- Y Diweddaraf sydd Ar Gael (Diwygiedig)

- Pwynt Penodol mewn Amser (10/12/2020)

- Gwreiddiol (Fel y’i mabwysiadwyd gan yr UE)

Commission Regulation (EU) No 1388/2014Dangos y teitl llawn

Commission Regulation (EU) No 1388/2014 of 16 December 2014 declaring certain categories of aid to undertakings active in the production, processing and marketing of fishery and aquaculture products compatible with the internal market in application of Articles 107 and 108 of the Treaty on the Functioning of the European Union

You are here:

- Rheoliadau yn deillio o’r UE

- 2014 No. 1388

- Whole Regulation

- Blaenorol

- Nesaf

Pa Fersiwn

Nodweddion Uwch

- Dangos Graddfa Ddaearyddol(e.e. Lloegr, Cymru, Yr Alban aca Gogledd Iwerddon)

- Dangos Llinell Amser Newidiadau

Rhagor o Adnoddau

PDF o Fersiynau Diwygiedig

- ddiwygiedig 10/12/20200.49 MB

Deddfwriaeth yn deillio o’r UE

Pan adawodd y DU yr UE, cyhoeddodd legislation.gov.uk ddeddfwriaeth yr UE a gyhoeddwyd gan yr UE hyd at ddiwrnod cwblhau’r cyfnod gweithredu (31 Rhagfyr 2020 11.00 p.m.). Ar legislation.gov.uk, mae'r eitemau hyn o ddeddfwriaeth yn cael eu diweddaru'n gyson ag unrhyw ddiwygiadau a wnaed gan y DU ers hynny.

Mae'r eitem hon o ddeddfwriaeth yn tarddu o'r UE

Mae legislation.gov.uk yn cyhoeddi fersiwn y DU. Mae EUR-Lex yn cyhoeddi fersiwn yr UE. Mae Archif Gwe Ymadael â’r UE yn rhoi cipolwg ar fersiwn EUR-Lex o ddiwrnod cwblhau’r cyfnod gweithredu (31 Rhagfyr 2020 11.00 p.m.).

Changes over time for: Commission Regulation (EU) No 1388/2014

Version Superseded: 31/12/2020

Alternative versions:

Status:

Point in time view as at 10/12/2020.

Changes to legislation:

There are currently no known outstanding effects by UK legislation for Commission Regulation (EU) No 1388/2014.

Changes to Legislation

Revised legislation carried on this site may not be fully up to date. At the current time any known changes or effects made by subsequent legislation have been applied to the text of the legislation you are viewing by the editorial team. Please see ‘Frequently Asked Questions’ for details regarding the timescales for which new effects are identified and recorded on this site.

Commission Regulation (EU) No 1388/2014

of 16 December 2014

declaring certain categories of aid to undertakings active in the production, processing and marketing of fishery and aquaculture products compatible with the internal market in application of Articles 107 and 108 of the Treaty on the Functioning of the European Union

THE EUROPEAN COMMISSION,

Having regard to the Treaty on the Functioning of the European Union, and in particular Article 108(4) thereof,

Having regard to Council Regulation (EC) No 994/98 of 7 May 1998 on the application of Articles 107 and 108 of the Treaty on the Functioning of the European Union to certain categories of horizontal State aid(1), and in particular Article 1(1) (a)(i) and (vi) thereof,

Having published a draft of this Regulation(2),

After consulting the Advisory Committee on State Aid,

Whereas:

(1) State funding meeting the criteria laid down in Article 107(1) of the Treaty constitutes State aid and requires notification to the Commission by virtue of Article 108(3) thereof. However, pursuant to Article 109 of the Treaty, the Council may determine categories of aid that are exempted from this notification requirement. In accordance with Article 108(4) of the Treaty, the Commission may adopt regulations relating to those categories of aid.

(2) Regulation (EC) No 994/98 empowers the Commission to declare, in accordance with Article 109 of the Treaty, that certain categories of aid may, under certain conditions, be exempted from the notification requirement. On the basis of that Regulation, the Commission adopted Commission Regulation (EC) No 736/2008(3) which provided that, under certain conditions, aid to small and medium-sized enterprises (‘SMEs’) active in the production, processing and marketing of fisheries products is compatible with the internal market and not subject to the notification requirement of Article 108(3) of the Treaty. Regulation (EC) No 736/2008 applied until 31 December 2013.

(3) The Commission has applied Articles 107 and 108 of the Treaty to SMEs active in the production, processing and marketing of fishery and aquaculture products in numerous decisions. It has also stated its policy in guidelines specific to that sector. In the light of the Commission's experience in applying those provisions to SMEs, it is appropriate for the Commission to continue making use of the powers conferred by Regulation (EC) No 994/98 in order to exempt aid to that category of undertakings from the notification requirement of Article 108(3) of the Treaty under certain conditions.

(4) On 22 July 2013 Regulation (EC) No 994/98 was amended by Council Regulation (EU) No 733/2013(4) to empower the Commission to extend the block exemption to new categories of aid in respect of which clear compatibility conditions can be defined. In the fishery and aquaculture sector, this is the case for aid to make good the damage caused by certain natural disasters, in light of the Commission's experience in applying Article 107(2)(b) of the Treaty to this category of aid.

(5) The compatibility of State aid in the fishery and aquaculture sector is assessed by the Commission on the basis of the objectives of both the Competition Policy and the Common Fisheries Policy. In the interests of coherence with Union-financed support measures, the maximum intensity of public aid allowed under this Regulation should be equal to that fixed for the same kind of aid in Article 95 of Regulation (EU) No 508/2014 of the European Parliament and of the Council(5) and the implementing acts adopted pursuant to that Regulation.

(6) It is essential that no aid is granted in circumstances where Union law, and in particular rules of the Common Fisheries Policy, are not complied with. An aid may therefore only be granted by a Member State in the fishery and aquaculture sector if the measures financed and their effects comply with Union law. Member States should ensure that beneficiaries of State aid comply with the rules of the Common Fisheries Policy.

(7) With its Communication on EU State Aid Modernisation (SAM)(6), the Commission launched a wider review of the State aid rules. The main objectives of that modernisation are: (i) to achieve sustainable, smart and inclusive growth in a competitive internal market, while contributing to Member State efforts towards a more efficient use of public finances; (ii) to focus Commission ex ante scrutiny of aid measures on cases with the biggest impact on the internal market, while strengthening Member State cooperation in State aid enforcement; and (iii) to streamline the rules and provide for faster, better informed and more robust decisions based on a clear economic rationale, a common approach and clear obligations. This Regulation is part of the SAM programme.

(8) This Regulation should allow for better prioritisation of State aid enforcement activities and greater simplification and should enhance transparency, effective evaluation and the control of compliance with the State aid rules at national and Union levels, while preserving the institutional competences of the Commission and the Member States. In accordance with the principle of proportionality, this Regulation does not go beyond what is necessary in order to achieve those objectives.

(9) The general conditions for the application of this Regulation should be defined on the basis of a set of common principles that ensure that the aid serves a purpose of common interest, has a clear incentive effect, is appropriate and proportionate, is granted in full transparency and subject to a control mechanism and regular evaluation and does not adversely affect trading conditions to an extent that is contrary to the common interest.

(10) Aid that fulfils all the conditions laid down in this Regulation both general and specific to the relevant categories of aid should be considered compatible with the internal market and exempted from the notification requirement laid down in Article 108(3) of the Treaty.

(11) State aid within the meaning of Article 107(1) of the Treaty not covered by this Regulation or by other Regulations adopted pursuant to Article 1 of Regulation (EC) No 994/98 remains subject to the notification requirement of Article 108(3) of the Treaty. This Regulation is without prejudice for Member States to notify aid potentially covered by this Regulation. Such aid should be assessed in the light of the Guidelines for the examination of State aid in the fishery and aquaculture sector or any successor guidelines(7).

(12) This Regulation should not apply to aid contingent upon the use of domestic over imported products or aid to export-related activities. In particular, it should not apply to aid financing the establishment and operation of a distribution network in other Member States or third countries. Aid towards the cost of participating in trade fairs or of studies or consultancy services needed for the launch of a new or existing product on a new market in another Member State or third country should not normally constitute aid to export-related activities.

(13) The Commission should ensure that authorised aid does not adversely affect trading conditions to an extent that is contrary to the common interest. Therefore, aid in favour of a beneficiary which is subject to an outstanding recovery order following a previous Commission decision declaring an aid illegal and incompatible with the internal market should be excluded from the scope of this Regulation, with the exception of aid schemes to make good the damage caused by natural disasters.

(14) Aid granted to undertakings in difficulty should be excluded from the scope of this Regulation, since such aid should be assessed under the Guidelines on State aid for rescuing and restructuring non-financial undertakings in difficulty(8), in order to avoid their circumvention, with the exception of aid schemes to make good the damage caused by natural disasters. In order to provide legal certainty, it is appropriate to establish clear criteria that do not require an assessment of all the particularities of the situation of an undertaking to determine whether an undertaking is considered to be in difficulty for the purposes of this Regulation.

(15) State aid enforcement is highly dependent on the cooperation of Member States. Therefore, Member States should take all necessary measures to ensure compliance with this Regulation, including compliance of individual aid granted under block-exempted schemes.

(16) In view of the need to strike the appropriate balance between minimising distortions of competition in the aided sector and the objectives of this Regulation, this Regulation should not exempt individual grants which exceed a fixed maximum amount, whether or not made under an aid scheme exempted by this Regulation.

(17) For the purpose of transparency, equal treatment and effective monitoring, this Regulation should apply only to aid in respect of which it is possible to calculate precisely the gross grant equivalent ex ante without the need to undertake a risk assessment (‘transparent aid’).

(18) This Regulation should define the conditions under which certain specific aid instruments, such as loans, guarantees, tax measures, and, in particular, repayable advances may be considered transparent. Aid comprised in guarantees should be considered as transparent if the gross grant equivalent has been calculated on the basis of safe-harbour premiums laid down for the respective type of undertaking. In the case of SMEs, the Commission Notice on the application of Articles 87 and 88 of the EC Treaty to State aid in the form of guarantees(9) indicates levels of annual premium above which a State guarantee would be deemed not to constitute aid. For the purposes of this Regulation, capital injections and risk capital measures should not be considered transparent aid.

(19) In order to ensure that the aid is necessary and acts as an incentive to further develop activities or projects, this Regulation should not apply to aid for activities in which the beneficiary would in any case engage even in the absence of the aid. Aid should only be exempted from notification requirement of Article 108(3) of the Treaty in accordance with this Regulation, where the activity or the work on the aided project starts after the beneficiary has submitted a written application for the aid.

(20) Automatic aid schemes in the form of tax advantages should continue to be subject to a specific condition concerning the incentive effect, due to the fact that this kind of aid is granted under different procedures than other categories of aid. Such schemes should already have been adopted before work on the aided project or activity started. However, this condition should not apply in the case of fiscal successor schemes provided the activity was already covered by the previous fiscal schemes in the form of tax advantages. For the assessment of the incentive effect of such schemes, the crucial moment is the moment when the tax measure was set out for the first time in the original scheme, which is then replaced by the successor scheme.

(21) For the calculation of aid intensity, only eligible costs should be included. This Regulation should not exempt aid which exceeds the relevant aid intensity as a result of including ineligible costs. The identification of eligible costs should be supported by clear, specific and up-to date documentary evidence. All figures used should be taken before any deduction of tax or other charges. Aid payable in several instalments should be discounted to its value on the date of granting of the aid. The eligible costs should also be discounted to their value on the date of granting. The interest rate to be used for discounting purposes and for calculating the amount of aid in the case of aid which does not take the form of a grant should be respectively the discount rate and the reference rate applicable at the time of the grant, as laid down in the Commission Communication on the revision of the method for setting the reference and discount rates(10). Where aid is granted by means of tax advantages, aid tranches should be discounted on the basis of the discount rates applicable on the various dates when the tax advantages become effective. The use of aid in the form of repayable advances should be promoted, since such risk-sharing instruments are conducive to strengthened incentive effect of aid. It is therefore appropriate to establish that where aid is granted in the form of repayable advances the applicable aid intensities referred to in this Regulation may be increased.

(22) In the case of tax advantages on future taxes, the applicable discount rate and the exact amount of the aid tranches may not be known in advance. In such cases, Member States should set in advance a cap on the discounted value of the aid respecting the applicable aid intensity. Subsequently, when the amount of the aid tranche at a given date becomes known, discounting can take place on the basis of the discount rate applicable at that time. The discounted value of each aid tranche should be deducted from the overall amount of the cap (‘capped amount’).

(23) To determine whether the notification thresholds and the maximum aid intensities referred to in this Regulation are respected, the total amount of public support for the aided activity or project should be taken into account. Moreover, this Regulation should specify the circumstances under which different categories of aid may be cumulated. Aid exempted by this Regulation and any other compatible aid exempted under other regulations or approved by the Commission may be cumulated as long as those measures concern different identifiable eligible costs. Where different sources of aid are related to the same — partly or fully overlapping — identifiable eligible costs, cumulation should be allowed up to the highest aid intensity or aid amount applicable to that aid under this Regulation. This Regulation should also set out special rules for cumulation of aid measures with de minimis aid. De minimis aid is often not granted for or attributable to specific identifiable eligible costs. In such a case, it should be possible to freely cumulate de minimis aid with State aid exempted under this Regulation. Where, however, de minimis aid is granted for the same identifiable eligible costs as State aid exempted under this Regulation, cumulation should only be allowed up to the maximum aid intensity as referred to in Chapter III of this Regulation.

(24) Given that State aid within the meaning of Article 107(1) of the Treaty is, in principle, prohibited, it is important for all parties to be able to check whether an aid is granted in compliance with the applicable rules. Transparency of State aid is, therefore, essential for the correct application of Treaty rules and leads to better compliance, greater accountability, peer review and ultimately more effective public spending. To ensure transparency, Member States should be required to establish comprehensive State aid websites, at regional or national level, setting out summary information about each aid measure exempted under this Regulation. That obligation should be a condition for the compatibility of the individual aid with the internal market. Following the standard practice regarding publication of information in Directive 2013/37/EU of the European Parliament and of the Council(11), a standard format should be used which allows the information to be searched, downloaded and easily published on the Internet. The links to the State aid websites of all the Member States should be published on the Commission's website. In accordance with Article 3 of Regulation (EC) No 994/98, as amended by Regulation (EU) No 733/2013, summary information on each aid measure exempted under this Regulation should be published on the website of the Commission.

(25) To ensure effective monitoring of aid measures in accordance with Regulation (EC) No 994/98, as amended by Regulation (EU) No 733/2013, it is appropriate to establish requirements regarding the reporting by the Member States of aid measures which have been exempted pursuant to this Regulation and the application of this Regulation. Moreover, it is appropriate to establish rules concerning the records that Member States should keep regarding the aid exempted by this Regulation, in light of the limitation period established in Article 15 of Council Regulation (EC) No 659/1999(12). Finally, each individual aid should contain an express reference to this Regulation.

(26) To reinforce the effectiveness of compatibility conditions set out in this Regulation, it should be possible for the Commission to withdraw the benefit of the block exemption for future aid measures in the event of failure to comply with these requirements. The Commission should be able to restrict the withdrawal of the benefit of the block exemption to certain types of aid, certain beneficiaries or aid measures adopted by certain authorities, where non-compliance with this Regulation affects only a limited group of measures or certain authorities. Such a targeted withdrawal should provide a proportionate remedy directly linked to the identified non-compliance with this Regulation. In case of failure to meet compatibility conditions set out in Chapters I and III, aid granted will not be covered by this Regulation and, as a consequence, will constitute unlawful aid, which the Commission will examine in the framework of the relevant procedure as set out in Regulation No (EC) No 659/1999. In case of failure to fulfil the requirements of Chapter II, the withdrawal of the benefit of the block exemption in respect of the future aid measures does not affect the fact that the past measures complying with this Regulation were block exempted.

(27) To eliminate differences that might give rise to distortions of competition and to facilitate coordination between different Union and national initiatives concerning SMEs, as well as for reasons of administrative clarity and legal certainty, the definition of SMEs used for the purpose of this Regulation should be based on the definition in Commission Recommendation 2003/361/EC(13).

(28) This Regulation should cover types of aid granted in the fishery and aquaculture sector which have been systematically approved by the Commission for many years. This aid should not require a case-by-case assessment of its compatibility with the internal market from the Commission, provided that it complies with the conditions laid down in Regulation (EU) No 508/2014.

(29) In accordance with Article 107(2)(b) of the Treaty, aid to make good the damage caused by natural disasters is compatible with the internal market. In order to provide legal certainty, it is necessary to define the type of the events that may constitute a natural disaster exempted by this Regulation. For the purposes of this Regulation, earthquakes, landslides, floods, in particular floods brought about by waters overflowing river banks or lake shores, avalanches, tornadoes, hurricanes, volcanic eruptions and wildfires of natural origin should be considered events constituting a natural disaster. Damage caused by adverse weather conditions such as storms, frost, hail, ice, rain or drought, which occur on a more regular basis, should not be considered a natural disaster within the meaning of Article 107(2)(b) of the Treaty. In order to ensure that the exemption covers indeed aid granted to make good the damage caused by natural disasters, this Regulation should lay down, following established practice, the conditions under which such aid schemes may benefit from that block exemption. Those conditions should relate, in particular, to the formal recognition by the competent Member States' authorities of the character of the event as a natural disaster and to a direct causal link between the natural disaster and the damages suffered by the beneficiary undertaking, which may include undertakings in difficulty, and should ensure that overcompensation is avoided. The compensation should not exceed what is necessary to enable the beneficiary to return to the situation prevailing before the disaster occurred.

(30) Pursuant to Article 15(1)(f) and Article 15(3) of Council Directive 2003/96/EC(14), Member States may introduce tax exemptions or reductions applicable to inland fishing and piscicultural works. It is therefore appropriate to continue exempting those measures from the notification requirement of Article 108(3) of the Treaty where the conditions provided under that Directive are fulfilled. Tax exemptions applicable to fishing within EU waters which Member States are to introduce pursuant to Article 14 (1)(c) of that Directive are not imputable to the State and therefore should not constitute State aid.

(31) In the light of the Commission's experience in this area, State aid policy should periodically be revised. The period of application of this Regulation should therefore be limited and transitional provisions should be laid down. Having regard to the fact that the conditions for granting aid under this Regulation have been aligned with the conditions established for the application of Regulation (EU) No 508/2014(15), it is appropriate to ensure consistency between the period of application of this Regulation and the period of application of Regulation (EU) No 508/2014. Should this Regulation expire without being extended, aid schemes already exempted by this Regulation should continue to be exempted for six months.

HAS ADOPTED THIS REGULATION:

CHAPTER IU.K. COMMON PROVISIONS

Article 1U.K.Scope

1.This Regulation shall apply to aid granted to small and medium-sized enterprises (SMEs) active in the production, processing or marketing of fishery and aquaculture products.

2.This Regulation shall also apply to aid granted to undertakings active in the production, processing or marketing of fishery and aquaculture products to make good the damage caused by natural disasters in accordance with Article 44 independently of the size of the beneficiary of the aid.

3.This Regulation shall not apply to:

(a)aid the amount of which is fixed on the basis of price or quantity of products put on the market;

(b)aid to export-related activities towards third countries or Member States, namely aid directly linked to the quantities exported, to the establishment and operation of a distribution network or to other current costs linked to the export activity;

(c)aid contingent upon the use of domestic over imported goods;

[F1(d) aid granted to undertakings in difficulty, with the exception of aid to make good the damage caused by natural disasters and aid to undertakings which were not in difficulty on 31 December 2019 but became undertakings in difficulty in the period from 1 January 2020 to 30 June 2021 ;]

(e)aid schemes which do not explicitly exclude the payment of individual aid in favour of an undertaking which is subject to an outstanding recovery order following a previous Commission decision declaring an aid illegal and incompatible with the internal market, with the exception of aid schemes to make good the damage caused by natural disasters;

(f)ad hoc aid in favour of an undertaking as referred to in point (e);

(g)aid granted to operations which would have been ineligible for support under Article 11 of Regulation (EU) No 508/2014;

(h)aid granted to undertakings that cannot apply for support from the European Maritime and Fisheries Fund on the grounds set out in Article 10(1)-(3) of Regulation (EU) No 508/2014.

4.This Regulation shall not apply to State aid measures, which entail, by themselves, by the conditions attached to them or by their financing method a non-severable violation of Union law, in particular:

(a)aid where the grant of aid is subject to the obligation for the beneficiary to have its headquarters in the relevant Member State or to be predominantly established in that Member State. However, the requirement to have an establishment or branch in the aid granting Member State at the moment of payment of the aid is allowed;

(b)aid where the grant of aid is subject to the obligation for the beneficiary to use nationally produced goods or national services;

(c)aid restricting the possibility for the beneficiaries to exploit the research, development and innovation results in other Member States.

Textual Amendments

Article 2U.K.Notification threshold

1.This Regulation shall not apply to aid for any project with eligible costs in excess of EUR 2 million, or where the amount of aid exceeds EUR 1 million per beneficiary per year.

2.The thresholds set out in paragraph 1 shall not be circumvented by artificially splitting up the aid schemes or aid projects.

Article 3U.K.Definitions

For the purpose of this Regulation the following definitions shall apply:

(1)

‘aid’ means any measure fulfilling all the criteria laid down in Article 107(1) of the Treaty;

(2)

‘small and medium-sized undertakings’ or ‘SMEs’ means undertakings fulfilling the criteria laid down in Annex I;

(3)

‘fishery and aquaculture products’ means the products defined in Annex I of Regulation (EU) No 1379/2013 of the European Parliament and of the Council of 11 December 2013(16);

(4)

‘natural disasters’ means earthquakes, avalanches, landslides and floods, tornadoes, hurricanes, volcanic eruptions and wild fires of natural origin;

(5)

‘undertaking in difficulty’ means an undertaking in respect of which at least one of the following circumstances occurs:

(a)

in the case of a limited liability company (other than an SME that has been in existence for less than three years), where more than half of its subscribed share capital has disappeared as a result of accumulated losses. This is the case when deduction of accumulated losses from reserves (and all other elements generally considered as part of the own funds of the company) leads to a negative cumulative amount that exceeds half of the subscribed share capital. For the purposes of this provision, ‘limited liability company’ refers in particular to the types of company mentioned in Annex I of Directive 2013/34/EU of the European Parliament and of the Council(17) and ‘share capital’ includes, where relevant, any share premium;

(b)

in the case of a company where at least some members have unlimited liability for the debt of the company (other than an SME that has been in existence for less than three years), where more than half of its capital as shown in the company accounts has disappeared as a result of accumulated losses. For the purposes of this provision, ‘a company where at least some members have unlimited liability for the debt of the company’ refers in particular to the types of company mentioned in Annex II to Directive 2013/34/EU;

(c)

where the undertaking is subject to collective insolvency proceedings or fulfils the criteria under its domestic law for being placed in collective insolvency proceedings at the request of its creditors;

(d)

where the undertaking has received rescue aid and has not yet reimbursed the loan or terminated the guarantee, or has received restructuring aid and is still subject to a restructuring plan;

(6)

‘ad hoc aid’ means aid not granted on the basis of an aid scheme;

(7)

‘aid scheme’ means any act on the basis of which, without further implementing measures being required, individual aid awards may be made to undertakings defined within the act in a general and abstract manner and any act on the basis of which aid which is not linked to a specific project may be granted to one or several undertakings for an indefinite period of time and/or for an indefinite amount;

(8)

‘individual aid’ means:

(a)

ad hoc aid; and

(b)

awards of aid to individual beneficiaries on the basis of an aid scheme;

(9)

‘gross grant equivalent’ means the amount of the aid if it had been provided in the form of a grant to the beneficiary, before any deduction of tax or other charges;

(10)

‘repayable advance’ means a loan for a project which is paid in one or more instalments and the conditions for the reimbursement of which depend on the outcome of the project;

(11)

‘start of works’ means the earlier of either the start of construction works relating to the investment, or the first legally binding commitment to order equipment or any other commitment that makes the investment irreversible. Buying land and preparatory works such as obtaining permits and conducting feasibility studies are not considered start of works. For take-overs, ‘start of works’ means the moment of acquiring assets directly linked to the acquired establishment;

(12)

‘fiscal successor scheme’ means a scheme in the form of tax advantages which constitutes an amended version of a previously existing scheme in the form of tax advantages and which replaces it;

(13)

‘aid intensity’ means the gross aid amount expressed as a percentage of the eligible costs, before any deduction of tax or other charge;

(14)

‘date of granting the aid’ means the date when the legal right to receive the aid is conferred on the beneficiary under the applicable national legal regime.

Article 4U.K.Conditions for exemption

1.Aid schemes, individual aid granted under aid schemes and ad hoc aid shall be compatible with the internal market within the meaning of Article 107(2) or (3) of the Treaty and shall be exempted from the notification requirement of Article 108(3) of the Treaty provided that such aid fulfils the conditions laid down in Chapter I of this Regulation, as well as the specific conditions for the relevant category of aid laid down in Chapter III of this Regulation.

2.Aid measures shall only be exempted under this Regulation as far as they explicitly provide that, during the grant period, the beneficiaries of the aid shall comply with the rules of the Common Fisheries Policy and that, if during that period it is found that the beneficiary does not comply with rules of the Common Fisheries Policy, the aid shall be reimbursed in proportion to the gravity of the infringement.

Article 5U.K.Transparency of aid

1.This Regulation shall apply only to aid in respect of which it is possible to calculate precisely the gross grant equivalent of the aid ex ante without any need to undertake a risk assessment (‘transparent aid’).

2.The following categories of aid shall be considered to be transparent:

(a)aid comprised in grants and interest rate subsidies;

(b)aid comprised in loans where the gross grant equivalent has been calculated on the basis of the reference rate prevailing at the time of the grant;

(c)aid comprised in guarantees:

(i)

where the gross grant equivalent has been calculated on the basis of safe-harbour premiums laid down in a Commission notice; or

(ii)

where before the implementation of the measure, the methodology to calculate the gross grant equivalent of the guarantee has been accepted on the basis of the Commission Notice on the application of Articles 87 and 88 of the EC Treaty to State aid in the form of guarantees(18), or any successor notice, following notification of that methodology to the Commission under any regulation adopted by the Commission in the State aid area applicable at the time, and the approved methodology explicitly addresses the type of guarantee and the type of underlying transaction at stake in the context of the application of this Regulation;

(d)aid in the form of tax advantages, where the measure provides for a cap ensuring that the applicable threshold is not exceeded;

(e)aid in the form of repayable advances, if the total nominal amount of the repayable advance does not exceed the thresholds applicable under this Regulation or if, before implementation of the measure, the methodology to calculate the gross grant equivalent of the repayable advance has been accepted following its notification to the Commission.

3.For the purposes of this Regulation, the following categories of aid shall not be considered to be transparent aid:

(a)aid comprised in capital injections;

(b)aid comprised in risk finance measures.

Article 6U.K.Incentive effect

1.This Regulation shall apply only to aid which has an incentive effect.

2.Aid shall be considered to have an incentive effect if the beneficiary has submitted a written application for the aid to the Member State concerned before work on the project or activity starts. The application for the aid shall contain at least the following information:

(a)undertaking's name and size;

(b)description of the project or activity, including its start and end dates;

(c)location of the project or activity;

(d)list of eligible costs;

(e)type of aid (grant, loan, guarantee, repayable advance or other) and amount of public funding needed for the project or activity.

3.By way of derogation from paragraph 2, measures in the form of tax advantages shall be deemed to have an incentive effect if the following conditions are fulfilled:

(a)the measure establishes a right to aid in accordance with objective criteria and without further exercise of discretion by the Member State; and

(b)the measure has been adopted and is in force before work on the aided project or activity has started, except in the case of fiscal successor schemes where the activity was already covered by the previous schemes in the form of tax advantages.

4.By way of derogation from paragraphs 1 and 2, the following categories of aid are not required to have or shall be deemed to have an incentive effect:

(a)aid to make good the damage caused by natural disasters, if the conditions laid down in Article 44 are fulfilled;

(b)aid in the form of tax exemptions or reductions adopted by the Member States pursuant to Article 15(1)(f) and Article 15(3) of Directive 2003/96/EC, if the conditions laid down in Article 45 of this Regulation are fulfilled.

Article 7U.K.Aid intensity and eligible costs

1.For the purpose of calculating aid intensity and eligible costs, all figures used shall be taken before any deduction of tax or other charge. The eligible costs shall be supported by documentary evidence which shall be clear, specific and contemporary.

2.Where aid is granted in a form other than a grant, the aid amount shall be the gross grant equivalent of the aid.

3.Aid payable in several instalments shall be discounted to its value on the date of granting the aid. The eligible costs shall be discounted to their value on the date of granting the aid. The interest rate to be used for discounting purposes shall be the discount rate applicable on the date of granting the aid.

4.Where aid is granted by means of tax advantages discounting of aid tranches shall take place on the basis of the discount rates applicable on the various dates when the tax advantage takes effect.

5.Where aid is granted in the form of repayable advances which, in the absence of an accepted methodology to calculate their gross grant equivalent, are expressed as a percentage of the eligible costs and the measure provides that in case of a successful outcome of the project, as defined on the basis of a reasonable and prudent hypothesis, the advances will be repaid with an interest rate at least equal to the discount rate applicable on the date of granting the aid, the maximum aid intensities laid down in Chapter III may be increased by 10 percentage points.

6.The eligible costs shall comply with the requirements of Articles 67 to 69 of Regulation (EU) No 1303/2013 of the European Parliament and of the Council(19).

Article 8U.K.Cumulation

1.In determining whether the notification thresholds in Article 2 and the maximum aid intensities in Chapter III are respected, the total amount of public support measures for the aided activity or project or undertaking shall be taken into account, regardless of whether that support is financed from local, regional, national or Union sources.

2.Aid exempted by this Regulation may be cumulated with:

(a)any other State aid, as long as those measures concern different identifiable eligible costs;

(b)any other State aid, in relation to the same eligible costs, partly or fully overlapping, only if such cumulation does not result in exceeding the highest aid intensity or aid amount applicable to this aid under this Regulation.

3.State aid exempted under this Regulation shall not be cumulated with any de minimis aid in respect of the same eligible costs if such cumulation would result in an aid intensity exceeding those referred to in Chapter III.

Article 9U.K.Publication and information

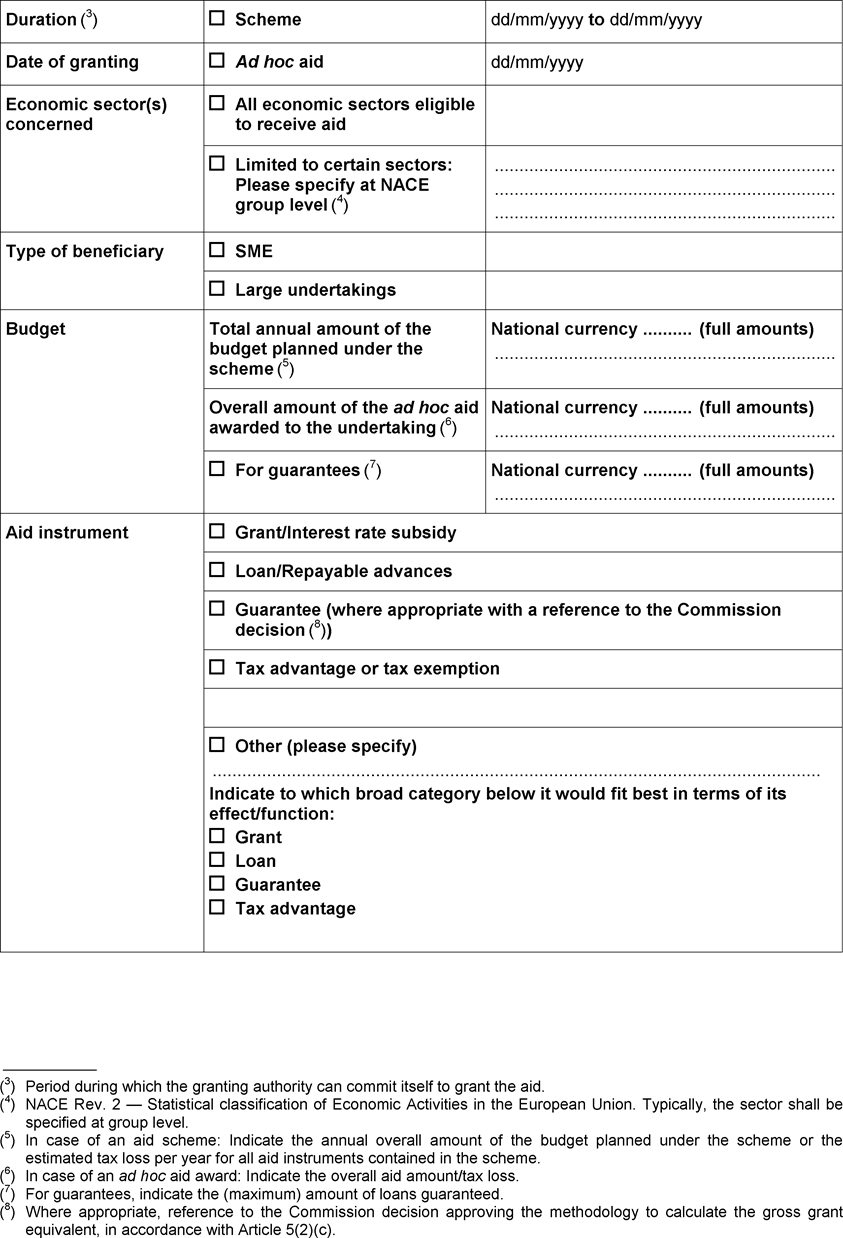

1.The Member State concerned shall ensure the publication on a comprehensive State aid website, at national or regional level of:

(a)the summary information referred to in Article 11 in the standardised format laid down in Annex II or a link providing access to it;

(b)the full text of each aid measure as referred to in Article 11 or a link providing access to the full text;

(c)the information referred to in Annex III on each individual aid award exceeding EUR 30 000.

2.For schemes in the form of tax advantages, the conditions set out in paragraph 1(c) shall be considered fulfilled if Member States publish the required information on individual aid amounts in the following ranges (in EUR million):

(a)0,03-0,2

(b)0,2-0,4

(c)0,4-0,6

(d)0,6-0,8

(e)0,8-1

3.The information referred to in paragraph 1(c) shall be organised and accessible in a standardised manner, as described in Annex III, and shall allow for effective search and download functions. The information referred to in paragraph 1 shall be published within six months from the date the aid was granted, or for aid in the form of tax advantage, within one year from the date the tax declaration is due, and shall be available for at least 10 years from the date on which the aid was granted.

4.Each aid scheme and individual aid shall contain an explicit reference to this Regulation, by citing its title and publication reference in the Official Journal of the European Union, and to the specific provisions of Chapter III concerned by that act, or where applicable, to the national law which ensures that the relevant provisions of this Regulation are complied with. It shall be accompanied by its implementing provisions and its amendments.

5.The Commission shall publish on its website:

(a)the links to the State aid websites, referred to in paragraph 1 of this Article;

(b)the summary information referred to in Article 11.

6.Member States shall comply with the provisions of this Article at the latest within two years after the entry into force of this Regulation.

CHAPTER IIU.K. MONITORING

Article 10U.K.Withdrawal of the benefit of the block exemption

Where a Member State grants aid allegedly exempted from the notification requirement under this Regulation without fulfilling the conditions set out in Chapters I, II and III, the Commission may, after having provided the Member State concerned with the possibility to make its views known, adopt a decision stating that all or some of the future aid measures adopted by the Member State concerned which would otherwise fulfil the requirements of this Regulation, are to be notified to the Commission in accordance with Article 108(3) of the Treaty. The measures to be notified may be limited to measures granting certain types of aid, in favour of certain beneficiaries or adopted by certain authorities of the Member State concerned.

Article 11U.K.Reporting

Member States shall transmit to the Commission:

(a)

via the Commission's electronic notification system, the summary information about each aid measure exempted under this Regulation in the standardised format laid down in Annex II, together with a link providing access to the full text of the aid measure, including its amendments, within 20 working days following its entry into force;

(b)

an annual report, as referred to in Commission Regulation (EC) No 794/2004(20), in electronic form, on the application of this Regulation, containing the information indicated in Regulation (EC) No 794/2004, in respect of each whole year or each part of the year during which this Regulation applies.

[F2Article 11a U.K. Derogation from information and publication requirements

By way of derogation from Article 9(5) and Article 11, point (a), where a Member State wishes to prolong measures in respect of which summary information was submitted to the Commission, summary information regarding the prolongation of those measures shall be deemed to have been communicated to the Commission and published, provided that no substantive amendment, other than a budget increase, is made to the measures concerned.]

Textual Amendments

Article 12U.K.Monitoring

In order to enable the Commission to monitor the aid exempted from notification by this Regulation, Member States shall maintain detailed records with the information and supporting documentation necessary to establish that all the conditions laid down in this Regulation are fulfilled. Such records shall be kept for 10 years from the date on which the ad hoc aid was granted or the last aid was granted under the scheme. The Member State concerned shall provide the Commission within a period of 20 working days or such longer period as may be fixed in the request, with all the information and supporting documentation which the Commission considers necessary to monitor the application of this Regulation.

CHAPTER IIIU.K. SPECIFIC PROVISIONS FOR DIFFERENT CATEGORIES OF AID

SECTION 1 U.K. Sustainable development of fisheries

Article 13U.K.Aid for innovation

Aid for innovation in fisheries fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 26 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 14U.K.Aid for advisory services

Aid for advisory services fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 27 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 15U.K.Aid for partnership between scientists and fishermen

Aid for partnership between scientists and fishermen fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 28 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 16U.K.Aid to promote human capital, job creation and social dialogue

Aid to promote human capital, job creation and social dialogue fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 29 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 17U.K.Aid to facilitate diversification and new forms of income

Aid to facilitate diversification and new forms of income fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 30 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 18U.K.Aid to start-up support for young fishermen

Aid to start-up support for young fishermen fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 31 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 19U.K.Aid to improve health and safety

Aid to improve health and safety fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 32 of Regulation (EU) No 508/2014 and the delegated acts adopted on the basis of Article 32(4) of that Regulation; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 20U.K.Aid to mutual funds for adverse climatic events and environmental incidents

Aid to mutual funds for adverse climatic events and environmental incidents fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 35 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 21U.K.Aid to support systems of allocation of fishing opportunities

Aid to support systems of allocation of fishing opportunities fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 36 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 22U.K.Aid to support the design and implementation of conservation measures and regional cooperation

Aid to support the design and implementation of conservation measures and regional cooperation fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 37 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 23U.K.Aid to limit the impact of fishing on the marine environment and adapt fishing to the protection of species

Aid to limit the impact of fishing on the marine environment and adapt fishing to the protection of species fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 38 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 24U.K.Aid to innovation linked to the conservation of marine biological resources

Aid to innovation linked to the conservation of marine biological resources fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 39 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 25U.K.Aid for the protection and restoration of marine biodiversity and ecosystems and compensation regimes in the framework of sustainable fishing activities

Aid for the protection and restoration of marine biodiversity and ecosystems and compensation regimes in the framework of sustainable fishing activities fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 40 of Regulation (EU) No 508/2014 and the delegated acts adopted on the basis of Article 40(4) of that Regulation; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 26U.K.Aid to improve energy efficiency and to mitigate the effects of climate change

Aid to improve energy efficiency and to mitigate the effects of climate change, with the exception of aid to replace or modernise engines, fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 41 of Regulation (EU) No 508/2014 and the delegated acts adopted on the basis of Article 41(10) of that Regulation; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 27U.K.Aid to added value, product quality and use of unwanted catches

Aid to added value, product quality and use of unwanted catches fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 42 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 28U.K.Aid to fishing ports, landing sites, auction halls and shelters

Aid to fishing ports, landing sites, auction halls and shelters fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 43 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 29U.K.Aid to inland fishing and inland aquatic fauna and flora

Aid to inland fishing and inland aquatic fauna and flora fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 25(1) and (2) and Article 44 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

SECTION 2 U.K. Sustainable development of aquaculture

Article 30U.K.Aid for innovation in aquaculture

Aid for innovation in aquaculture fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 47 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 31U.K.Aid to productive investments in aquaculture

Aid to productive investments in aquaculture fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 48 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 32U.K.Aid to management, relief and advisory services for aquaculture farms

Aid to management, relief and advisory services for aquaculture farms fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 49 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 33U.K.Aid to promote human capital and networking in aquaculture

Aid to promote human capital and networking in aquaculture fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 50 of Regulation (EU) No 508/2014 and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 34U.K.Aid to increase the potential of aquaculture sites

Aid to increase the potential of aquaculture sites fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 51 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 35U.K.Aid to encourage new aquaculture farmers practising sustainable aquaculture

Aid to encourage new aquaculture farmers practising sustainable aquaculture fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 52 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 36U.K.Aid for the conversion to eco-management and audit schemes and organic aquaculture

Aid for the conversion to eco-management and audit schemes and organic aquaculture fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 53 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 37U.K.Aid to aquaculture providing environmental services

Aid to aquaculture providing environmental services fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 54 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 38U.K.Aid for public health measures

Aid for public health measures fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 55 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 39U.K.Aid for animal health and welfare measures

Aid for animal health and welfare measures fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 56 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 40U.K.Aid for aquaculture stock insurance

Aid for aquaculture stock insurance fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Articles 46 and 57 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

SECTION 3 U.K. Marketing and processing related measures

Article 41U.K.Aid for marketing measures

Aid for marketing measures fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 68 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 42U.K.Aid for the processing of fishery and aquaculture products

Aid for the processing of fishery and aquaculture products fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 69 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

SECTION 4 U.K. Other categories of AID

Article 43U.K.Aid for data collection

Aid for data collection fulfilling the conditions laid down in Chapter I shall be compatible with the internal market within the meaning of Article 107(3)(c) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof provided that:

(a)

the aid fulfils the conditions of Article 77 of Regulation (EU) No 508/2014; and

(b)

the amount of the aid does not exceed, in gross grant equivalent, the maximum intensity of public aid fixed by Article 95 of Regulation (EU) No 508/2014 and the implementing acts adopted on the basis of Article 95(5) of that Regulation.

Article 44U.K.Aid to make good the damage caused by natural disasters

1.Aid schemes to make good the damage caused by natural disasters shall be compatible with the internal market within the meaning of Article 107(2)(b) of the Treaty and shall be exempted from the notification requirement of Article 108(3) thereof where it fulfils the conditions laid down in this Article and in Chapter I.

2.Aid granted under this Article shall be granted subject to the following conditions:

(a)the competent authority of the Member State has formally recognized the character of the event as a natural disaster; and

(b)there is a direct causal link between the natural disaster and the damage suffered by the undertaking.

3.Aid shall be paid directly to the undertaking concerned.

4.Aid schemes related to a specific natural disaster shall be established within three years from the date of the occurrence of the natural disaster. The aid shall be paid out within four years from that date.

5.The eligible costs shall be the damage incurred as a direct consequence of the natural disaster, as assessed either by a public authority, by an independent expert recognized by the granting authority or by an insurance undertaking. That damage may include the following:

(a)material damage to assets such as buildings, equipment, machinery, stocks and means of production;

(b)loss of income due to the full or partial suspension of activity for a period not exceeding six months from the occurrence of the disaster.

6.The calculation of the material damage shall be based on the repair cost or economic value of the affected asset before the disaster. It shall not exceed the repair cost or the decrease in fair market value caused by the disaster, namely the difference between the property's value immediately before and immediately after the disaster.

7.The loss of income shall be calculated by subtracting:

(a)the result of multiplying the quantity of the fishery and aquaculture products produced in the year of the natural disaster, or in each following year affected by the full or partial destruction of the means of production, by the average selling price obtained during that year; from

(b)the result of multiplying the average annual quantity of fishery and aquaculture products produced in the three-year period preceding the natural disaster, or a three year average based on the five-year period preceding the natural disaster, excluding the highest and lowest entry, by the average selling price obtained.

8.The damage shall be calculated at the level of the individual beneficiary.

9.The aid and any other payments received to compensate the damage, including payments under insurance policies, shall be limited to 100 % of the eligible costs.

Article 45U.K.Tax exemptions and reductions in accordance with Directive 2003/96/EC

1.Aid in the form of tax exemptions or reductions adopted by the Member States pursuant to Article 15(1)(f) and Article 15(3) of Directive 2003/96/EC shall be compatible with the internal market within the meaning of Article 107(3)(c) and exempt from the notification requirement of Article 108(3) of the Treaty, provided that the conditions laid down in Directive 2003/96/EC and in Chapter I of this Regulation are fulfilled.

2.The beneficiaries of the tax exemptions or reductions shall be selected on the basis of transparent and objective criteria. Where applicable, they shall pay at least the respective minimum level of taxation set by Directive 2003/96/EC.

CHAPTER IVU.K. TRANSITIONAL AND FINAL PROVISIONS

Article 46U.K.Transitional provisions

1.This Regulation shall apply to individual aid granted before its entry into force, if the aid fulfils all the conditions laid down in this Regulation, with the exception of Article 9.

2.Any aid granted before 1 July 2014 by virtue of any regulation adopted pursuant to Article 1 of Regulation (EC) No 994/98 previously in force shall be compatible with the internal market and exempted from the notification requirement of Article 108(3) of the Treaty.

3.Any aid not exempted from the notification requirement of Article 108(3) of the Treaty by virtue of this Regulation or other regulations adopted pursuant to Article 1 of Regulation (EC) No 994/98 previously in force shall be assessed by the Commission in accordance with the relevant frameworks, guidelines, communications and notices.

4.At the end of the period of validity of this Regulation any aid schemes exempted under this Regulation shall remain exempted during an adjustment period of six months.

Article 47U.K.Entry into force and applicability

This Regulation shall enter into force on 1 January 2015.

[F1It shall apply until 31 December 2022 .]

Textual Amendments

This Regulation shall be binding in its entirety and directly applicable in all Member States.

ANNEX IU.K.SME DEFINITION

Article 1U.K.Enterprise

An enterprise is considered to be any entity engaged in an economic activity, irrespective of its legal form. This includes, in particular, self-employed persons and family businesses engaged in craft or other activities, and partnerships or associations regularly engaged in an economic activity.

Article 2U.K.Staff headcount and financial thresholds determining enterprise categories

1.The category of micro, small and medium-sized enterprises (‘SMEs’) is made up of enterprises which employ fewer than 250 persons and which have an annual turnover not exceeding EUR 50 million, and/or an annual balance sheet total not exceeding EUR 43 million.

2.Within the SME category, a small enterprise is defined as an enterprise which employs fewer than 50 persons and whose annual turnover and/or annual balance sheet total does not exceed EUR 10 million.

3.Within the SME category, a micro-enterprise is defined as an enterprise which employs fewer than 10 persons and whose annual turnover and/or annual balance sheet total does not exceed EUR 2 million.

Article 3U.K.Types of enterprise taken into consideration in calculating staff numbers and financial amounts

1.An ‘autonomous enterprise’ is any enterprise which is not classified as a partner enterprise within the meaning of paragraph 2 or as a linked enterprise within the meaning of paragraph 3.

2.‘Partner enterprises’ are all enterprises which are not classified as linked enterprises within the meaning of paragraph 3 and between which there is the following relationship: an enterprise (upstream enterprise) holds, either solely or jointly with one or more linked enterprises within the meaning of paragraph 3, 25 % or more of the capital or voting rights of another enterprise (downstream enterprise).

However, an enterprise may be ranked as autonomous, and thus as not having any partner enterprises, even if this 25 % threshold is reached or exceeded by the following investors, provided that those investors are not linked, within the meaning of paragraph 3, either individually or jointly to the enterprise in question:

(a)public investment corporations, venture capital companies, individuals or groups of individuals with a regular venture capital investment activity who invest equity capital in unquoted businesses (business angels), provided the total investment of those business angels in the same enterprise is less than EUR 1 250 000;

(b)universities or non-profit research centres;

(c)institutional investors, including regional development funds;

(d)autonomous local authorities with an annual budget of less than EUR 10 million and less than 5 000 inhabitants.

3.‘Linked enterprises’ are enterprises which have any of the following relationships with each other:

(a)an enterprise has a majority of the shareholders' or members' voting rights in another enterprise;

(b)an enterprise has the right to appoint or remove a majority of the members of the administrative, management or supervisory body of another enterprise;

(c)an enterprise has the right to exercise a dominant influence over another enterprise pursuant to a contract entered into with that enterprise or to a provision in its memorandum or articles of association;

(d)an enterprise, which is a shareholder in or member of another enterprise, controls alone, pursuant to an agreement with other shareholders in or members of that enterprise, a majority of shareholders' or members' voting rights in that enterprise.

There is a presumption that no dominant influence exists if the investors listed in the second subparagraph of paragraph 2 are not involving themselves directly or indirectly in the management of the enterprise in question, without prejudice to their rights as shareholders.

Enterprises having any of the relationships described in the first subparagraph through one or more other enterprises, or any one of the investors mentioned in paragraph 2, are also considered to be linked.

Enterprises which have one or other of such relationships through a natural person or group of natural persons acting jointly are also considered linked enterprises if they engage in their activity or in part of their activity in the same relevant market or in adjacent markets.

An ‘adjacent market’ is considered to be the market for a product or service situated directly upstream or downstream of the relevant market.

4.Except in the cases set out in paragraph 2, second subparagraph, an enterprise cannot be considered an SME if 5 % or more of the capital or voting rights are directly or indirectly controlled, jointly or individually, by one or more public bodies.

5.Enterprises may make a declaration of status as an autonomous enterprise, partner enterprise or linked enterprise, including the data regarding the thresholds set out in Article 2. The declaration may be made even if the capital is spread in such a way that it is not possible to determine exactly by whom it is held, in which case the enterprise may declare in good faith that it can legitimately presume that it is not owned as to 25 % or more by one enterprise or jointly by enterprises linked to one another. Such declarations are made without prejudice to the checks and investigations provided for by national or Union rules.

Article 4U.K.Data used for the staff headcount and the financial amounts and reference period

1.The data to apply to the headcount of staff and the financial amounts are those relating to the latest approved accounting period and calculated on an annual basis. They are taken into account from the date of closure of the accounts. The amount selected for the turnover is calculated excluding value added tax (VAT) and other indirect taxes.

2.Where, at the date of closure of the accounts, an enterprise finds that, on an annual basis, it has exceeded or fallen below the headcount or financial thresholds stated in Article 2, this will not result in the loss or acquisition of the status of medium-sized, small or micro-enterprise unless those thresholds are exceeded over two consecutive accounting periods.