it was determined in pursuance of subsection (6) of section 48 of that Act that the hereditament, including the dwelling occupied as the home, was a mixed hereditament and that only a proportion of the rateable value of the hereditament was attributable to use for the purpose of a private dwelling; or

(b)in Scotland, before 1st April 1989 an assessor acting pursuant to section 45(1) of the Water (Scotland) Act 1980 F2 (provision as to valuation roll) has apportioned the net annual value of the premises including the dwelling occupied as the home between the part occupied as a dwelling and the remainder,

the amounts applicable under this Schedule are to be such proportion of the amounts applicable in respect of the hereditament or premises as a whole as is equal to the proportion of the rateable value of the hereditament attributable to the part of the hereditament used for the purposes of a private tenancy or, in Scotland, the proportion of the net annual value of the premises apportioned to the part occupied as a dwelling house.

(2) Subject to sub-paragraph (1) and the following provisions of this paragraph, where the dwelling occupied as the home is a composite hereditament, the amount applicable under this Schedule is to be the relevant fraction of the amount which would otherwise be applicable under this Schedule in respect of the dwelling occupied as the home.

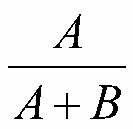

(3) For the purposes of sub-paragraph (2), the relevant fraction is to be obtained in accordance with the formula—

where—

A is the current market value of the claimant's interest in that part of the composite hereditament which is domestic property within the meaning of section 66 of the Act of 1988;

B is the current market value of the claimant's interest in that part of the composite hereditament which is not domestic property within that section.

(4) In this paragraph—

“composite hereditament” means—

as respects England and Wales, any hereditament which is shown as a composite hereditament in a local non-domestic rating list;

as respects Scotland, any lands and heritages entered in the valuation roll which are part residential subjects within the meaning of section 26(1) of the Act of 1987;

“local non-domestic rating list” means a list compiled and maintained under section 41(1) of the Act of 1988;

“the Act of 1987” means the Abolition of Domestic Rates Etc. (Scotland) Act 1987 F3;

“the Act of 1988” means the Local Government Finance Act 1988 F4.

(5) Where responsibility for expenditure which relates to housing costs met under this Schedule is shared, the amounts applicable are to be calculated by reference to the appropriate proportion of that expenditure for which the claimant is responsible.

Textual Amendments

F41988 c. 41. Section 41(1) was amended by the Local Government Finance Act 1992 (c. 14), Schedule 13, paragraph 59.

Modifications etc. (not altering text)

C1Sch. 6 para. 7(3) sum maintained (coming into force in accordance with art. 1(2)(j) of the amending S.I.) by The Social Security Benefits Up-rating Order 2015 (S.I. 2015/457), arts. 1(2)(j), 22(1)(5), Sch. 15