- Latest available (Revised)

- Point in Time (10/07/2003)

- Original (As enacted)

Finance Act 2003

You are here:

- UK Public General Acts

- 2003 c. 14

- SCHEDULE 5

What Version

Advanced Features

- Show Geographical Extent(e.g. England, Wales, Scotland and Northern Ireland)

- Show Timeline of Changes

Opening Options

Changes over time for: SCHEDULE 5

Version Superseded: 01/12/2003

Status:

Point in time view as at 10/07/2003.

Changes to legislation:

Finance Act 2003, SCHEDULE 5 is up to date with all changes known to be in force on or before 23 May 2024. There are changes that may be brought into force at a future date. Changes that have been made appear in the content and are referenced with annotations.

Changes to Legislation

Changes and effects yet to be applied by the editorial team are only applicable when viewing the latest version or prospective version of legislation. They are therefore not accessible when viewing legislation as at a specific point in time. To view the ‘Changes to Legislation’ information for this provision return to the latest version view using the options provided in the ‘What Version’ box above.

Section 56

SCHEDULE 5U.K.Stamp duty land tax: amount of tax chargeable: rent

IntroductionU.K.

1U.K.This Schedule provides for calculating the tax chargeable—

(a)in respect of a chargeable transaction for which the chargeable consideration consists of or includes rent, or

(b)where such a transaction is to be taken into account as a linked transaction.

Calculation of tax chargeable in respect of rentU.K.

2(1)Tax is chargeable under this Schedule in respect of so much of the chargeable consideration as consists of rent.U.K.

(2)The tax so chargeable is a percentage of the net present value of the rent payable over the term of the lease.

(3)That percentage is determined by reference to whether the relevant land—

(a)consists entirely of residential property (in which case Table A below applies), or

(b)consists of or includes land that is not residential property (in which case Table B below applies),

and, in either case, by reference to the amount of the relevant rental value.

Table A: Residential

| Relevant rental value | Percentage |

|---|---|

| Not more than £60,000 | 0% |

| More than £60,000 | 1% |

Table B: Non-residential or mixed

| Relevant rental value | Percentage |

|---|---|

| Not more than £150,000 | 0% |

| More than £150,000 | 1% |

(4)For the purposes of sub-paragraph (3)—

(a)the relevant land is the land that is the subject of the lease, and

(b)the relevant rental value is the net present value of the rent payable over the term of the lease,

subject as follows.

(5)If the lease in question is one of a number of linked transactions for which the chargeable consideration consists of or includes rent—

(a)the relevant land is any land that is the subject of any of those leases, and

(b)the relevant rental value is the total of the net present values of the rent payable over the terms of those leases.

Net present value of rent payable over term of leaseU.K.

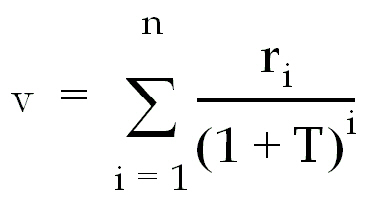

3U.K.The net present value (v) of the rent payable over the term of a lease is calculated by applying the formula:

where—

ri is the rent payable (see paragraphs 4 and 5) in year i,

i is the first, second, third, etc year of the term,

n is the term of the lease (see paragraphs 6 and 7), and

T is the temporal discount rate (see paragraph 8).

Rent payableU.K.

4(1)For the purposes of this Schedule a single sum expressed to be payable in respect of rent, or expressed to be payable in respect of rent and other matters but not apportioned, shall be treated as entirely rent.U.K.

This is without prejudice to the application of paragraph 4 of Schedule 4 (chargeable consideration: just and reasonable apportionment) where separate sums are expressed to be payable in respect of rent and other matters.

(2)Subject to paragraph 5 (effect of provision for rent review), section 51 (contingent, uncertain or unascertained consideration) applies in relation to rent as in relation to other chargeable consideration, but no application may be made under section 90 (application to defer payment in case of contingent or uncertain consideration) in respect of tax chargeable under this Schedule.

(3)No account shall be taken for the purposes of this Schedule of any provision for rent to be adjusted in line with the retail price index.

Effect of provision for rent reviewU.K.

5(1)This paragraph applies where the lease contains provision for adjustment of the rent, as from a specified date or dates, to reflect current market values.U.K.

(2)In this paragraph—

(a)a “rent review” means an adjustment in pursuance of such provision, and

(b)references to the date of a rent review are to the date from which any such adjustment has or would have effect.

(3)If the lease provides for a rent review on or before the end of the second year of the lease, section 51 (contingent, uncertain or unascertained consideration) applies in relation to the possibility that the rent may be adjusted on that review.

(4)If the lease provides for a rent review after the end of the second year of the lease, the annual rent payable after that review—

(a)is determined without regard to the possibility of an adjustment on that review, and

(b)is assumed to be the same as the annual rent payable over the year preceding the first rent review or, if the period from the beginning of the term of the lease to the date of the first rent review is less than a year, over that period.

Term of leaseU.K.

6(1)For the purposes of this Schedule the term of a lease is determined as follows.U.K.

(2)Subject to the following provisions of this paragraph, the term of a lease is—

(a)the contractual term specified in the lease, or

(b)if shorter, the period from the date of the grant of the lease until the end of the contractual term.

(3)Where in England and Wales or Northern Ireland—

(a)an agreement for a lease is entered into,

(b)the agreement is substantially performed otherwise than by completion, and

(c)a lease is subsequently granted in pursuance of the agreement,

the term of a lease is the period from the date of substantial performance of the agreement until the end of the contractual term specified in the lease.

In this sub-paragraph “substantially performed” and “completion” have the same meanings as in section 44 (contract and conveyance).

(4)Notwithstanding anything in sub-paragraph (2) or (3), a lease granted by way of renewal of a previous lease is treated as if its term had begun on the expiry of the previous lease.

This applies, in particular, to leases granted under Part 2 of the Landlord and Tenant Act 1954 (c. 56) or under the Business Tenancies (Northern Ireland) Order 1996 (S.I. 1996/725 (N.I. 5)).

(5)No account shall be taken of any right of either party to determine the lease or to renew it.

Treatment of lease for indefinite termU.K.

7(1)For the purposes of this Schedule a lease for an indefinite term is treated as if it were a lease for a term of 12 years.U.K.

(2)Sub-paragraph (1) applies, in particular, to a lease expressed to be—

(a)perpetual,

(b)for life, or

(c)determinable on the marriage of the lessee.

(3)No account shall be taken for the purposes of this Schedule of any statutory provision deeming such a lease to be a lease for a longer definite term.

Temporal discount rateU.K.

8(1)For the purposes of this Schedule the “temporal discount rate” is 3.5% or such other rate as may be specified by regulations made by the Treasury.U.K.

(2)Regulations under this paragraph may make any such provision as is mentioned in subsection (3)(b) to (f) of section 178 of the Finance Act 1989 (c. 26) (power of Treasury to set rates of interest).

(3)Subsection (5) of that section (power of Inland Revenue to specify rate by order in certain circumstances) applies in relation to regulations under this paragraph as it applies in relation to regulations under that section.

Tax chargeable in respect of consideration other than rentU.K.

9(1)Where in the case of a transaction to which this Schedule applies there is chargeable consideration other than rent, the provisions of this Part apply in relation to that consideration as in relation to other chargeable consideration.U.K.

(2)If the annual rent exceeds £600 a year, the 0% band in the Tables in subsection (2) of section 55 does not apply and any case that would have fallen within that band is treated as falling within the 1% band.

(3)For the purposes of sub-paragraph (2) the “annual rent” means the average annual rent over the term of the lease or, if—

(a)different amounts of rent are payable for different parts of the term, and

(b)those amounts (or any of them) are ascertainable at the effective date of the transaction,

the average annual rent over the period for which the highest ascertainable rent is payable.

(4)Tax chargeable under this Schedule is in addition to any tax chargeable under section 55 in respect of consideration other than rent.

(5)Where a transaction to which this Schedule applies falls to be taken into account for the purposes of that section as a linked transaction, no account shall be taken of rent in determining the relevant consideration.

Increase of rent treated as grant of new leaseU.K.

10(1)Where a lease is varied so as to increase the amount of the rent, the variation is treated for the purposes of this Schedule as if it were the grant of a lease in consideration of the additional rent made payable by it.U.K.

(2)Sub-paragraph (1) does not apply to an increase of rent in pursuance of a provision already contained in the lease.

InterpretationU.K.

11U.K.In Scotland any reference in this Part to the term of a lease is to the period of the lease.

Options/Help

Print Options

PrintThe Whole Act

PrintThis Schedule only

You have chosen to open The Whole Act

The Whole Act you have selected contains over 200 provisions and might take some time to download. You may also experience some issues with your browser, such as an alert box that a script is taking a long time to run.

Would you like to continue?

You have chosen to open The Whole Act as a PDF

The Whole Act you have selected contains over 200 provisions and might take some time to download.

Would you like to continue?

You have chosen to open the Whole Act

The Whole Act you have selected contains over 200 provisions and might take some time to download. You may also experience some issues with your browser, such as an alert box that a script is taking a long time to run.

Would you like to continue?

You have chosen to open the Whole Act without Schedules

The Whole Act without Schedules you have selected contains over 200 provisions and might take some time to download. You may also experience some issues with your browser, such as an alert box that a script is taking a long time to run.

Would you like to continue?

You have chosen to open Schedules only

The Schedules you have selected contains over 200 provisions and might take some time to download. You may also experience some issues with your browser, such as an alert box that a script is taking a long time to run.

Would you like to continue?

Legislation is available in different versions:

Latest Available (revised):The latest available updated version of the legislation incorporating changes made by subsequent legislation and applied by our editorial team. Changes we have not yet applied to the text, can be found in the ‘Changes to Legislation’ area.

Original (As Enacted or Made): The original version of the legislation as it stood when it was enacted or made. No changes have been applied to the text.

Point in Time: This becomes available after navigating to view revised legislation as it stood at a certain point in time via Advanced Features > Show Timeline of Changes or via a point in time advanced search.

See additional information alongside the content

Geographical Extent: Indicates the geographical area that this provision applies to. For further information see ‘Frequently Asked Questions’.

Show Timeline of Changes: See how this legislation has or could change over time. Turning this feature on will show extra navigation options to go to these specific points in time. Return to the latest available version by using the controls above in the What Version box.

Opening Options

Different options to open legislation in order to view more content on screen at once

More Resources

Access essential accompanying documents and information for this legislation item from this tab. Dependent on the legislation item being viewed this may include:

- the original print PDF of the as enacted version that was used for the print copy

- lists of changes made by and/or affecting this legislation item

- confers power and blanket amendment details

- all formats of all associated documents

- correction slips

- links to related legislation and further information resources

Timeline of Changes

This timeline shows the different points in time where a change occurred. The dates will coincide with the earliest date on which the change (e.g an insertion, a repeal or a substitution) that was applied came into force. The first date in the timeline will usually be the earliest date when the provision came into force. In some cases the first date is 01/02/1991 (or for Northern Ireland legislation 01/01/2006). This date is our basedate. No versions before this date are available. For further information see the Editorial Practice Guide and Glossary under Help.

More Resources

Use this menu to access essential accompanying documents and information for this legislation item. Dependent on the legislation item being viewed this may include:

- the original print PDF of the as enacted version that was used for the print copy

- correction slips

Click 'View More' or select 'More Resources' tab for additional information including:

- lists of changes made by and/or affecting this legislation item

- confers power and blanket amendment details

- all formats of all associated documents

- links to related legislation and further information resources

All content is available under the Open Government Licence v3.0 except where otherwise stated. This site additionally contains content derived from EUR-Lex, reused under the terms of the Commission Decision 2011/833/EU on the reuse of documents from the EU institutions. For more information see the EUR-Lex public statement on re-use.

All content is available under the Open Government Licence v3.0 except where otherwise stated. This site additionally contains content derived from EUR-Lex, reused under the terms of the Commission Decision 2011/833/EU on the reuse of documents from the EU institutions. For more information see the EUR-Lex public statement on re-use.